Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

08

March 2023

Are we on the brink of a major market correction?

Tunin Roy

Wealth Adviser

There seems to be a lot of noise around at present asking whether there may be a major stock market correction imminent given that valuations on some US megacap stocks are extreme and that there have been signs in recent weeks of some speculative excesses in companies like Gamestock and Tesla by retail traders with new low-cost, app-based trading accounts such as Robinhood flush with stimulus cheques which they are using to speculate in the US stock market. I will briefly address this question but would like to address whether this is the right question for most investors to be asking. Remember, investors are not traders.

“ Investors may be becoming worried while others may be falling prey to speculative excess . ”

Investors may be becoming worried while others may be falling prey to speculative excess

There seems to be a lot of noise around at present asking whether there may be a major stock market correction imminent given that valuations on some US megacap stocks are extreme and that there have been signs in recent weeks of some speculative excesses in companies like Gamestock and Tesla by retail traders with new low-cost, app-based trading accounts such as Robinhood flush with stimulus cheques which they are using to speculate in the US stock market. I will briefly address this question but would like to address whether this is the right question for most investors to be asking. Remember, investors are not traders.

It is worth stating at the outset….. There is no single entity which constitutes the stock market. Sure, there is a place where stocks are traded but to say that “the market is too high” or “the market is too expensive” or even “the market is set to crash” means very little because “the market” consists of a multitude of stocks with very different characteristics that share very little in common. Most people refer to either the US or their local stock market as “the market.” Which is right? Probably neither. That is because when assessing investment in stocks, one has to look at the characteristics of the individual companies in which you are investing and the price that you are paying for them. That is what our portfolio managers and unit trust managers do for us every day.

It is possible that there is a bubble forming in certain megacap tech stocks, particularly in the US, but it is quite possible that even in the “bubble sectors” the bubble could continue to inflate for another year or more. The most likely catalyst for the bursting of the bubble would be the re-emergence of US inflation causing the Fed to cut its printing program and raise rates. Although inflation seems possible, the policy response of raising rates does not seem likely any time soon. The Fed have now moved to accommodate inflation to go over and above their stated target range without raising rates.

“The real problem is in major bull markets that last for years. Long, slow-burning bull markets can spend many years above fair value and even two, three, or four years far above,” says a long time market analyst.

In the US, “bifurcation” has become a very frequently-used and relevant term to describe the fact that, even in the US, there are lots of unloved areas many stocks in other countries present value even while the megacap stocks such as Amazon, Google, Facebook, Apple, Microsoft, Visa etc. look very stretched. There are many stocks whose prices have not risen substantially during recent years. I would caution against throwing the baby out with the bathwater and reducing exposure to equities to a very low level. Any potential bubble is concentrated in the US megacaps, tech and healthcare sectors. Other stocks are not expensive and many have actually been in a bear market for years – just look at the banks, for example. The extreme market valuations of “the market” do not persist if you strip out the tech sector and valuations are actually quite reasonable. Speculative activity seems to be pretty confined to the tech sector as well. This concentration of market cap in extremely valued areas makes passive investing dangerous at present as all broad global equity indexes are dominated by the US megacaps.

Monetary policy is extremely supportive for equities. You get sub-inflation post-tax returns on cash and bonds almost everywhere in the world so where else will money go? In South Africa, we are lucky to have very attractive real returns on bonds so there is an argument for a more balanced exposure here.

However, calling the short-term direction of the equity markets is the wrong exercise for most investors. And this is the reason:

Equities KILL all other asset classes over the long-term. This is over any multi-decade long period of time and in every market in the world. NO ONE can afford to pass on the ONE advantage all investors have access to:

- Compounding equity returns over many years

“The power of compounding is the 8th wonder of the world; he who understands it earns it; he who doesn’t pays it” (Albert Einstein)

To create meaningful wealth over long periods of time a healthy weighting in equities is required - “it's time in the markets that matters, not timing markets”

Equities deliver spectacularly over the long-term. The temptation to time markets is hard to resist. We all feel it… It feels right to buy when the news is good and sell when the news is bad, but that does not reward the investor. Emotions and feelings always trump reason and when faced with bad news selling feels like right thing to do. Equity returns have undoubtedly been poor in South Africa over that 5 years but this is highly unusual and unlikely to continue.

We don’t fully grasp the compounding power of equities over long periods of time. Our minds are not wired to grasp non-linear growth and often this means that, as investors, fears about the short-term lead us to miss out on the phenomenal long-term opportunities that equities present. Non-linear/exponential (constant proportion) vs linear growth (constant amount) is a very powerful thing on the side of equities. Equities give a multi-decade wealth-generating opportunity like nothing else on this planet.

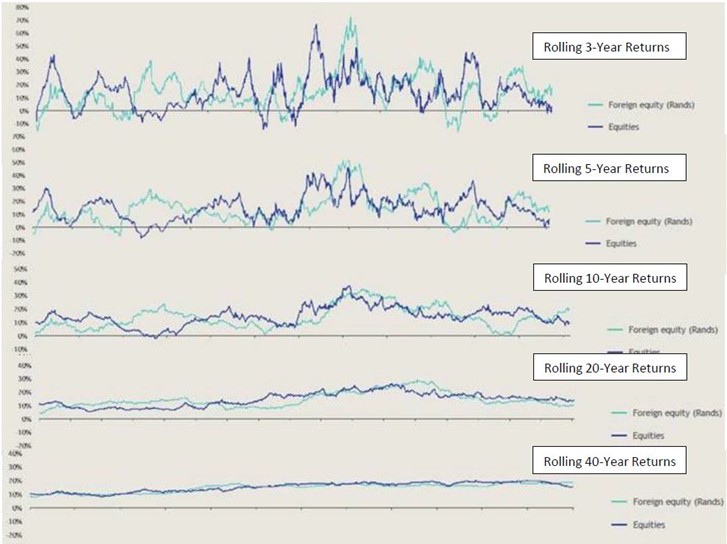

Have a look at the charts below which show rolling returns from foreign and local equities over various periods since 1934 (with thanks to Karl Leinberger of Coronation Fund Managers):

The point to note is that over longer periods of time, equity returns are ALWAYS positive, way above cash and never negative. If your goal is to create wealth across generations, an equity exposure is essential and timing your entry to the market is largely irrelevant.

Sure, I do think some degree of caution on large-cap US equities is warranted, but a long-term allocation to global equities is essential and can be put in place on a gradual basis to minimise the impact of short-term volatility or maintained with caution by exposure to the right companies. Locally, I think opportunity in equities is now.

The key here is to establish your goals and accept at the outset that looking at short-term returns is futile and actually contributes to bad decisions. Timing the market is impossible and those who try are only right 50% of the time. Even if you were to suffer losses in the short term, as the graphs above show, it always works out in the long-term if you hold your nerve.

Please get in touch if you would like to discuss further.

+27 (0)79 551 5988 | tunin.roy@psg.co.za

PSG Old Oak | Tel: +27 (79) 551 5988 | tunin.roy@psg.co.za | psg.co.za

The opinions expressed in this document are the opinions of the writer and not necessarily those of PSG. The information in this document is provided as general information. It does not constitute financial, tax, legal or investment advice and the PSG Konsult Group of Companies does not guarantee its suitability or potential value. Since individual needs and risk profiles differ, we suggest you consult your qualified financial adviser, if needed. PSG Wealth Financial Planning (Pty) Ltd is an authorised financial services provider. FSP 728.

Stay Informed

Sign up for our newsletters and receive information on finance.