22

February 2024

Budget Speech 2024/2025

Ronald N King CFP® CTA®

Head: Public Policy & Regulatory Affairs

A summary of key Budget provisions and highlights, as well as an infographic of the South African Budget Speech 2024/2025.

Tax table

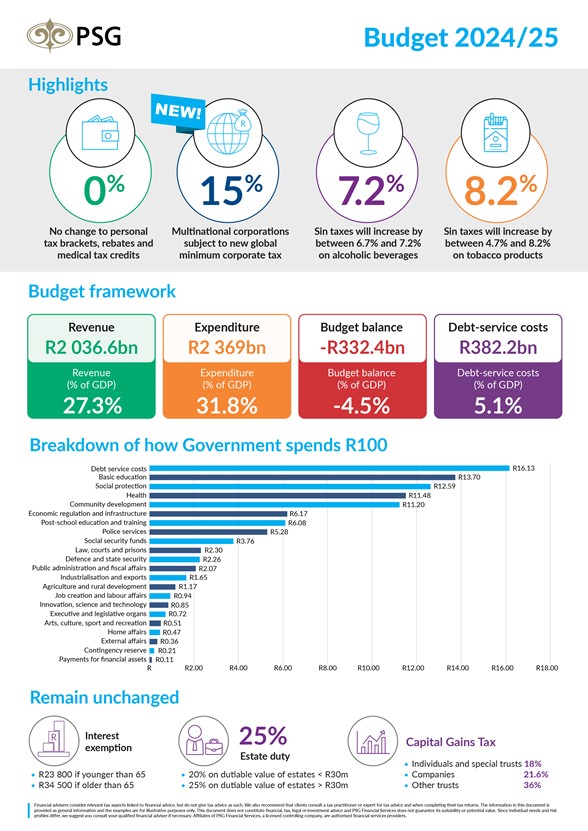

No adjustments were made to the individual tax brackets and rebates. Everyone will therefore pay more tax in line with their annual salary increase.

Capital gains tax (CGT)

The inclusion rate for capital gains remains unchanged at 40% for natural persons and 80% for companies and trusts.

This means the maximum CGT rates are:

- Individuals and special trusts 18%

- Other trusts 36%

- Companies 21.6%

- Individual policyholder funds 12%

Corporate taxes

The rate of corporate income tax remains at 27% as introduced last year.

Together with other countries, South Africa is instituting a flat rate of 15% on multinationals irrespective of where they operate from as of 1 January 2024. The Bill has been published for comment.

Dividends tax and interest exemption

Dividends tax remains at 20% and no changes were made to the interest exemptions either. The exemption remains R23 800 for those younger than 65 and R34 500 for those aged 65 or older.

Motor vehicle expenses

SARS is yet to publish the revised motor vehicle tax table for the new tax year. The table will be available on their website under Legal Counsel / Secondary Legislation / Income Tax Notices / 2024 / Fixing of rate per kilometre in respect of motor vehicles.

Trusts

No changes to the taxation of trusts were announced but some changes to the taxation of interest-free loans can be expected to provide more clarity.

Medical aid rebates

No changes were made to the medical tax rebates. The tax credit for the first two dependants remains at R364, and for additional dependants at R246. In order for the NHI to roll out, Government will focus on key enablers that include the following:

- Building a national health information system and digital patient records;

- Upgrading health facilities and improving quality of care to ensure that they meet the minimum criteria to be certified and accredited for contracting under NHI;

- Strengthening facility and district management in preparation for contracting;

- Granting semi-autonomous status for central (and potentially other) hospitals; and

- Developing reference prices and provider payment methods for hospitals

Retirement fund changes

No changes were made to the tax deductibility of retirement fund contributions or the lump sum tax

tables. Taxpayers will be able to deduct contributions to any retirement fund up to a maximum of 27.5% of the greater of remuneration for PAYE purposes or taxable income (both excluding retirement fund lump sums and severance benefits). The deduction is capped at R350 000.

The two-pot system will be introduced from 1 September 2024. Permissible withdrawals from the portion invested prior to 1 March 2024 will be taxed according to the lump sum tables. Withdrawals from the one-third savings pot will be taxed at marginal rates, while at retirement it will be taxed according to the lump sum tables. The retirement pot will purchase an annuity. Rules on access to this pot in extreme circumstances will be consulted on.

Retirement fund changes

No changes were made to the tax deductibility of retirement fund contributions or the lump sum tax

tables. Taxpayers will be able to deduct contributions to any retirement fund up to a maximum of 27.5% of the greater of remuneration for PAYE purposes or taxable income (both excluding retirement fund lump sums and severance benefits). The deduction is capped at R350 000.

The two-pot system will be introduced from 1 September 2024. Permissible withdrawals from the portion invested prior to 1 March 2024 will be taxed according to the lump sum tables. Withdrawals from the one-third savings pot will be taxed at marginal rates, while at retirement it will be taxed according to the lump sum tables. The retirement pot will purchase an annuity. Rules on access to this pot in extreme circumstances will be consulted on.

Financial advisers consider relevant tax aspects linked to financial advice, but do not give tax advice as such. We also recommend that clients consult a tax practitioner or expert for tax advice and when completing their tax returns. The opinions expressed in this document are the opinions of the writer and not necessarily those of PSG Financial Services and do not constitute advice. Although the utmost care has been taken in the research and preparation of this document, no responsibility can be taken for actions taken based on information in this newsletter. Should you require further information, please consult an adviser for a personalised opinion.

Some highlights from the Budget speech:

#SABudget2024 #BudgetSpeech2024 #SABudgetSpeech2024 #Budget2024

Stay Informed

Sign up for our newsletters and receive information on finance.