Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

18

February 2026

Boom or bust in 2026? That is the wrong macro question! - Angles & Perspectives Q4 2025

Kevin Cousins, Head of Research

PSG Asset Management

Boom or bust in 2026? That is the wrong macro question!

Traditionally, bottom-up investment houses do not pay a lot of attention to ‘macro’ views (the top-down view of macroeconomics and markets). The period following the Global Financial Crisis (GFC) was one of secular stagnation, with macro variables behaving in relatively stable and predictable ways. However, we have seen macro volatility return with a vengeance over the past four years. Since early 2021, we have allocated more research time to facilitate our process becoming more ‘macro aware’. Rather than attempting macro forecasts, we focus on a number of scenarios. Our goal is to assist fund managers to be aware of and comfortable with risks and fund positioning, and to ensure that our portfolios are capable of navigating a wide variety of possible macro outcomes.

The macro environment changed radically after the Covid crisis

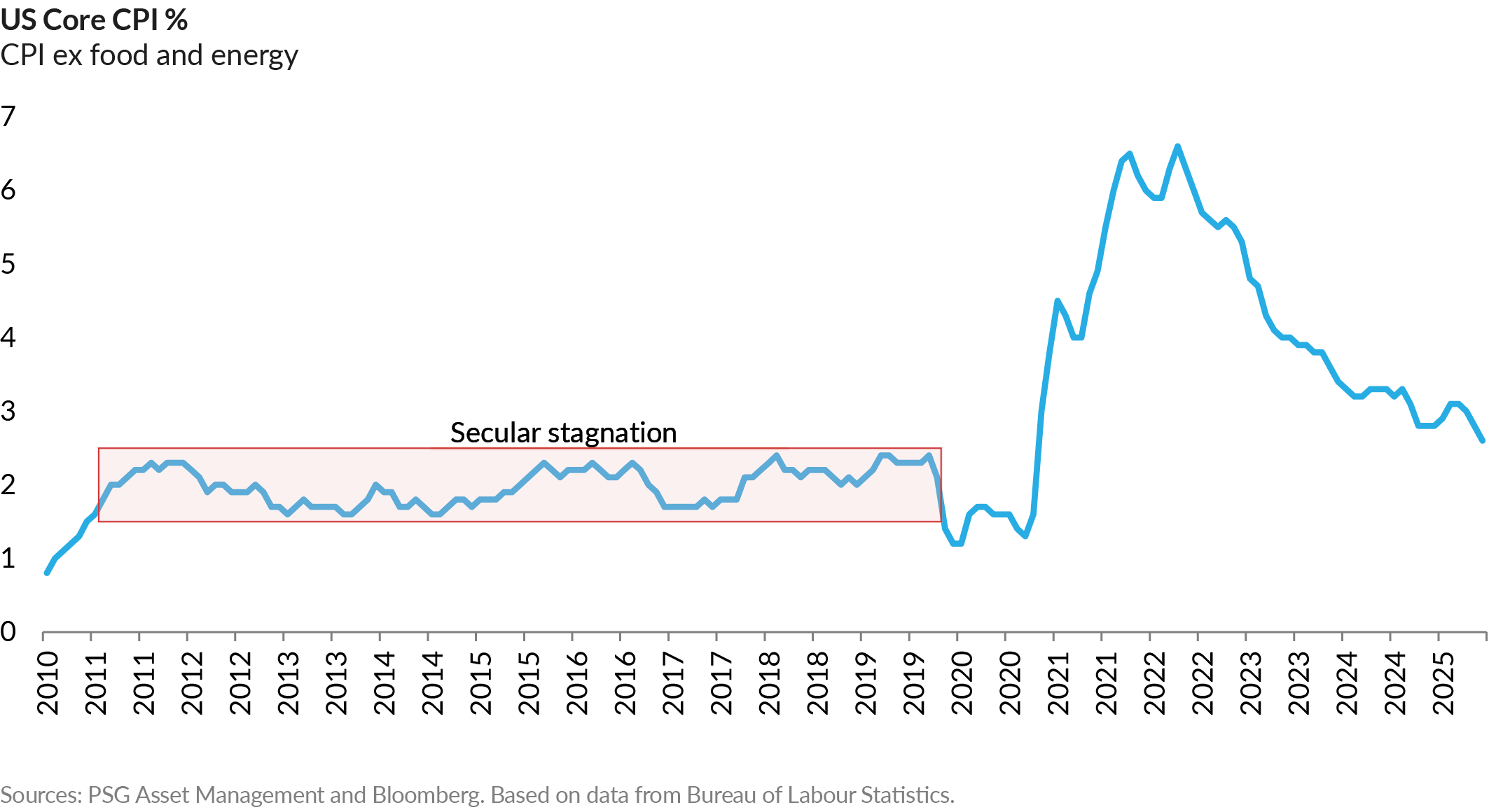

The decade after the GFC was well described as a period of secular stagnation with little macroeconomic volatility. For example, the US core CPI (shown below) remained in a narrow 90 basis point range of 1.5% to 2.4% from late 2011 to early 2020. Since early 2021, it became clear to us that the build-up of substantial financial imbalances, combined with global policymaker responses to Covid-19, raised the probability that the world – and the US in particular – had entered a new economic era. This view has proved to be accurate, with macro volatility returning with a vengeance over the last four years.

We have therefore been devoting a larger slice of research efforts to the macro environment since 2021, incorporating more macro insights into our investment process via our Portfolio Review Group (PRG). Our portfolios are unashamedly constructed on a bottom-up basis, but the PRG process is designed to facilitate ‘what if’ questions through (inter alia) stress tests, scenario analyses and factor analyses. This helps to ensure fund managers are fully aware of and comfortable with risks and fund positioning (both on an absolute and a relative basis) in the portfolios that they manage.

Higher macro volatility has been exacerbated by the increase in geopolitical risk and policy uncertainty as the world moves towards a multi-polar power structure. Since President Donald Trump’s inauguration a year ago, the US administration’s policies (not to mention President Trump’s social media postings!) have further amplified volatility.

Macro research, the PSG Asset Management way

A typical ‘top-down’ input into an investment process would be deriving a macro forecast and then optimising portfolio positioning to that forecast. The many 2026 outlooks and macro forecasts cluttering up our readers’ inboxes would be a prime example of this. While some articles review how their 2025 and prior predictions panned out, most don’t. This is for good reason: macro forecasting is hard in any environment, let alone the world we are in now. This is especially true over shorter time frames like one year, where even the most gifted and experienced analysts can be completely wrong.

You can’t ignore macro in today’s world, but forecasting is hard and you’re likely to get it wrong. So how do we practically navigate high macro volatility in our investment process?

Extreme uncertainty can be liberating

Acknowledging the extreme macro uncertainty and our inability to satisfactorily forecast the future allows the focus to shift to a much more productive approach to incorporating macro insights into our investment process. Specifically, we evaluate a number of different macro scenarios, and understand how assets behaved during similar macro periods historically. We can then evaluate the impact of similar macro scenarios on our portfolios.

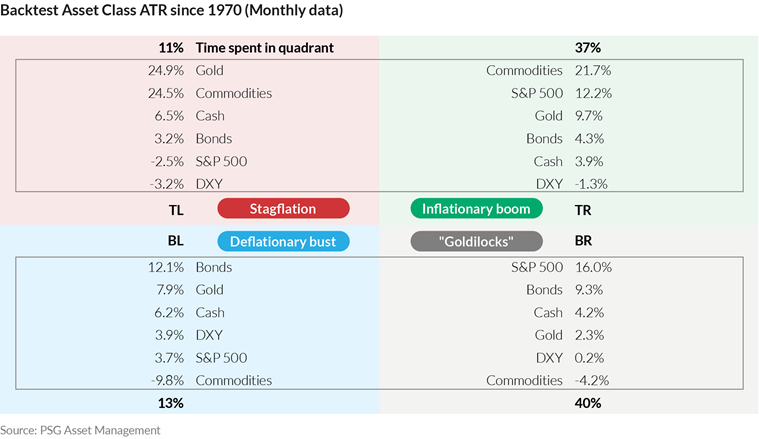

We use a macro grid dashboard loosely based on the ‘Investment Clock’ work by Trevor Greetham and Michael Harnett in 2004, at what was then Merrill Lynch. We classify the prevailing macro environment into four quadrants based on growth (above or below trend) and inflation (accelerating or decelerating). We have over 50 years of historic data about how different asset classes and sectors perform in each quadrant.

While we do attempt to apply a probability to which quadrants the US economy will be in, the important part of the work is drawing on the back-testing to understand how each of the different quadrant scenarios could impact our portfolios. For this we do not just look at the averages (shown above) but also the outliers, including how asset prices behaved during extreme events such as the GFC in 2008/9 and the Covid-19 crisis in March 2020.

To quote Australia’s The Future Fund: “The use of scenarios is not about predicting; it is about preparing. And proper preparation achieves portfolio resilience.”

The big caveats to this process

Relying on historic average correlations to construct well-diversified portfolios is standard practice in the asset management industry, and a key component of the quantitative risk models that are used almost universally to optimise portfolios.

The foundational assumption here is that historic average correlations between assets correctly describe future correlations. Like some other important assumptions in financial theory, this is unfortunately not the case in practice. Correlations tend to rise sharply during periods of market turmoil. This wreaks havoc in multi-asset portfolios that have been optimised based on historic average correlations.

In addition, the whole industry uses similar quantitative risk models drawing on similar historical data, and they are all searching for ‘idiosyncratic’ positions that will enhance portfolio resilience. Markets are dynamic, and future returns are hugely influenced by position crowding and starting valuations. This means an asset that acted as a good hedge historically may no longer behave in an uncorrelated fashion during the next big market event if it is widely owned and expensively valued.

Will your ‘idiosyncratic safe haven’ correlate with equities on the next big decline?

Many investment strategies today carry significant leverage, such as risk parity and ‘pod shop’ hedge funds. Leverage in the hedge fund industry is near all-time highs. This, together with client redemptions, increases the need for market participants to de-gross and sell holdings during market declines. If they have significant exposure to your so-called ‘safe haven’, it’s going to correlate with the collapsing market rather than act as a hedge.

The typical response to the resulting performance lag is to say you were carrying too much risk, and to lower the holdings in risk assets and increase the holdings in cash and other ‘safe’ assets going forward. This ‘drive slower’ response is likely to be a poor solution, as it limits upside returns. This inevitably raises what we see as a crucially important and little-discussed risk: that of not achieving client performance objectives over the long term.

What is a better way to respond to an uncertain macro environment?

We do not believe that attempting macro forecasts, especially over short time frames, is time well spent. Such forecasts are very likely to be wrong, and even if they are correct, asset prices could behave in unexpected ways. We far prefer evaluating how our portfolios will perform across a variety of macro scenarios.

That said, here are four ways we believe genuine portfolio resilience can be maintained in uncertain times:

- Quantitative risk model output needs to be overlayed with a healthy dose of common sense. Simply understanding that what will be a safe-haven asset in the future cannot be quantitatively determined based on historic data, is an important differentiator. Creative and contrary thinking when determining research focus areas is essential. Attractive starting valuations and uncrowded positions are an obvious starting point.

- We spend most of our macro research efforts on understanding financial history, secular regimes and regime change (e.g. the reversal of bond/equity correlations in 2022). Secular forces act as ‘magnets’ pulling the economy towards a particular macro quadrant. These have proven to be a fertile area for research, requiring more of a focus on very long time frames – i.e. economic history, rather than quantitative modelling. We spend little time trying to forecast what will happen over the next year.

- Understanding the risk implications of very concentrated equity indices is essential as well, as indices like the S&P 500 and MSCI World currently carry large idiosyncratic sector risks rather than being a broad representation of the asset class (see our article The hidden risks of hugging an index).

Importantly, we use explicit hedging of equities to enable us to carry substantial and larger risk positions despite the uncertain environment (“drive fast, but invest in excellent brakes”). This explicit hedging makes our portfolios much less dependent on asset correlations in times of market stress.

Our macro research, while a relatively small part of our overall research efforts, plays an important role. It assists us in optimising portfolios that will be resilient through different macro environments but are still structured to achieve our clients’ long-term return objectives.

Recommended news

Welcome to the latest edition of the Angles & Perspectives - Q4 2025

In this edition, we discuss how our process leads us to construct portfolios that are able to do well in a variety of market conditions. Head of Research Kevin Cousins discusses the shortcomings of forecasts, and our preference when navigating an uncertain macro environment. Chief Investment Officer John Gilchrist shares how our stock selection positions our portfolios to excel in a variety of scenarios, while Fund Manager Marc Beckenstrater asks whether large, global managers are really best positioned to deliver performance to investors. Finally, Fund Manager Duayne le Roux highlights that despite a softening interest rate environment, inflation-linked bonds can make an attractive addition to fixed income portfolios.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.