Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

02

December 2025

Should investors be adding to their offshore component?

Craig Sterling CFP®

PSG Wealth

Sometimes it is nice to live at the pointy end of Africa

Feel free to reach out to PSG Wealth Manager Craig Sterling directly.

At the time of writing our local bourse is up a pleasing 28.7% over 12 months. Sure, we have been affected by international events, I think back to Covid in 2020, the Chinese Evergrande collapse in 2021, and the February 2022 Russia and Ukraine war. Also, the third biggest bank crisis in US history hit in March 2023 when Silicon Valley Bank (SVB) collapsed. In addition, conflict in some African countries continue.

Despite its shortcomings, South Africa has managed to emerge on relatively solid footing. The transition of the ANC led government to the GNU has been remarkably calm. We are inundated with new corruption cases being brought to court on daily basis. Much was made of South Africa’s grey listing, but little has been reported on the strengthened controls, increased enforcement and the 22 action items we ‘ticked off’ to regain our investment status.

A look into past performance:

The takeaway from the above table is twofold: global equity has handsomely outperformed over the past 10 and 15 years. Secondly, local equities have started to show signs of life over a 5-year period and year-to-date (YTD).

Reasons to invest offshore:

- South Africa still only makes up 0.6% of global GDP.

- There are around 266 companies listed on the JSE; the local universe is limited when compared to our global peers.

- Possibly the most compelling reason to invest a portion of your wealth offshore is the level of South Africa’s economic growth along with our ever-changing political landscape.

- Our volatile local currency tends to behave like a Disney rollercoaster, in mid-2025 we reached our worst ever exchange rate of R19.93/$1. Given such volatility, one should build an offshore portfolio to smooth out returns.

How much offshore is ideal?

Let me start by saying there is no “one size fit all” allocation, but there are guidelines and research on the subject.

Two decades ago, when I started my career at PSG, there was a pension fund regulation limiting offshore exposure in pension funds to a maximum of 15%. The limit has gradually been increased and now stands on an aggregate 45% for all foreign assets. It is fair to say that fund managers have more arrows in their quiver as their investment universe has expanded since 2004.

The following broad statements can be considered for further guidance:

- Liquid (accessible) investments are likely to have less offshore exposure.

- More conservative investments are likely to have less offshore exposure.

- Investors who require a monthly income are more likely to have less offshore exposure.

- An investor with ample capital is able to take more risk than an investor who struggles to make ends meet.

- Lastly, younger generations are generally able to invest a higher percentage of their wealth offshore.

Notwithstanding the above, your financial adviser will need to look at your personal scenario, understand your short- and long-term goals and finally steer you on a path which will above all else, satisfy your goals. Over the past two decades we have seen a rise in offshore investing, and we expect the trend to continue.

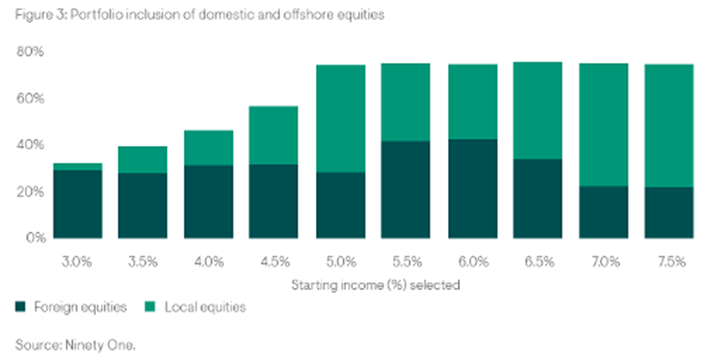

Below is an interesting case study done by Jaco van Tonder of Ninety One Platform, he looked at the ideal offshore exposure within a living annuity and the results are surprising.

He makes three conclusions required to deliver a 30-year inflation proof income:

- A living annuity portfolio should consist of 25-40% in equities for low starting incomes in the range of 2.5-3.5%.

- As initial income levels increase from these low levels, annuities require increased exposure to equities. As your starting income requirement reaches 4%, the minimum equity exposure is already at 50%. At a 5% starting income, your equity exposure should be over 70%.

- A living annuity requires a consistent 20-35% exposure to offshore equities, irrespective of the size of the initial income drawdown levels.

The following chart highlights the split between South African equities and offshore equities within the optimised annuity:

The above graph does appear strange, as a high percentage of offshore exposure is allocated to lower withdrawal rates.

Jaco summarises the above graph as follows:

“The answer to these questions lies in the unique diversification benefits of offshore equities when combined with a South African portfolio of bonds and equities:

- Offshore equities have the advantage of a lower correlation with South African bonds.

- But domestic equities have a higher real return than offshore equities.

What we see in Figure 3 is the interplay between real return and portfolio volatility. Annuities are sensitive to portfolio volatility. Therefore, our optimiser model adds offshore equities at lower incomes because they simultaneously:

- Increase the real return potential of the portfolio, and

- Improve the risk profile of the overall investment portfolio.

However, as incomes increase, the stronger real return from domestic equities becomes more important than the lower volatility of the offshore equities, and the model starts allocating more and more to domestic equities.

The model proposes an offshore equity exposure in the region of 20-40% of the total portfolio across all starting incomes. Even for low starting incomes of 3%, the model suggests an offshore equity holding of around 25% of the total portfolio.”

Although stats don’t lie, they may not tell the full story. Your total offshore exposure must be aligned to your goals. An adviser will always look at your needs and goals to determine your ideal offshore exposure. This article has alluded to the volatility in the rand, and one should be acutely aware that volatility does not only mean a weakening in the rand, but also a strengthening, as we have witnessed over the past year.

South Africans cannot, nor should we, discount the macroeconomic environment we operate in. Statistical data (indicating 25% offshore exposure) does not accurately guide the ideal future offshore exposure, but one could argue that constructing a well-diversified South African portfolio will likely push your offshore exposure to around the 40% level in today’s environment. Yes, it is a moving target, and yes, Peter will look different to Paul, but comfort is important when investing – make sure you understand the value of your offshore investment.

Stay Informed

Sign up for our newsletters and receive information on finance.