Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

24

January 2022

Barbarians at the gate: JSE mid-caps on the shopping list - Angles & Perspectives

Justin Floor, Head of Equities

Asset Management

It is becoming increasingly apparent that there is something valuable hidden on the JSE. The last while has seen a notable surge in activity from private buyers signalling that they see opportunity in JSE-listed mid-cap companies. Private equity, industry players (particularly foreign companies) and even some management teams are taking listed companies off public markets. This zeal and optimism contrasts with the prevailing sentiment we are still observing on the JSE: many smaller, domestic-oriented companies trade below their reasonable fundamental value and pessimism and disinterest continue to prevail.

“ We are focused on the complete spectrum of the investment cycle. ”

Barbarians at the gate: JSE mid-caps on the shopping list

It is becoming increasingly apparent that there is something valuable hidden on the JSE. The last while has seen a notable surge in activity from private buyers signalling that they see opportunity in JSE-listed mid-cap companies. Private equity, industry players (particularly foreign companies) and even some management teams are taking listed companies off public markets. This zeal and optimism contrasts with the prevailing sentiment we are still observing on the JSE: many smaller, domestic-oriented companies trade below their reasonable fundamental value and pessimism and disinterest continue to prevail.

We are not surprised that offers are being made for our portfolio companies

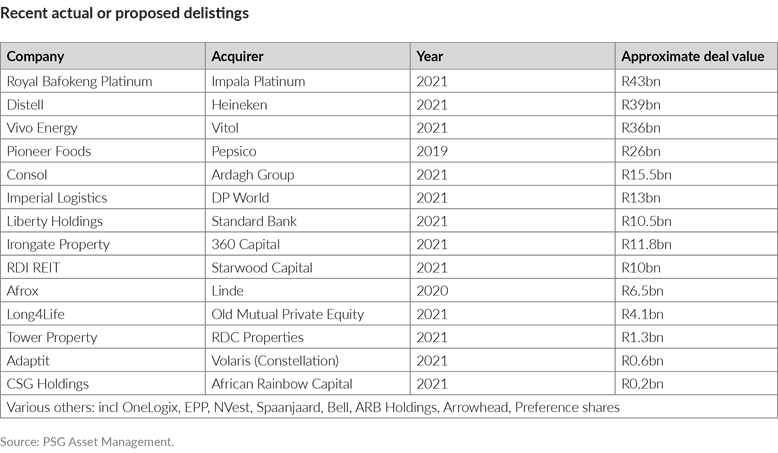

Regular readers will know that we have seen value in SA mid-cap shares for a while now, and it is not unexpected that offers are being made for several of our portfolio companies. Imperial Logistics (shareholders have accepted an offer from global logistics company DP World), Distell (to be delisted by Heineken in partnership with Remgro), Pepsico’s 2019 purchase of Pioneer Foods, and recent offers for Royal Bafokeng Platinum and Long4Life are notable examples of takeover interest in our portfolio holdings. Additional case studies include Standard Bank buying out minority interests in its Liberty insurance subsidiary, Vitol’s offer for Vivo Energy, and many more as shown in the table below. Occasionally, the interest is in specific assets, and not the entire company. For example, Omnia, Zeder, and Mondolez’s approach to AVI stand out.

These assets are being targeted for good reason

There are several reasons why these shares are tempting private buyers:

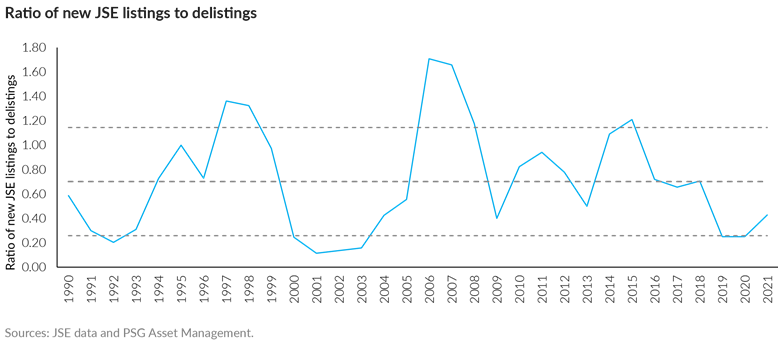

- Firstly, we are at a very favourable part of the cycle. Sentiment and confidence are still low, and therefore prices and valuations are probably still too pessimistic. The graph below shows the ratio of new listings to delistings on the JSE. A ratio of less than 1 indicates a net reduction in listings. The ratio is lower when confidence is weak, and prospective returns are often very good from these low points. Conversely, beware when there is exuberance in the market and net listings are strongly positive. Domestic equities put in a very poor subsequent run following the last cyclical peak in 2015. With elevated delisting and few IPOs to compensate, the ratio is currently very low. Interestingly, this apathy on our stock exchange stands in sharp contrast to the elevated exuberance evident in the flurry of initial public offering (IPO) activity, particularly in US markets.

- Secondly, these buyers are rational and are seeking the same attributes that we target through our own 3M investment process: companies with competitive advantages (moats), that are well managed and well capitalised. And the price needs to make sense (or offer a margin of safety).

Thirdly, private and industry buyers have a powerful competitive advantage of their own: they are plugged into the true economy, with all its very real challenges, and have the confidence to buy businesses to delist them, removing the feedback from high-frequency price data and its corresponding volatility. This allows them to be opportunistic and to take a truly long-term approach. They do not care about benchmarks or relative performance. They just want a good deal. These competitive advantages are powerful and our investment process seeks to replicate them to the extent that we can as public market investors

These developments offer external validation of our investment thesis

We are encouraged by this external validation of our investment thesis in many of the stocks we hold. The existence of new buyers on the scene is a fresh development, particularly in companies that have been neglected for some time. As in previous cycles such as the early 2000s, we suspect they signal better times ahead and a recovery in confidence.

However, situations like this are not straightforward cases of selling with relief at the first sign of an offer to buy our shares at a premium to the prevailing (low) share price. We have a duty to realise fair value for our clients and, given the prevailing market sentiment and low prices of South African assets in general, we face considerable risk that our clients will sell too early and at too low a price, losing out on what can be a multi-year period of precious, life-changing returns.

We have a deliberate and thoughtful approach to maximising client value in case of a takeout offer

At PSG Asset Management, we are in the position of being large enough to take influential stakes in smaller companies, while not being too big to make these smaller opportunities too meaningful in our clients’ lives. In many cases we are one of the top institutional shareholders where we own 5% to 15% of outstanding shares. While we can be influential and have an important voice, we are often not large enough on our own to singularly force an outcome, like blocking an offer to buy a company through a scheme of arrangement.

In a market there is a democracy of perspectives, and it can happen that fellow shareholders have shorter time horizons or do not share our opinion of the long-term value of the companies we collectively own. One of the roles we play is to engage responsibly with fellow shareholders and the market, and to make our case.

Equally, the role of the board of directors is vital, as they are the body ultimately empowered by our clients (the owners) to represent shareholder interests. This must include careful thought about the value of the company they represent and whether any offer is in fact a fair reflection of its true potential, measured over an appropriate time horizon and adjusting for any bouts of overly depressive sentiment. Our engagements with the boards and executive teams are critical components of our ESG proposition on behalf of our clients, and have demonstrable relevance to their economic best interest as well.

The above approach tilts the odds in our favour and is one we recently employed during DP World’s offer for our Imperial shares. Ultimately, however, the only two components of this story that we can fully control are exercising our proxy votes in a way that puts our clients first, and buying good companies at good prices in the first place. We strive to do both well.

A focus on the full spectrum of the investment cycle

It does not surprise us that private buyers are seeing value in our smaller companies, even while other public market investors remain somewhat disinterested or pessimistic. Indeed, we expect more announcements and delistings in the future.

We are focused on the complete spectrum of the investment cycle. The risk of selling too early and at too low a price is one we worry about, and we apply considerable effort in achieving a fair and an appropriate investment outcome when we sell. The smaller companies that we own on behalf of our clients are a valuable component of our current portfolios and are difficult to replicate in large asset management firms. We aim to fully exploit this opportunity.

PSG Asset Management is a wholly owned subsidiary of PSG Konsult Group.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

In this edition, we debate why it is important that fund managers differentiate themselves, and then explore how our funds deliver on this imperative. In the first article, Fund Manager John Gilchrist outlines how our 3M philosophy empowers us to deliver long-term outperformance to our clients. Next, Fund Manager Justin Floor finds validation for our views in the recent flurry of interest in mid-cap companies on the JSE. Lastly, Fund Manager Philipp Wörz argues that despite the perception of global markets being expensive, opportunities remain for selective investors using a differentiated approach.

Read moreIntroduction - Angles & Perspectives Q4 2021

Investors often resort to mental shortcuts and rules of thumb to speed up decision-making, and tend to extrapolate the recent environment into the future. This encourages a binary outlook (value vs growth, e-commerce vs bricks and mortar) and, as investors pile into what has worked in the past, markets can be driven to extremes. Taking a view that is different from the consensus outlook can be challenging and may seem foolhardy, especially if anomalous market behaviour persists longer than expected. However, this behaviour also creates opportunities for patient investors who are willing to look beyond such oversimplifications and question prevailing narratives. We would also argue that this approach is essential to assuring long-term outperformance.

Read moreOnly the start of an anticipated outperformance cycle from our differentiated approach - Angles & Perspectives

Fund managers need to approach the world differently from competitors to deliver outperformance in the highly competitive world of investing – they need to both think and act in a differentiated manner. Behavioural biases and business pressures make truly independent thinking and positioning in portfolios extremely rare.

Read moreGlobal equities – Beware the rearview mirror - Angles & Perspectives

A globally integrated investment process – different by design. At PSG Asset Management, we have been investing in global equities since 2006. Our global process serves the offshore component of our local funds and our stand-alone global funds. Constructing a portfolio of one’s best ideas can be a challenging task, even in the relatively small local market such as the JSE, and even more so globally.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.