Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

15

September 2023

What’s the Obvious Story in 2033?

Philipp Wörz, Fund Manager

PSG Asset Management

Imagine for a moment you are an investor in early 2008 questioning the value of the US dollar as a store of value, having seen the dollar index decline 40% from 2001 to an all-time low in March 2008.

What’s the obvious story in 2033?

Imagine for a moment you are an investor in early 2008 questioning the value of the US dollar as a store of value, having seen the dollar index decline 40% from 2001 to an all-time low in March 2008.

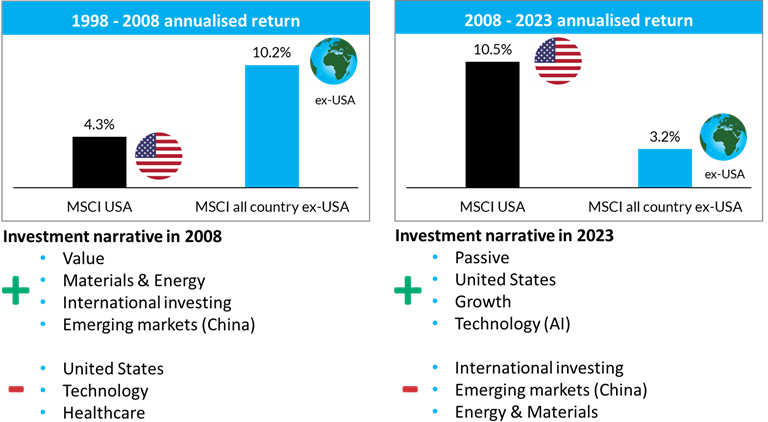

Over the decade ending March 2008, returns from US stocks (as measured by the MSCI USA Index) had been lacklustre, delivering a total return of 4.3% per annum. International stocks, as measured by the MSCI All Country World ex-USA index (MSCI ACWI ex-USA), on the other hand, handsomely outperformed the US market by 6% per annum for an annualised return of 10.2%.

The rise of China and other emerging markets, and wildly speculative property markets contributed to the materials, energy and real estate sectors dominating the decade’s return tables to 2008, while communication services, information technology (still recovering from the bursting of the dotcom bubble) and healthcare were at the back of the pack.

Unsurprisingly, the popular narrative of how to invest at the time was to shun the US and technology stocks and buy anything related to China and materials stocks, in particular.

Fast forward to today and the tables have turned. The US market has been the gift that kept giving since the Global Financial Crisis (GFC), while China has gone from darling to ugly duckling. A swift recovery from the GFC, excessively loose monetary policies favouring growth assets, troubles abroad (European credit, Brexit, lost decade for emerging markets, etc.) and more recently the continued dominance of ‘big tech’, meant that the American market and the US dollar were the places to be. Isn’t it all so obvious, in hindsight?!

Since March 2008, the US stock market has outperformed international markets by over 7% per annum with information technology and healthcare the top performers, while previous high-fliers, materials and energy, languished – nearly the mirror opposite of the experience from 1998 to 2008.

Sources: Bloomberg and PSG Asset Management, total annualised returns 30 September 1998 – 31 March 2008, 31 March 2008 – 31 August 2023

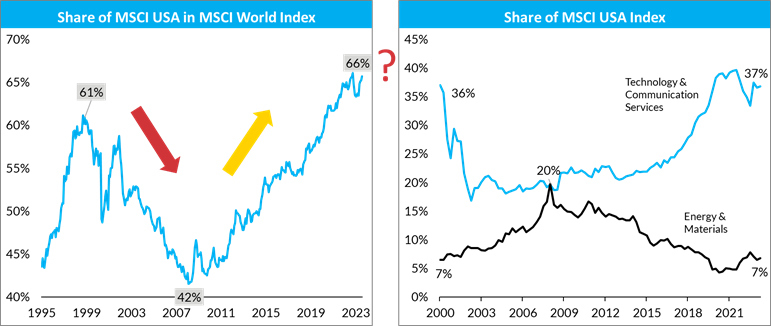

Given this backdrop and investors’ tendencies to extrapolate long term trends, it is not surprising that the winners of the past (US-focused indices and areas benefitting from the latest technology trends, such as artificial intelligence (AI)), dominate investors’ portfolios and passive indices today. Why would anyone want to invest in areas other than the US and tech, given the resilience of the world’s largest economy and continued dominance of the world’s largest tech platforms?

The positioning of passive indices bears this out, as seen in the graphs below: the share of the United States in the MSCI World Index is back to historically high levels. Interestingly, within the MSCI USA index, information technology and communications services account for 37% of the index while energy and materials are less than 7%.

Index composition

Sources: Bloomberg and PSG Asset Management. MSCI USA market cap as % of MSCI World market cap; MSCI USA sectors as % of MSCI USA market cap, data to 31 August 2023.

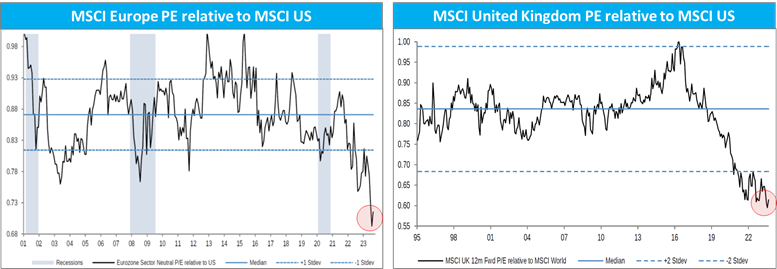

We have written extensively about the market inflection brought about by the Covid-19 pandemic and the beginning of the process to unwind the significant market distortions built up over previous decades. The end of the disinflationary environment and a four-decade bull market in bonds, coupled with significant under-investment in the real economy over the past decade, an energy transition and the need to build supply chain redundancy given the volatile and uncertain geopolitical environment, suggest the future is likely to look very different to the post-GFC period.

Interestingly, some of the likely net beneficiaries of a changing environment - stocks outside the US - are trading at the largest valuation discount seen in decades, as shown below.

Sources: Datastream, IBES and JPMorgan

It is impossible to consistently predict the future and successful long-term investing is not about knowing exactly what will happen next. Rather, it is about assessing where the odds of success are stacked in your favour and allocating capital accordingly, while keeping an open mind. When looking back in a decade’s time, is it likely that your portfolio would have benefited from the great next ‘obvious story’?

An investment manager like PSG Asset Management, which seeks underappreciated quality trading at depressed valuations on a global basis, is well placed to uncover hidden gems that help tilt the odds of long-term success in the investor’s favour. Those already familiar with our thinking would not be surprised that we are currently finding opportunities in international equities outside the US and in real asset sectors, such as energy and materials.

For more insights into our current thinking, read our latest Angles & Perspectives.

Philipp Wörz is a Fund Manager at PSG Asset Management.

Recommended news

Angles & Perspectives - Second Quarter 2023

In this edition, Head of Research Kevin Cousins considers how a misunderstanding of the nature of inflation during the 1970s and 1980s may be contributing to an incorrect policy response currently. Assistant Fund Manager Ané Craig elaborates on how investors should think about navigating the investment environment when it is clear that conditions are far from ideal. Lastly, Fund Manager Shaun le Roux argues that in the current environment, the benefits for patient investors who can stay the course are amplified even more than usual.

Read more

The Free Lunch from Guarantees May Come at a Hefty Cost

The cyclicality of markets and investing is often recognised at the macro level: bull and bear markets, commodity super cycles, the outperformance of value or growth stocks at various times, to name just a few. However, I’d like to argue that with the cyclical nature of the stock market, comes a certain cyclicality in investor behaviour and sentiment too: we often find that similar topics crop up predictably from time to time, as market movements and cycles play out.

Read more

Investing when the market blows hot and cold

It is amazing how many major events the year has already delivered – and we are only halfway through. We have seen a banking crisis causing fall-out on both sides of the Atlantic, a debt ceiling stand-off in the US, the rand at (repeated) record lows against the US dollar and unprecedented levels of loadshedding locally, not to mention the diplomatic fallout from the Lady R debacle. Investors would be forgiven for feeling slightly exhausted so early in the year.

Read more

Globally integrated, team-based approach credited for Raging Bull success

PSG Asset Management delivered a strong showing at the most recent Raging Bull Awards. The prestigious awards recognised funds that delivered category-leading performance for various periods ended 31 December 2022.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.