13

February 2024

Fostering a Culture of Teamwork and Learning - Angles & Perspectives Q4 2023

Kevin Cousins, Head of Research

PSG Asset Management

Greg Hopkins, Deputy-Chief Investment Officer

Fostering a culture of teamwork and learning

Culture is one of the key factors professional investors and fund selectors consider before allocating money to investment managers. However, it is seldom discussed outside of the due diligence process, and perhaps understandably, the average investor tends to underestimate culture’s importance. In our view, culture is crucial to our ability to replicate our proven 3M investment process over time and in constructing differentiated investment portfolios for our clients.

Framing the learning problem

We draw extensively on work by Annie Duke (see detail below) to outline the learning issues and then describe how we create a teamwork-driven culture that is conducive to learning.

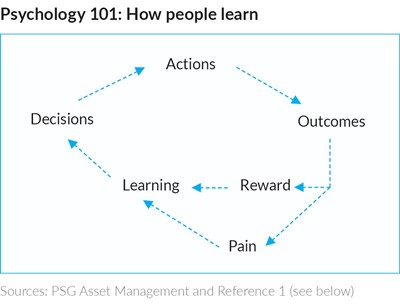

Psychologists believe that feedback loops are the key to learning. However, the theoretical model of how people should learn does not work in environments with lots of uncertainty (things we don’t know), lots of luck (things we can’t control) and clearly visible outcomes. Here the feedback loops can be deeply distorted by outcomes resulting from chance or incomplete information rather than the decision itself. Investment management is a typical example of this.

In such an environment:

- Good outcomes are often attributed to skill.

- Poor outcomes are often attributed to bad luck.

This occurs because the alternative is distinctly uncomfortable for most people. If we attribute the ‘pain’ of bad outcomes to poor decisions, it feels like an attack on our identity, whereas attributing this ‘pain’ to bad luck means we don’t have to update prior beliefs, so we feel better. However, this has a devastating impact on learning.

As Annie Duke says, if you are part of a group sharing bad luck stories (blaming the market for poor decisions) how can you learn?

Key pillars of our culture: A team-based approach

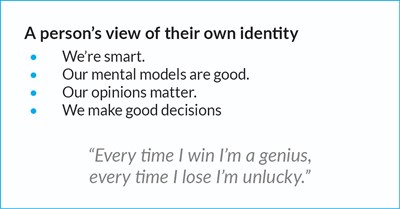

At PSG Asset Management, we see huge risks stemming from an inappropriate culture, especially the typical high ego ‘star manager’ environment where it is important to take credit for successes and avoid being blamed for failures. This environment makes investment errors difficult to discuss – it risks becoming an emotional process of allocating blame.

Discussing a mistake is fraught with ego-related problems. The natural reaction is to see the discussion as an attack on your own identity and to respond very defensively.

Most investment errors arise from incomplete information or biases in evaluating the decision. While biases are pretty easy to spot in other people, they seem very hard to identify in ourselves. The asset management industry is full of very smart people. Unfortunately, smart people, who know all about biases, are actually more prone to succumbing to those very biases:

- They believe their knowledge of biases protects them against being biased.

- They can slice and dice data to suit prior beliefs.

- They aren’t actually lying, just very good at fooling themselves.

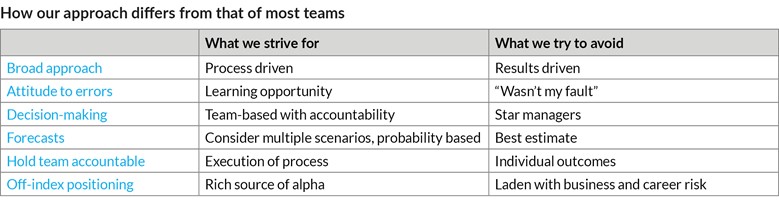

To compensate for bias, we strive for a low-ego culture where the focus is a joint search for the truth, an evidence-led discussion of the objective reality. Across our team, we have diverse personalities, qualifications and natural focuses, well suited to this task. Importantly, there is also a collective muscle memory from many decades of experience in managing money. Our Investment Committee votes on, and has responsibility for, all buylist decisions. We hold each other accountable, and we keep detailed records of individual voting decisions, idea generation, research impact and performance attribution. Although we do monitor the outcomes, the focus is more on whether team members are executing consistently on our process and contributing to the team-based approach. This gives us the best opportunity to learn from our mistakes and incrementally improve our investment process over time.

Key pillars of our culture: Focus on the process, not the result

Even if we manage an evidence-based discussion on an investment error, when evaluating individual outcomes, it is very easy to draw incorrect conclusions with the benefit of hindsight, known as ‘resulting’. Our process helps to avoid this in several ways:

- We overtly consider a range of outcomes ahead of time, including bear and bull cases, acknowledging the inherent uncertainty.

- Where possible, we assign probabilities to these outcomes, which greatly assists with impartial evaluation of evidence and being open-minded to other scenarios and perspectives rather than being ‘right’.

- Our investment team leadership ‘walks the talk’ consistently holding team members accountable for process execution rather than individual outcomes.

We are not benchmark cognisant, and hence often have significant positions that are not owned by our competition. Likewise, we do not own large index components if they do not successfully pass our process and are not considered one of our best ideas. This makes us vulnerable to one aspect of resulting: conventional bets gone wrong tend to be regarded as bad luck (“who could have known?”) but unconventional bets that do not pay off are seen as egregious errors.

While this makes for some uncomfortable interactions, in today’s world dominated by passive and benchmark-hugging investors, off-index positions have the potential to be deeply mispriced, making the focus on process rather than outcomes key to delivering significant alpha over time.

Key pillars of our culture: Continual learning

We have highlighted how a low-ego dynamic and a focus on process enable us to discuss and learn from investment errors. However, this is just part of a culture that views continual learning as essential to the growth of our business. Our Continual Learning Centre (CLC) hosts deep-dive presentations and discussions with the investment team on key areas of process. These are recorded and form part of our induction programme for new hires.

The team members, who read widely and are naturally curious, contribute to an email of weekend reading, podcasts and videos that is circulated every Friday. This is a ‘living’ compilation aimed at delivering both topical insights and learning material of enduring value.

This obligation to devote time to learning no matter what stage you are at in your career is an important part of our culture in a continually evolving world.

Culture actively contributes to our investment success

Our culture is central to our ability to deliver long-term investment success to our clients. It creates an enabling environment within which our investment process can flourish. It does this by creating pillars of support that underpin our investment process by encouraging a team-based approach, focusing on the process rather than outcomes and instilling an appreciation of the importance of continual learning.

References:

- Mastering the Decision-Making Process with Annie Duke, Bigger Pockets Real Estate Podcast, September 2018.

- Thinking in bets: Making smarter decisions when you don’t have all the facts, Annie Duke, Penguin, 2018.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

In this edition, Head of Research Kevin Cousins and Co-CIO Greg Hopkins explain why culture is so important to us at PSG Asset Management, and how it enables us to achieve excellent investment outcomes for our clients. Then, we turn our attention to the many-faceted nature of risk. Head of Equities Justin Floor and Co-CIO John Gilchrist unpack why a more nuanced view of risk can facilitate more robust decision-making. Finally, Head of Equities Justin Floor and Fund Manager Dirk Jooste get to grips with the thorny issues of the risk of investing in SA equities, and weighing them against the opportunities we see ahead.

Read moreIntroduction - Angles & Perspectives Q4 2023

Read moreWe are What We Measure - Getting to Grips with Volatility - Angles & Perspectives Q4 2023

Read moreInvesting in SA-Exposed Securities: Finding the Opportunity Amidst the Danger - Angles & Perspectives Q4 2023

Read moreStay Informed

Sign up for our newsletters and receive information on finance.