Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

05

August 2022

Capitalising on the ‘big unwind’ – picking stocks that are fit for the future - Angles & Perspectives

Shaun le Roux, Fund Manager

Asset Management

The unwinding of market distortions of this magnitude will have a dramatic impact on future market returns. However, there will be beneficiaries of this process and we believe differentiated managers in particular are well-positioned to exploit them. We see clear opportunity for multi-year gains from some of the areas we highlight in this edition.

Capitalising on the ‘big unwind’ – picking stocks that are fit for the future

Global financial markets became very distorted over the past decade. These distortions are in the process of unwinding – a process we expect to take several years. This environment should reward differentiated stock selection. This article discusses some of the areas where we can identify good long-term opportunities for our clients.

So far, 2022 has been a brutal year for both risk assets like equities and perceived low-risk assets like developed market (G7) government bonds – in June, the S&P 500 Index found itself 23% lower than it started the year and holders of US 10-year bonds lost 14% over the same period. Currently, significant fear is building that hawkish rhetoric from the US Federal Reserve (the Fed) implies that they will aggressively raise the federal funds rate to levels that will stem rampant inflation, but tip the US (and other economies) into recession. The prices of cyclical sectors and commodities have fallen sharply in recent months, suggesting that markets are increasingly pricing the likelihood of a sharp global contraction.

We believe that investors are well served by zooming out of shorter-term fears and assessing the bigger picture backdrop to make sense of how to navigate these uncertain times. Here, we identify a number of sizeable market distortions that have built up in recent years and that have had a profound impact on asset pricing. It is important to acknowledge the effect that the unwinding of these distortions will have on asset class returns over the next five years and more. We think it will be challenging to generate satisfactory real returns over this period if an investor fails to appreciate the magnitude of these distortions and the impact of the unwind. Furthermore, a robust bottom-up equity selection process provides valuable insights into the fundamentals and valuations of individual companies, making it possible to identify stocks that are attractively priced and not reliant on the continuation of these distortions. Indeed, we think differentiated stock pickers should come to the fore in the years ahead.

Five factors have recently had a dramatic impact on asset prices

These are:

- Very cheap money – the extremely low cost of capital and negative real rates in the developed world have supported high prices of financial assets.

- The rise of passive investing – a fundamental reallocation of funds towards the winners of the past at the expense of the losers. Notably, most portfolios have materially drifted closer to benchmark indices, upweighting winning funds and stocks at the expense of poorer performers.

- The ESG movement – capital has been redirected away from perceived ‘bad’ industries to ‘good’ industries, in most cases with limited consideration of the unintended consequences.

- Capital flight from South Africa – both foreigners and locals have drastically reduced exposure to domestic assets in recent years, in favour of some of the beneficiaries of global market conditions.

- Fiscal stimulus – initially in the form of tax cuts, but more recently via vast cash payments to counter the impact of the pandemic. Historically, fiscal spending has been focused on expanding productive capacity and infrastructure. This time, the injections primarily funded private consumption and savings.

The result has been profoundly distortionary effects in financial markets

Some of the effects we have seen play out include:

- Misallocation of capital away from productive parts of the economy towards the perceived beneficiaries of this environment, including ‘hot’ areas such as tech and renewables.

- A severe mispricing of risk where a vast array of financial assets that derive much of their value from negative real rates had seen their valuations soar (long duration assets).

- Rampant speculation fuelled by high levels of liquidity stimulus cheques, and zero-commission trading for retail investors. Bubbles or manias developed in various pockets including cryptocurrencies, unprofitable tech, special purpose acquisition companies (SPACs), meme and story stocks like Gamestop and Tesla.

- Extraordinarily wide divergences in valuations between the winners of this environment and the assets where capital was exiting.

- Underinvestment in many productive parts of the global economy including infrastructure, supply chains, most of the energy complex, and raw material capacity.

- The emergence of strong and pervasive inflationary pressure as the world realises that misallocation of capital and aggressive expansion of the monetary base have given rise to ‘too much money chasing too few goods’.

Distortions of this magnitude will not unwind in a matter of months

Our 3M stock selection process aims to identify good businesses where the market is under-appreciating their inherent quality, and which can be bought at attractive prices. This tends to happen in times of fear and/or when stocks have endured challenging market conditions. In countries or industries that have been starved of capital, we have witnessed the combination of tough end markets for several years and very low valuations. Furthermore, Covid-19 restrictions have weighed heavily on certain sectors and geographies, many of which are yet to enjoy the benefits of normal trading levels. A stark contrast can be drawn between stocks that have endured tough times for many years (and which are very cheap) and the beneficiaries of the market distortions described earlier. We argue that multi-year trends are underway that will strongly favour certain assets, and that the beneficiaries of the market distortions (the winners of the past) are less likely to produce satisfactory returns and are riskier than is commonly perceived.

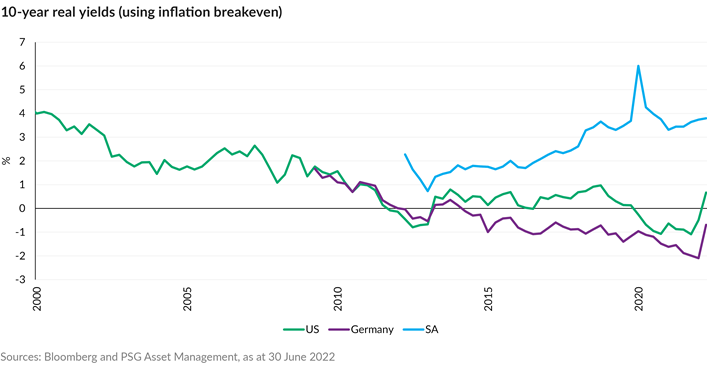

This is demonstrated in the graph that follows. It contrasts the real yields in South Africa with real yields in the US, UK and Germany using 10-year bonds and inflation breakevens (which reflect medium-term sovereign inflation expectations). You will observe the steady decline in real yields in the West to the deeply negative levels of 2021. Notably, these yields were negative before inflationary pressures fully emerged. Conversely, real yields in South Africa (and similar emerging markets) have been high and rising over the past seven years. This shows how domestic SA assets are already factoring in high costs of capital – meaning the valuations of domestic bonds and equities are already depressed, making them far less susceptible to rising global real yields. Witness the relative performance of SA versus US or European stocks in 2022. Through this lens, SA stocks are the lower-risk proposition in a rising global real yield environment.

Unwinding imbalances are likely to reward local investors

The clamour to exit SA assets built from 2015 and reached fever pitch during the Covid-19 pandemic. The prevailing narrative during 2020 was that a fiscal cliff was imminent and SA Inc. was uninvestable. We saw this as a very favourable environment for taking a differentiated view and investing in good domestic companies that should provide acceptable returns even in tough economic conditions – mainly because starting valuations were so low. The market has applied a very high risk premium to South African and other emerging market assets. A further liquidity risk premium is being overlayed on domestic small and mid-cap stocks. Thus, valuations for smaller domestic counters have attained deep crisis levels in recent years, especially during the panic of 2020. We argue that PSG Asset Management has a competitive advantage in the domestic mid-cap universe: our relative size allows us to invest outside of the narrow large cap universe and we conduct proprietary research on a number of companies that have little or no sell-side coverage at present.

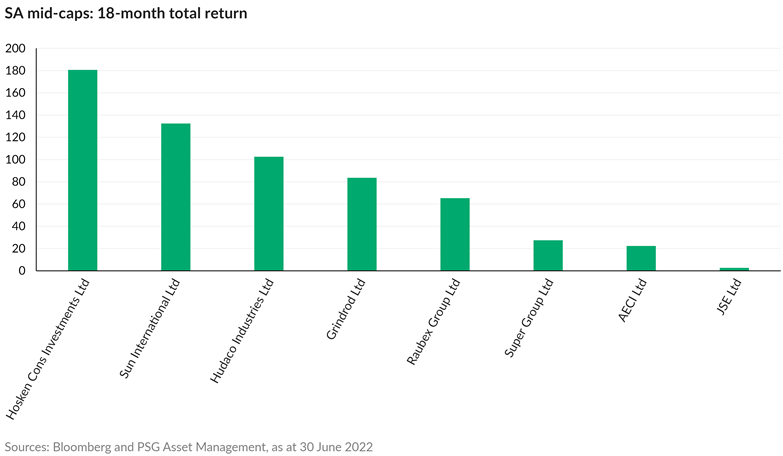

Our funds are not constrained by benchmarks that are dominated by a handful of well-owned large caps, and mid-caps have been positive contributors to long-run outperformance. While this opportunity set has been a headwind to performance between 2015 and 2020 for the reasons described above, it is pleasing to note that in such a favourable environment for stock picking some of our higher conviction mid-caps have started delivering pleasing returns in recent times. The graph that follows shows the 18-month returns of our largest mid-cap positions. In what has been a challenging economic climate given pandemic restrictions, the KZN riots and supply chain bottlenecks, a number of our investee companies have delivered commendable and resilient profit performance, which the market has started to recognise. In such an unloved arena in global financial markets, the market seems only prepared to reward strong performance when it is very visible. We would be disappointed if the names shown here did not positively surprise the market in the years ahead, and if they are afforded a more reasonable valuation our clients should enjoy very strong returns from this part of the portfolio.

It is noteworthy that we own between 5% and 10% of the companies above. Collectively, they represent 24% of the PSG Equity Fund as at the end of June 2022. These positions have been built in tough times and at depressed valuations.

Shorter-term market developments do not negate our longer-term views

As would be expected, cyclical stocks have sold off with global recession fears ratcheting up in recent weeks. These have included material and energy companies that had been the year-to-date outperformers in otherwise weak global stock markets. Commodity prices have been very buoyant in 2022 – in many cases supported by disruption from the war in Ukraine and sanctions against Russia – though recent sharp declines suggest looming concerns around the impacts that a hard landing of the global economy will have on demand for raw materials. Global financial markets moved aggressively to price the likelihood of such an occurrence in June. While our macro analysis suggests that a near-term recession is hardly a foregone conclusion, our bottom-up research is primarily focused on understanding the supply-side fundamentals of capital-intensive industries like mining and energy. It is clear to us that after a long period of underinvestment in capacity, we have entered an era of scarcity in certain commodities as well as many sources of energy. We retain our belief that higher than average commodity prices (and strong returns to shareholders) are likely to persist until the supply side responds (which will take several years in most cases). Accordingly, we continue to see attractive long-term returns from the commodity names that our clients own. However, we do anticipate sustained price volatility while the market wrestles with the shorter-term demand implications of tightening financial conditions. Currently, our domestic funds own both JSE-listed and offshore commodity shares. In a world that suits stock pickers, we are looking to optimise this opportunity by investing in the commodities and companies that best meet our criteria. For example, we have healthy exposure to both energy and shippers in our domestic funds, but most of this exposure is via direct offshore equity exposure in oil and gas majors or drillers, as well as dry bulk shippers and product tankers.

Unwinding imbalances will have profound impacts on the future investor experience

We have laid out a case that the unwinding of market distortions of this magnitude will have a dramatic impact on future market returns. There will be beneficiaries of this process and we see clear opportunity for multi-year gains from some of the areas described above. However, patience will be required and volatility will have to be endured. For unconstrained investors like ourselves, this should be a favourable environment.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

In this edition, we passionately position our case in favour of differentiated investment management and share insights into how these views are reflected in the portfolios. Despite the challenging investment environment ahead, we believe we are in the process of seeing some great investment prospects unfolding for patient long-term investors. In the first article, Fund Manager Shaun le Roux argues the unwinding of distortions will have a dramatic impact on fund returns in the year ahead. Nonetheless, there are some appealing prospects for differentiated thinkers. Fund Manager Philipp Wörz and CIO Greg Hopkins highlight the concentration we have seen in fund positioning, and offer compelling arguments why differentiated managers bring benefits as part of a diversified portfolio. Lastly, Fund Managers Philipp Wörz and Shaun le Roux unpack how the abundance of opportunities we see are incorporated into our portfolios.

Read moreIntroduction - Angles & Perspectives Q2 2022

The world is slowly waking up from a decade of excesses fuelled by easy money and low interest rates. The pending unwind is bound to be both protracted and painful. Despite the challenging investment environment ahead, we believe we are in the process of seeing some great investment prospects unfolding for patient long-term investors.

Read moreWhy global investors need to consciously seek out differentiation during the ‘big unwind’ - Angles & Perspectives

Our research has highlighted a high degree of concentration in fund positioning, even as it becomes clear that continuing to favour strategies that have worked in the past is likely to come at the expense of future portfolio growth. Given the environment we see ahead, we believe differentiated managers bring important benefits as part of a diversified portfolio.

Read moreGrowing capital during the big 'unwind' – positioning for growth - Angles & Perspectives

To grow one’s capital in the years ahead, investors will have to look through the noise and adopt a long-term perspective. In this article our fund managers share how the abundance of opportunities we identify as part of our 3M process informs our fund positioning.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.