Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

05

November 2021

Multi-asset fixed income funds: Risk management when the rules are the same, but the game has changed - Angles & Perspectives

Ané Craig, Fund Manager

PSG Asset Management

2021 is showing signs that four decades of declining global interest rates and inflation are coming to an end. A major cycle inflection changes the game for fixed income investors. It will become more and more difficult to earn inflation-beating returns while sticking to the rules of the game, being low levels of risk. In this case, the obvious question fixed income investors should be asking themselves is whether their strategy and toolkit are appropriate for a future that will look very different from the past.

“ The obvious question fixed income investors should be asking themselves is whether their strategy and toolkit are appropriate for a future that will look very different from the past. ”

Multi-asset fixed income funds: Risk management when the rules are the same, but the game has changed

2021 is showing signs that four decades of declining global interest rates and inflation are coming to an end. A major cycle inflection changes the game for fixed income investors. It will become more and more difficult to earn inflation-beating returns while sticking to the rules of the game, being low levels of risk. In this case, the obvious question fixed income investors should be asking themselves is whether their strategy and toolkit are appropriate for a future that will look very different from the past.

What global reflation means for South Africa

In his article Thriving in a major market inflection depends on duration and mandate Head of Research, Kevin Cousins, details how higher and stickier inflation than what we’ve experienced in developed markets over the past decade has to do with much more than just the base effects of 2020. Developed market inflation is likely to exceed the 2% experienced over the past 10 years. But as Fund Manager Lyle Sankar points out in Major market inflection points: Thinking about portfolios for the next decade, we should not necessarily expect higher than average inflation in South Africa at the same time.

Several important developed market inflation pressures are not present in South Africa. House prices are rising globally, yet house price and rental growth in South Africa are still below 2%. Covid-19 has left millennials and Gen Xers across the pond reassessing priorities and branding 2021 as ‘The Great Resignation’ (4.3 million Americans or 2.9% of the labour force resigned in August). Add reduced cross-border mobility and you can see why wage price inflation is climbing in the developed world. With unemployment at 34% and National Treasury more resolute than we have seen it in years to curb the public sector wage bill, our wage inflation outlook could be quite different to history, as well as to the developed world. South Africa will face similar food and fuel price pressures to those of the rest of the world, though increased commodity prices will be GDP-growth positive for us and could offset some ‘imported inflation’ through a weakening currency.

More important than the divergent practical realities impacting the inflation differential between South Africa and developed markets, is the South African Reserve Bank (SARB). The SARB has built up credibility over the past decade and succeeded in lowering inflation expectations. Anchoring inflation expectations is incredibly powerful in lowering actual inflation, because expectations drive wage negotiations, longer-term funding costs for businesses (which pass on costs to consumers), rental negotiations and more.

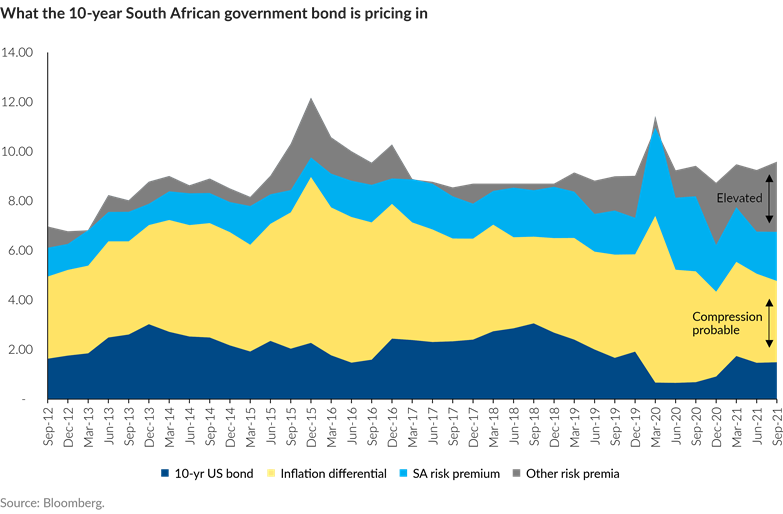

Global inflation above the 2% average that we have grown accustomed to, and local inflation more consistently around the 5% average experienced post the Global Financial Crisis, should be very positive for South African government bonds. Combined with a country risk premium that also looks overstated, we argue that South African government bonds carry less risk than they have in the past whereas developed market bonds (sovereign and corporate) are considered riskier now.

Tools required to beat inflation without increasing risk

Can investors accept the typical multi-asset fixed income fund positioning to give them inflation-beating returns at the same level of risk as during the last decade? Not likely.

The traditional portfolio has the key ingredients of cash, corporate bonds (credit), South African government bonds and listed property. As we argue in Major market inflection points: Thinking about portfolios for the next decade, investments into cash and cash-like instruments could generate low real yields for a prolonged time. Similarly, credit is expensive, with many of the lowest risk (bank) bonds offering investors negative real yields.

Highlighting the attractive opportunity in local government bonds and lamenting how expensive the local credit market has become, is hardly contrarian or new. However, it is worth pointing out that there has simply been less supply of credit since 2018, and particularly since the start of the pandemic. Investors have therefore not necessarily been actively selling their expensive holdings of corporate bonds, as we have over the past three years, but have simply not been able to invest to the same extent as in the past. Oversubscribed auctions of corporate bonds and continuously tightening credit spreads indicate that investors are still buying corporate bonds and are increasingly giving up returns for the same level of risk - at best. This shows that credit is seen as a critical part of some portfolios ‘all the time’, as opposed to ‘at the right time’. With issuance lacking, we have also noted an increase in investments in structured notes. Our process places a high bar on investing in instruments that sacrifice liquidity or introduce pricing opacity.

If real yields aren’t available in cash or credit, investors may be tempted to increase their exposure to ultra-long-dated SA government bonds, which are offering near 6% real yields. Within the lower risk income mandates we limit our interest rate (or duration) risk and prefer the real yields of 3% at the 5-year point and 5% at the 10-year point of the government bond curve. In the absence of increased interest rate risk or the customary level of credit enhancement, multi-asset income portfolio returns could disappoint, as the remaining building block of the traditional toolkit, listed property, is also no longer the sweetener that it has been in the past. While some investors may need to look at asset classes beyond their traditional toolkit to achieve the required real returns, we benefit from a single investment process across asset classes which the PSG Diversified Income Fund has been able to use since inception.

Rely on a consistent process to give you a differentiated portfolio

At PSG, we conduct bottom-up research on every security we invest in. We rely on a tested 3M process where we look for real returns and quality on sale, focusing on a company or bond issuer’s moat, its management, and the margin of safety of the investment. Property is assessed through this same process, and the risk-adjusted return of listed property is compared to that of the equities we consider. Consequently, the PSG Diversified Income Fund, which can hold up to 25% in listed property, often does not invest in property at all. Since inception, the fund first invested in global property stocks in 2018, whereas local property stocks only made it through our investment process from 2020. Only our best ideas make it into our funds, and having an established global process means that we weigh domestic listed property against global property as well as global equities (the PSG Diversified Income Fund has an offshore limit of 30%).

The headwinds to the domestic listed property sector are well documented – high levels of vacancies, decreasing rental values on new leases and tenant incentives such as lengthy rent-free periods mean that real annual rental growth is now the exception and no longer the norm. Without predictable and growing dividend yields, many SA property stocks are much closer to equities on the risk spectrum than they are to traditional real estate income trusts (REITs). High leverage in the sector further increases the risk profile of these stocks, with few prospects for the bulk of the sector to meaningfully reduce gearing in the near term. There is not enough appetite from buyers to execute large portfolio asset sales, raising equity to reduce debt is not an option for most counters that trade at large discounts to net asset value, and not enough earnings can be retained to reduce debt due to REITs being required to distribute 75% of earnings.

We therefore have been, and remain, very selective when investing in this space, gravitating to stronger balance sheets and quality assets that we could acquire cheaply during the Covid-19 sell-off. Locally, we are invested in Resilient REIT. Resilient’s portfolio of peri-urban and rural retail assets has been supported incredibly well by consumers visiting these centres to buy essential goods in areas that do not suffer from the dense competition seen in urban retail, where shopping centres are competing with each other as well as facing the small but growing threat of online retail. The type of retail that Resilient owns, is structurally more durable and run by best-in-class property managers. The ESG profile of the stock has also changed completely. In 2017, complicated investment structures and enterprising empowerment schemes raised flags of conflicts of interest and aggressive accounting. In 2021, a much simpler structure, better disclosure, enhanced governance policies and a stronger board meant that Resilient scored well in our management assessment. Adding to the attractiveness of the stock is the roughly 9% forward dividend yield.

As we believe local property opportunities to be limited, we have preferred allocating capital to global property companies such as Tanger Factory Outlets. Tanger is a niche player in US and Canadian outlet centres, and is the only specialist Premium Outlet REIT. It is considered one of two players that dominate the outlet sector, faces much less competition than other types of brick-and-mortar US retail such as malls and department stores, and has proven the post-pandemic relevance of its portfolio of open-air outlets stocking premium brands at discounted prices.

Through the single investment process highlighted earlier, the PSG Diversified Income Fund is able to invest in equities (up to 10% together with preference shares), where we can tailor our stock selection to the fund’s lower risk profile. We are attracted to characteristics such as strong and growing cash flows (AB InBev), healthy debt profiles (JSE), low price-to-earnings ratios (AECI) and attractive dividend yields (Exxaro), with much of our equity buy list standing to benefit from higher inflation as well. We believe that measured exposure to equities such as these improves the return profile without compromising on the overall risk management of the fund.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

The investment landscape has changed dramatically since the beginning of the Covid-19 pandemic. We believe markets have reached an inflection point, with deep consequences for how we construct portfolios going forward. In this edition, our panel of experts debate a range of issues centred around this topic. Long and short duration assets can be expected to yield very different outcomes than over the past 40 years, which will be problematic for investors and portfolio constructors who cling to what has worked in the past. This challenge is likely to be especially pronounced for fixed income investors, who will need to reconsider their investment toolkit to ensure they are well positioned to continue meeting their objectives.

Read moreIntroduction - Angles & Perspectives Q3 2021

We have been writing about the phenomenon of built-in extremes within the same system – in this case the market – for some time. The discerning investor seldom sees the market as one entity and realises that from time to time, bifurcations may occur. This fragmentation into quite distinct parts can occur slowly at first, initially creeping into the system almost unnoticed, but eventually manifesting itself in stark and undeniable ways. This offers both risk and tremendous opportunity.

Read moreThriving in a major market inflection depends on duration and mandate - Angles & Perspectives

Why is the bifurcation between long duration and short duration assets important now? Long duration assets have earned their high weightings in benchmarks and dominant positions in investor portfolios through many years of delivering good returns. However, after 40 years of declining interest rates and inflation, the world appears to be at a long-term inflection point. Anchoring on what has worked historically through big market inflection points, is immensely risky for investors. The ratings of long duration assets, as highlighted below, imply a continuation of the current cycle for many years into the future. Should that outlook be incorrect, very substantial capital losses may ensue.

Read moreMajor market inflection points: Thinking about portfolios for the next decade - Angles & Perspectives

Conditions have changed substantially over the past 18 months, and we believe the weight of the evidence suggests that the market has probably reached an inflection point. In our view, the probability has shifted towards a more reflationary global backdrop, which the market is not yet pricing in. This is likely to have wide implications when considering asset classes that performed well over the last decade, and those that can be expected to deliver real returns at appropriate levels of risk over the next decade. Accordingly, fixed income investors need to review their strategy and explore the benefits of multi-asset income funds for generating real returns at low levels of risk.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.