Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

10

May 2022

Challenging the seven narratives embedded in current portfolios - Angles & Perspectives

Shaun le Roux, Fund Manager

Asset Management

In this article, Shaun considers how the prevailing views have influenced portfolio positioning for most managers. He argues that global positioning reflects strongly entrenched perceptions around riskiness and expected returns from various asset classes. In our view, the future is likely to look very different to the recent past, and investors who have fallen into the trap of extrapolating the experience of the past decade into the future, should consider amending their portfolios to reflect a material change in future sources of risk and return.

Challenging the seven narratives embedded in current portfolios

Global positioning reflects strongly entrenched perceptions around riskiness and expected returns from various asset classes. Recent developments, such as the US Federal Reserve (the Fed) starting to tighten amidst rampant inflation, are testing those perceptions. We argue that the future is likely to look very different to the recent past, and investors who have fallen into the trap of extrapolating the experience of the past decade into the future, should consider amending their portfolios to reflect a material change in future sources of risk and return.

Persistent conditions over the past decade or so have entrenched a certain world view

An entire generation of global money managers have been programmed to think about risk and return in a particular fashion. They have been conditioned to behave in a way that is suited to market dynamics that have persisted for long periods of time, in some cases a few decades. What happens when those conditions change abruptly and start pointing in the opposite direction? Given the human tendency to extrapolate recent experience, the longer we have endured a set of circumstances, the more entrenched views become, making it much harder to change course. We think global financial markets have passed a major inflection point. A dramatic change in economic and monetary conditions is underway and most investors will need to think afresh about where returns will come from over the decade ahead. They will also need to drastically recalibrate their perceptions around risk. This will likely require a meaningful and an enduring adjustment for many portfolios, giving rise to big divergences in future performance.

Kevin Cousins argues in his article What if secular growth, and not stagnation, is the new normal? that secular stagnation and low nominal growth were strong driving forces behind asset class returns over the past decade. Following 40 years of declining or benign inflation in the US, the 2020 pandemic induced an economic slump and a multi-century low in interest rates. This saw extremely low costs of capital for certain assets boosting demand for long duration assets including growth equities, driving up prices and making them very expensive. Secular stagnation and a very low cost of capital were very supportive of the relative performance of the winners of the past decade: financial assets in general, the US (given its dominance in financial markets and technology), and growth and quality (long duration) equities.

Contrarians and value managers have had to be patient

Over the past 10 years, there have been many false starts to a reversal in trend, with many saying that it was time for outperformance by value, emerging markets or non-US international equities. Like the boy crying wolf, the contrarian (value) camp has been repeatedly embarrassed when the winners (growth) resumed their strong uptrend. With growth/quality (as represented by the MSCI World Quality Index) outperforming eight of the last nine years, confidence in these styles was to be expected and extreme crowding into the winners of the past decade followed. This trend was exacerbated by the significant growth in passive investing – a strategy which is price-insensitive and sees flows being directed to the winners of the past, the largest stocks. The result has been extremely aggressive positioning within global financial markets with portfolios firmly anchored in what has worked in the last decade or so.

But now, things have changed

We see clear evidence that we are beyond an inflection point in both interest rates and inflation. While the US inflation rate may well have peaked in the current cycle at 8.5%, current US CPI exceeds the South African equivalent by 2.8%. We think it is probable that global inflationary pressures will persist. Considering that few US fund managers have seen inflationary pressure during their careers – in stark contrast to their emerging market peers – they are unlikely to find it easy to adapt to a change in status quo. A review of market positioning illustrates that the bulk of the money is positioned for the prevailing narratives around risk and returns to persist. We will now examine some of those prevailing narratives and present an alternative view.

Prevailing narratives that are reflected in market positioning:

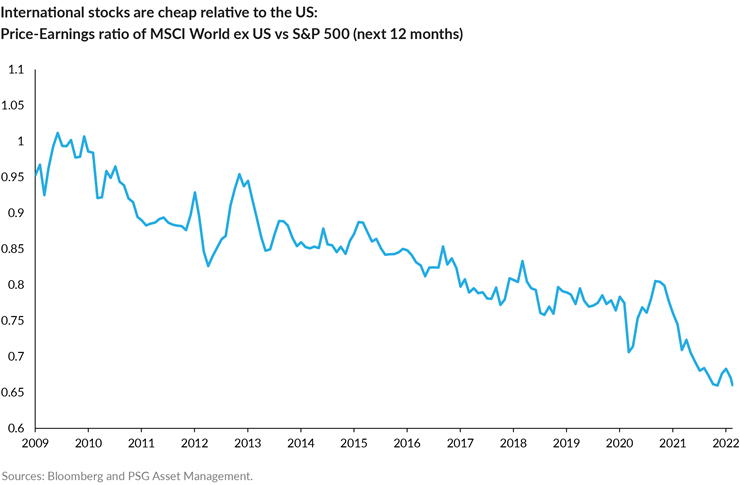

- US equities will continue to outperform

The US has outperformed other stock markets dramatically over the past decade. As the chart below shows, a significant proportion of this outperformance has come from relative valuation expansion – the US has become expensive while other markets have largely languished in the era of secular stagnation. Global stock market valuations traded in line with the US after the Global Financial Crisis (GFC). Since then, the premium valuation attached to US stocks has grown steadily to the extent that other countries currently trade at a 33% discount to the US. We argue that price levels are a big determinant of future returns and from this base, US underperformance (at an index level) looks like the more likely outcome.

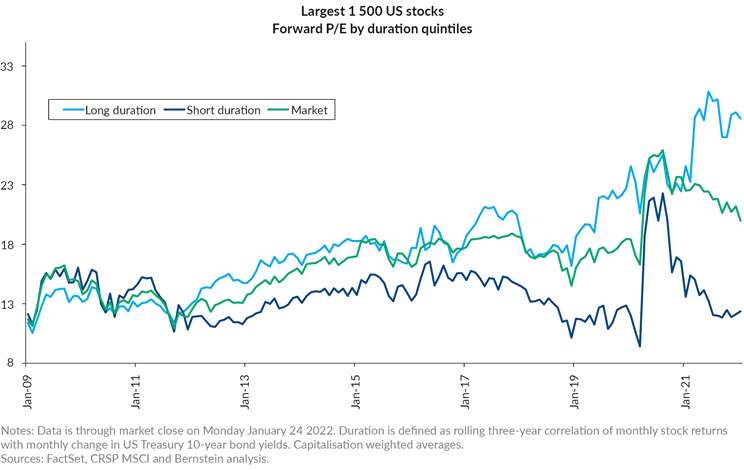

Long duration assets will continue to outperform

The past decade has been very kind to long duration assets, which derive a significant proportion of their value from the discount rate that is applied to future cash flows. A low discount rate supports a high valuation being ascribed to companies with high expectations for future growth. As the chart below shows, the anomaly of current times is that stocks in the US that perform poorly when rates rise (long duration equities – top line in chart) have become very expensive just as rates have started rising, with the market now pricing in aggressive 2022 hikes. In contrast, short duration equities (bottom line in chart) or stocks that tend to do better at times when rates are rising (typically because nominal growth is strong) remain cheap and trade at one of the widest discounts to long duration stocks on record. We expect the relative performance of carefully selected short duration equities to materially outperform the average long duration equity. Short duration equities that we favour would include interest rate sensitive financials, materials, energy and value stocks sitting on depressed earnings levels. Even after recent outperformance, global portfolios remain materially underexposed to short duration equities, which lays the foundation for a painful rotation and a significant headwind to future returns.

Caveat emptor: long duration stocks are expensive as rates start rising

Risk remains on the other side of the value/growth distribution as long duration stocks are still expensive

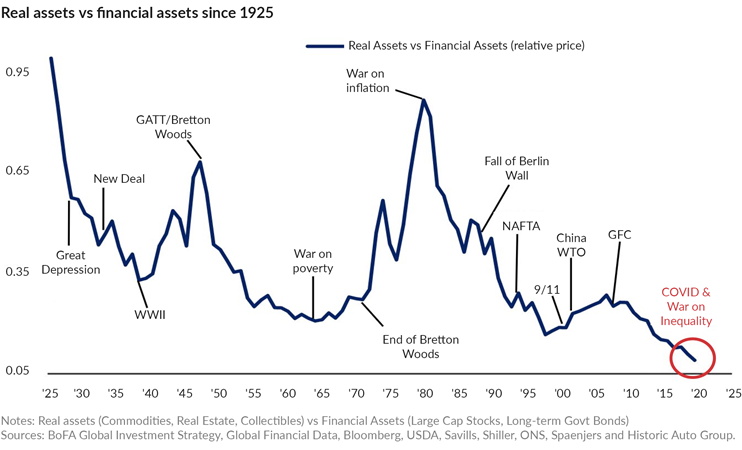

Financial assets will continue to outperform real assets

A consequence of the era of ultra-easy money, including massive quantitative easing (QE) injections, has been the suppression of yields and a driving up of the prices of financial markets (Wall Street) at a time when the real economy (Main Street) has largely stagnated.As mentioned in Kevin’s article What if secular growth, and not stagnation, is the new normal?, we see clear reasons why Main Street should perform better from here. It is interesting to observe in the chart below that 2021 saw real assets being valued at their lowest level relative to financial assets in a century. We would favour real assets (and their indirect beneficiaries including many stocks on the JSE) to the direct plays on cheap and plentiful money.

Emerging markets will continue to underperform

Many commentators have called for a reversal of the underperformance by emerging markets over the past decade, only to be proved wrong. We highlight the dangers of expressing a view on emerging markets as if a particular index is indicative of a homogenous group of companies or geographies. For example, in recent times, the MSCI Emerging Market ETF has come to be heavily weighted in Chinese and technology companies. Recent regulatory woes in China and the exclusion of Russia indicate the perils of a one-size-fits-all approach in emerging markets. We see clear opportunities in emerging markets but would differentiate between commodity exporters (like South Africa and Brazil) and commodity importers (like India). We expect carefully selected emerging market stocks to outperform US indices over the next few years.Passive is a low-risk outperforming strategy

Global indices have become dominated by tech shares with five mega caps accounting for 25% of the S&P 500 Index. That trend has coincided with the increasing prevalence of passive investing – a lower-cost approach that reduces the risk associated with fund or security selection. The results of a passive equity approach have been materially flattered by the relative performance of the mega caps. This article suggests several reasons why differentiated active strategies are likely to outperform in the years ahead. This will challenge the prevailing narratives around passive investing delivering market-beating returns at lower levels of risk. While we are confident that passive will continue to play a valuable role in balanced portfolios, we think current expectations will need to be tempered.Equity market risk can be hedged by investing in bonds and defensive quality equities

Investors tend to seek out safe havens in times of turmoil like the present. Traditionally, bonds and defensive quality equities have served this purpose. Global bonds have been in a 40-year bull market that looks like it may be coming to an end. Over this period, bond yields have traditionally come down (and prices have risen) when equity risk premiums rose, as equities performed poorly during economic setbacks. This has smoothed the ride for a 60-40 investor and proved to be a successful strategy for lowering risk and enjoying the return benefits of risky equities. However, recent months have shown that the current environment is one in which bond yields can rise while equities are falling. This is because inflation is now widespread, real yields are incredibly low, and central banks are in the first innings of rate normalisation – not a healthy starting point for sovereign bonds to be safe havens. Similarly, quality defensive equity valuations have been boosted by negative real bond yields and we see clear evidence of crowding into this part of equity markets. Today, rates and input cost pressures are rising and secular stagnation may be coming to an end. Hence, we are cautious on the future relative performance from equities that are currently perceived to be defensive growers and are very expensive.- Commodity stocks are risky

By definition, commodities are substitutable and no producer has pricing power. This means that prices fluctuate wildly with changes in demand and supply. Some investors argue that such volatility makes commodities and commodity stocks poor investments. Our process is strongly focused on the capital cycle, which shows that high prices typically result in more supply − meaning prices eventually fall to levels at which additional supply becomes constrained. We tend to invest only in commodity stocks where we see clear evidence of constrained supply that should result in sustainably higher profits until capacity is expanded. There are many current examples of extreme supply constraints in global commodity markets that will take many years to be overcome. A number of factors have contributed to a perfect storm in under-investment over the past several years. These include shareholder pressure to improve capital discipline and cash returns, coupled with the aggressive ESG stance towards materials and energy companies, particularly in the fossil fuel domain. Furthermore, the desire to drastically alter the composition of future energy consumption – building out renewable grids and transitioning to electric vehicles (EVs) – will likely put pressure on already constrained raw materials. The consequence of these factors is commodity markets that have already been tight before the disruption of Russian supply or before we consider the possible end to secular stagnation. All this speaks to an environment of stronger commodity prices for longer, which we believe has failed to be captured in the valuations of several materials and energy companies.

While commodity prices are likely to remain volatile as near-term demand is very uncertain, we argue that investors who can accept volatility and focus on the medium-term outlook, will be well rewarded by carefully selected commodity-related investments.

The importance of a solid process and an open mind

Clearly, we are heading into a very uncertain time. Geopolitical risks have risen to a level not seen in decades. Central banks are going to find it very difficult to walk the tightrope towards policy normalisation without disrupting financial markets. We anticipate volatility in the months ahead. At times like these, it is important to have a solid process and an open mind. The ability to take a longer-term view is a clear advantage when most market participants focus on the near term and have such entrenched positioning. We conclude that we have entered a period where the prevailing view on what constitutes risk and where returns are going to come from will be turned on its head. The future looks likely to be very different to the past, and different perspectives and an active approach will be well rewarded.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

As bottom-up investors we steer clear of macro forecasts. However, stock pickers risk short-changing their investors if they do not take cognisance of the environment within which companies are operating.

Read moreHow our market views translate in our portfolios - Angles & Perspectives

In the final article of this edition, we unpack how our differentiated views have been implemented in our portfolios, and how we believe this positions us to deliver future growth. They argue that our 3M investment philosophy leads us to hunt for underappreciated quality at a favourable price, and that the current market environment is offering an above-average number of opportunities, many of which are unlikely to be found in more mainstream portfolios.

Read moreIntroduction - Angles & Perspectives Q1 2022

Our differentiated perspective allows us to look beyond the prevailing narratives. In the past, we have elaborated on how market narratives often become an unquestioned underpin for investors’ choices. The antidote, we have long argued, lies in independent thinking, thorough research, and open and honest debate. Sounds simple, doesn’t it? The challenge, however, is that narratives can become entrenched and normalised to such an extent that it can be very difficult to stand against ‘common wisdom’.

Read moreWhat if secular growth, and not stagnation, is the new normal? - Angles & Perspectives

This article explores some of the currently widely held beliefs and weighs the arguments in favour of a contrary view. We believe there is compelling evidence that the low growth, low interest rate environment following the Global Financial Crisis (GFC) was an anomaly, rather than the new normal. The implications for portfolio constructors are profound.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.