Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

25

May 2021

Where to Park Cash Holdings

Tunin Roy

Wealth Adviser

Although it is not wise to hold cash for the long-term, clients do have a need for cash at times. Some clients want to hold cash to express a market or for shorter-term expenditure requirements. Where that is the case, is a call account or bank deposit the best option? Often, the answer is no.

“ Although it is not wise to hold cash for the long-term, clients do have a need for cash at times. ”

I have been advising that clients do not hold significant rand cash allocations for longer periods of time given the sub-inflation after-tax returns offered by the asset class. There are some of the newer banks that are offering attractive deposit rates to attract capital but they may involve significant credit risk. You may remember what happened with African Bank recently. Depositors lost substantial amounts of money when it filed for insolvency. It is worth noting this when considering putting any substantial funds into some of the newer entrants to the SA banking sector.

At the time of the COVID-19 crisis, you will be well aware that the Reserve Bank of South Africa aggressively cut the SA repo rate by 300 basis points (or 3%) to safeguard and stimulate the economy. As cash and money market returns follow the repo rate, bank call and deposit rates also fell to a point where many of the ‘Big 4’ SA banks were offering call rates of below 3% for instantly accessible cash up to a paltry 4% for 12-month money. With the official StatsSA inflation standing at 4.5%, that means a negative real return on cash even before thinking about any tax payable on the interest you earn. So – it is evident that cash should not play a part currently in long-term allocations for the South African investor.

However, some clients want to hold cash to express a market view or for shorter-term expenditure requirements. So, a cash or near-cash allocation has a place where the need arises.

Where that is the case, is a call account or bank deposit the best option? Often, the answer is no.

A cash account is just one of the vehicles available in the fixed income area of the financial markets, which is the lowest risk area of all. A cash account is just an offer to repay your money on demand in exchange for a given interest rate. A fixed deposit is an offer to repay your money at a given date in the future in exchange for a slightly higher interest rate, given the reduced flexibility. When you invest in either, you are taking credit risk on the issuing bank – so in the event that you are using just one bank, your credit risk is concentrated in a single institution.

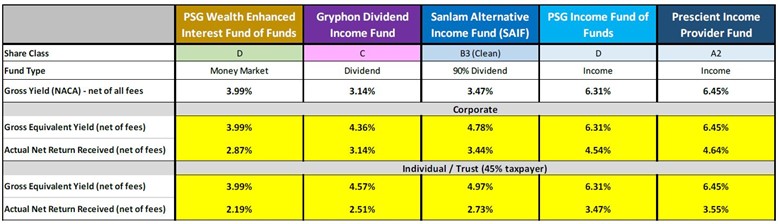

As everyone should be aware, diversification is the only free lunch in investing so by getting exposure to many more institutions, you reduce risk and potentially enhance returns. This is achieved by using a fund where the fund manager spreads your risk over a whole range of borrowing institutions. A fund that invests in cash instruments is called a money market fund. PSG’s flagship money market fund is the PSG Wealth Enhanced Interest Fund of Funds, which has a track record of providing excellent cash returns and beats almost all other comparable funds over multiple periods.

As mentioned above, a term deposit pays a higher rate of interest than an overnight call account. This reflects the fact that you should be paid more for the lower flexibility of the term deposit. To be classified as a money market investment, regulation stipulates that the term of any cash instrument must not be longer than 1 year although most of the instruments in a typical money market fund will not be longer than 3 months. By considering instruments with longer terms than this, you can boost your returns as long as you intend to hold your cash position for long enough to ensure that you achieve your target return. For investors with a sufficient time horizon, a near-cash or income fund would be the best solution. This is a fund that invests in money markets instruments as well as some short-term bonds with sometimes small allocations to listed property and preference shares. By doing this, they offer much higher returns than cash. Our preferred picks in this area would be the PSG Wealth Income Fund of Funds and the Prescient Income Provider Fund.

Finally, it can also be worthwhile to consider your tax position. Dividend income funds deliver returns in the form of mainly dividends by swapping the interest income that they receive with other institutions for dividends. For a higher rate taxpayer or companies without assessed losses or similar deductions, these could also provide the best option for a cash allocation. My pick of these funds would be the Gryphon Dividend Income Fund or the Sanlam Alternative Income Fund. Individual investors would pay a 20% dividend withholding tax charge on the income offered.

Although it is not wise to hold cash for the long-term, clients do have a need for cash at times. Some clients want to hold cash to express a market or for shorter-term expenditure requirements. Where that is the case, is a call account or bank deposit the best option? Often, the answer is no.

With that in mind, I am pleased to provide a comparison of rates currently offered by our market-leading money market fund (the PSG Wealth Enhanced Interest FoF), two dividend income funds (the Gryphon Dividend Income Fund and the Sanlam Alternative Income Fund) which offer returns as dividends which is more tax-efficient for a company or a higher-rate individual or trust taxpayer and two income funds - the PSG Income Fund of Funds and the Prescient Income Provider, which holds shorter- and medium-term bonds to boost returns. In the case of the latter, this means that it is prudent to hold the fund for a minimum of 6 months.

If you, your company or your trust hold cash deposits and would like to beat the returns offered at the bank, please get in touch to discuss further. For larger amounts, we would also be very happy to work on more sophisticated blended solutions based upon risk appetite to achieve the correct return for you.

We can also look at enhancing yields in offshore markets. Our near-cash yield enhancement solutions have delivered 4-5% in USD terms over the last year.

Please contact me for further information.

Tunin Roy

PSG Claremont

tunin.roy@psg.co.za

Tel: +27 (0)79 551 5988

PSG Claremont | Tel: +27 (79) 551 5988 | tunin.roy@psg.co.za | psg.co.za

The opinions expressed in this document are the opinions of the writer and not necessarily those of PSG. The information in this document is provided as general information. It does not constitute financial, tax, legal or investment advice and the PSG Konsult Group of Companies does not guarantee its suitability or potential value. Since individual needs and risk profiles differ, we suggest you consult your qualified financial adviser, if needed. PSG Wealth Financial Planning (Pty) Ltd is an authorised financial services provider. FSP 728.

Stay Informed

Sign up for our newsletters and receive information on finance.