Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

06

August 2021

Our current views on the macro environment - Angles & Perspectives

Greg Hopkins, Deputy-Chief Investment Officer

PSG Asset Management

Our panel of fund managers address some key issues around our macro views and how they feed into our portfolio construction process. Our CIO Greg Hopkins addresses the extreme market conditions and the perceived riskiness of our funds, Fund Manager Shaun le Roux explains why our cash holdings are low despite markets being at all-time highs, and Fund Manager Philipp Wörz delves into the global landscape and the resurgence of value as an investment style.

“ A change in status quo, like tighter monetary conditions or sustained higher inflation, could have a pronounced impact on asset prices. ”

Our current views on the macro environment

Given the wild swings in various asset prices over the past year and a half, and with the future looking particularly uncertain, we interviewed some members of the PSG Asset Management team to expand on how they are seeing the market environment and expressing their views in client portfolios.

Q1: PSG has been highlighting the extreme market conditions for some time. Why do you consider them extreme, and what do they mean for investors?

A1: Greg Hopkins responds.

Financial markets have seen it all over the last few years: a raging bull market in popular global assets, underperforming domestic assets, a dramatic sell-off last year followed by an extraordinarily sharp recovery, unprecedented monetary and fiscal stimulus, and a speculative mania in contemporary ‘investment’ fads. We are currently witnessing intense debate around whether the world should prepare for the return of inflation, and whether we are on the cusp of a commodity supercycle. Alternatively, many expect the disinflationary forces of the past few decades, including the mountains of debt piled on as a response to the pandemic, to keep prices in check. Furthermore, a look into financial markets continues to reveal a very wide chasm between the prices of securities that have outperformed in recent years (and hence continue to dominate portfolios), and cheap, unloved assets. This remains a very challenging investment environment.

Investors will always extrapolate recent experience: selling the underperformers to buy the recent winners. After many years of material outperformance by assets that benefit from the prevailing conditions, complacency sets in: there is no incentive to change your portfolio. Domestic investors have been multi-year sellers of domestic equities in favour of more expensive offshore stocks and income funds. And, global investors have crowded into the multi-year outperformers (US, tech, growth, high quality), a move that has been greatly accentuated by the growing relevance of passive price-insensitive investing. Consequently, the beneficiaries of this positioning have become very expensive, and it is worth reminding ourselves that these are mostly long duration assets and the lofty prices are underpinned by historical lows in interest rates as well as abundant liquidity. A change in status quo, like tighter monetary conditions or sustained higher inflation, could have a pronounced impact on asset prices. It is our view that the price paid for an asset has a material impact on the future returns that are experienced and - in the case of expensive ‘winners’ of recent years - mediocre long-run returns look like the best-case scenario.

In contrast, cheaper stocks, especially in out-of-favour emerging markets, have been shunned for years, and 2020 saw investors capitulating and fleeing to the ‘safety’ of expensive developed market stocks and bonds. This created a unique opportunity for counter-cyclical investing. Despite the fact that we like to take advantage of a crisis and our funds have enjoyed a very strong 15 months, we continue to find very attractive investment opportunities. Our clients own a portfolio of higher quality domestic and global stocks that are very cheap and well positioned for strong multi-year profit growth. This is in sharp contrast to the very elevated prices that dominate most portfolios today. We think investors need to be acutely aware of the prevailing market conditions and the implications for future returns. PSG cannot recall a better opportunity for differentiated active managers than what exists today.

Q2: The PSG funds have excellent long-run track records and the recovery over the past year has been noteworthy, but relative 3- to 5-year performance is still disappointing. Your funds also endured sharp declines in 2020. Is it appropriate to conclude that PSG funds are riskier than better-performing funds or funds with smaller 2020 drawdowns?

A2: Greg Hopkins responds.

Our performance has indeed been remarkably consistent over longer periods – for example, our largest fund, the PSG Flexible Fund, was in the first quartile on a rolling 3-year basis for 89% of the time from 2010 to 2018. This, together with good performance over the last year, has made our longer-term track records generally quite satisfactory. However, it is worth focusing on the performance of our funds in the period leading up to and during the Covid-19 related market sell-off.

Though we did make some mistakes that we have written about in previous publications, we would encourage clients to consider the extreme market conditions and their impact on our consistent investment approach.

The primary risk that we focus on is the risk of our funds not achieving mandate objectives for our clients. Our track record has been built on sensibly and patiently using market conditions to increase the chances of achieving these objectives. In practice, we tend to buy more when the prices of assets we favour decline, and sell when prices rise sharply. Often, we hold high levels of cash while waiting patiently for market conditions to provide a better entry point. The past few years have been characterised by cheap stocks getting cheaper (especially in SA) and expensive mega-cap stocks powering indices to all-time highs.

This is not a favourable investment environment for our process and underperformance is to be expected, as was the case for other price-sensitive or value investors around the world.

Unfortunately, for investors in funds heavily exposed to cheaper assets, the Covid-19 meltdown amplified pre-existing conditions: cheap stocks offered limited protection and were among the worst performers. Indeed, the March 2020 drawdown was a bitter pill to swallow for clients that had already endured underperformance.

However, during those dark days of last year, we were at pains to communicate that we expected the losses to prove temporary – which they did – and that the indiscriminate selling gave rise to seldom seen opportunity to improve the chances of achieving client objectives. A collapse in confidence led to volatile markets and deeply depressed prices. The gap between the intrinsic values of our investee companies and prevailing share prices – the margin of safety – widened to levels last seen in 2009. So, we argued that the riskiness of our portfolios had actually been reduced. Today, the average stock in our funds continues to trade at a wide margin of safety and we continue to believe that our funds offer a lower-risk chance of producing acceptable client outcomes in the long run.

We do not believe that it is appropriate to conclude (on the basis of recent experience) that our process is riskier than most others. Our focus on margin of safety and our desire to avoid permanent capital loss provide a measure of protection against risk and volatility. What we have witnessed, however, is a very tough period for our investment style, which was compounded by the unique extraneous shock of the pandemic.

Q3: You mention markets powering to all-time highs. Surely, your clients should expect you to be more conservatively positioned under the circumstances? Your funds appear offensively positioned. Why is this appropriate and why are you confident about your portfolio holdings?

A3: Shaun le Roux responds.

This is an accurate observation – markets are high but our cash levels are low. We caution our clients to expect large cash holdings in our multi-asset funds when markets are expensive, as they are now. However, we currently have low levels of cash and are very optimistic about the long-term return expectations for our funds from here. This is because our buylists are full and are expressing a high conviction in our stock ideas. We just happen to be looking in out-of-favour areas for ideas.

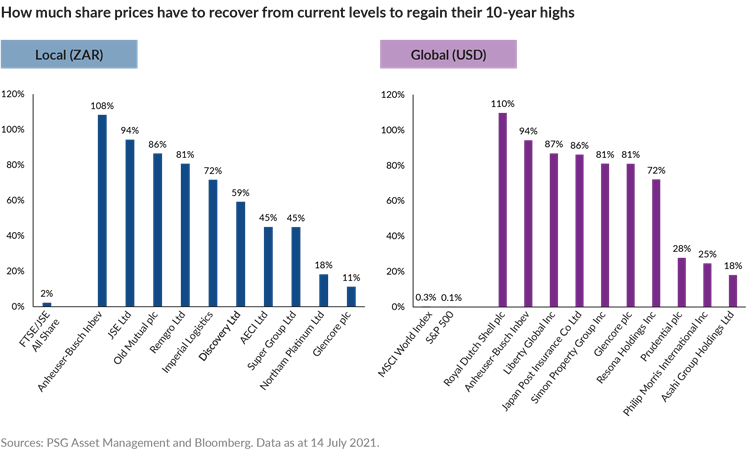

As this chart shows, most of our highest conviction domestic and offshore portfolio positions can be bought at a wide discount to the highs of recent years. Consequently, upside remains material should they recapture those highs, and we see no reason why most should not do so. Indeed, most global stocks were in a bear market before Covid-19 and the pandemic induced a climactic capitulation out of cheap, unloved stocks that were perceived to be excessively risky. Despite a sharp recovery, most of our best ideas remain very cheap. This is in sharp contrast to global indices that have been trading at all-time highs largely due to expensive mega caps.

We think it is highly unlikely that the winners of the past few years that have outperformed so handsomely, will prove to be the winners over the next few years. When we look into our portfolios, we have high confidence that our clients own the winners of the future. The combination of quality business models and management teams, depressed share prices, strong balance sheets and great prospects for multi-year profit growth bodes well for future returns.

Q4: Please provide us with insights into the global landscape. We have seen a resurgence in the performance of ‘value’. Is it sustainable and where is PSG finding opportunities?

A4: Philipp Wörz responds.

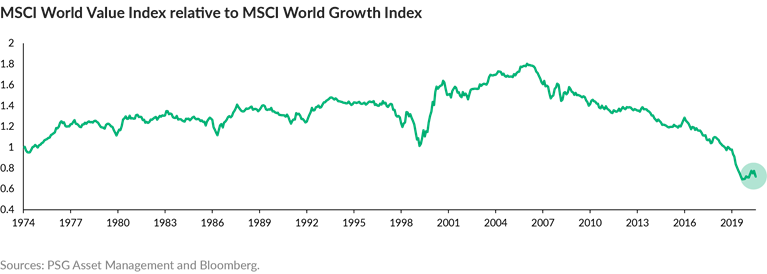

As you point out, value stocks have finally had some time in the sun after a long winter – growth has outperformed value for 13 years. But, as the chart below shows, the recent outperformance by value hardly features on long-term charts.

At PSG, we are value managers in the sense that we care about the price we pay in a market that has become increasingly price agnostic. We are currently finding far more opportunities in the cheaper part of the market and hence have a strong value tilt.

There is intense debate at the moment as to whether the world is about to transition from being dominated by disinflationary forces to a new era of inflation. The consensus argument is that for value investment to work, inflation needs to set in. This is a very complex topic, especially as we find ourselves in unprecedented times with ultra-loose monetary and fiscal policy juxtaposed against very high levels of global debt. We are extremely cautious of orientating a portfolio to an explicit macro prediction, as we appreciate the unpredictability of future macro outcomes and acknowledge the challenge of getting the timing right in a market with a very short time horizon. Instead of making explicit forecasts, we have reviewed our portfolios and other investment opportunities considering the risks associated with different macro scenarios.

We have concluded that while the possibility of future inflation has been attracting headlines, the bulk of the money remains positioned for a continuation of the old regime of low inflation. This is reflected in US$14.6 trillion of negative-yielding bonds and the elevated prices of the most widely held global equities, which are very long duration assets.

We argue that elevated starting valuations significantly reduce the likelihood of acceptable returns from the perceived beneficiaries of sustained low levels of inflation. Conversely, even though people are talking about the possibility of inflation proving to be anything but transitory, the assets that provide protection against such a scenario are cheap. We think many of the global stocks we own are set to deliver satisfactory returns even if inflationary pressures prove to be transitory. Importantly, they will do especially well in a world of sustained higher prices, effectively offering free leverage in (and protection against) a transition to an era of higher inflation.

We think that the extremes of financial markets provide the opportunity to buy the winners of the future: cheap companies with strong pricing power and recovering end markets. Hence, we think that a carefully selected portfolio of ‘value’ opportunities has the ingredients to outperform on a multi-year basis. The team has been able to identify solid global investment ideas that are more idiosyncratic in nature and are not beneficiaries of passive flows or low interest rates. We have bought cheap stocks in the UK (27% of PSG Global Equity) and Japan (16%), and large parts of our exposure to the US are in more typically overlooked ideas such as Simon Property Group, Liberty Global with operations in the UK and Europe, and Philip Morris, the owner of Marlboro outside the US.

We remain committed to engaging with our investors, and answering their pressing questions. Remember that you are always welcome to contact us if there are questions you would like us to address in future editions of this publication.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

In this edition, we continue to look beyond the surface to find opportunities for our clients. Research and critical inquiry are part and parcel to our research process, and inform our differentiated positioning. We consider the macro views that form a backdrop to our fund positioning, unpack what ESG investing could mean for the current commodity run, and expand on our unique approach to the opportunities in the SA Inc. space.

Read moreIntroduction - Angles & Perspectives Q2 2021

Our value proposition to investors is to seek out great companies that are underappreciated by the market. We believe that if we buy such companies at a discount to their intrinsic value, they are likely to appreciate significantly in value in the long run. But markets, economies and companies are not static: conditions evolve on a daily basis, and what seems like a simple endeavour in theory, becomes a complex one in practice.

Read moreWeighing up the investment case for commodity stocks - Angles & Perspectives

In this article, we weigh up the investment case for commodities given current market conditions. Commodity companies are prone to boom-and bust cycles, and there is currently much debate around the sustainability of the current run-up in commodity prices. The team weighs in on how factors like decarbonisation, the environmental, social and governance (ESG) investing phenomenon and a renewed focus on capital discipline are impacting the commodity cycle.

Read moreA differentiated approach to investing in SA equities in turbulent times - Angles & Perspectives

While many investment managers are coming around to our long-held view on the potential of the local market, we are in a unique position to exploit opportunities around SA Inc. shares. Fund Managers Shaun le Roux and Justin Floor unpack our approach to ensuring broader exposure to SA Inc. shares.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.