Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

09

September 2024

ETFs: Trends this year

Schalk Louw, Wealth Manager

Wealth

With two-thirds of 2024 behind us and Boney M Christmas carols scheduled to start playing in the shopping malls in the not-too-distant future, now might be a good time to review your portfolios and start planning for 2025. I thought it would be a good idea to focus on several trends this month to identify potential opportunities and risks. I do this using everyday data that is freely available to investors worldwide. When we look at 2024 so far (as at 26 August 2024), I’ve noticed that it’s very much a continuation of 2023 - US growth, driven by tech has continued to dominate in 2024.

Feel free to reach out to PSG Wealth Manager Schalk Louw directly.

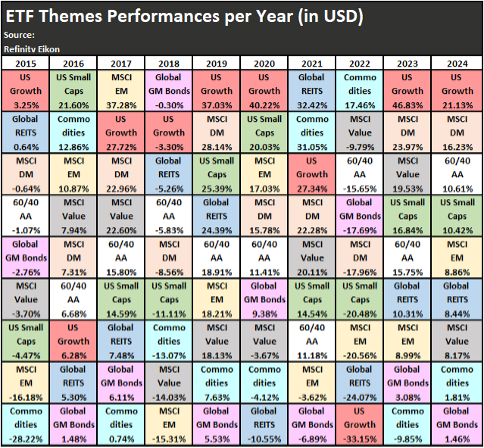

2024 trends largely follow the 2023 playbook

Source: Refinitiv Eikon

Developed markets are outperforming emerging markets, global bonds and commodities are struggling, and small caps are holding their own. However, there are two significant differences: value stocks are struggling significantly this year, and balanced portfolios have made a comeback. We will delve deeper into several of these trends a bit later.

The ever-magnificent sectors

Source: Refinitiv Eikon

For those who were underweight in communication or tech, unfortunately, they were also underweight in returns. Financial stocks didn't perform too badly either. However, resource stocks struggled, with consumer discretionary stocks not faring much better.

Value opportunities or value traps?

Source: Refinitiv Eikon

As many well-known fund managers and large investment firms have pointed out, value stocks have become progressively cheaper over the past decade, and 2024 was no exception. If this area of the global markets stood out as an opportunity for investors at the end of 2023, it could be even more enticing now, with the relative performance clearly highlighting the underperformance of value stocks. Only time will tell if this turns out to be a value trap.

Small could be a big opportunity

Source: Refinitiv Eikon

Larger companies with bigger wallets are able to withstand a higher interest rate cycle more comfortably. This becomes especially clear when comparing US small-cap stocks with their larger counterparts, such as those in the S&P 500. Since the Fed raised rates 11 times since March 2022, US small caps have lagged behind significantly. Between the "magnificent" tech rally and the heavier strain on smaller companies in this high-interest-rate cycle, this gap widened further in 2024. The big question now remains: if they struggled in a high-interest-rate environment, how will they perform during a period of falling interest rates, which is now strongly anticipated in September 2024?

How not to train your dragon

Source: Refinitiv Eikon

According to reports from most of the top investment houses, they believed that this would be the "year of the dragon" and that China, against all odds, might not only start its recovery but also give most other countries a run for their money. However, this has not been the case at all, with China underperforming not only in developed markets but even in emerging markets.

Noteworthy is that South Africa has not only comfortably outperformed the Emerging Markets Index in 2024, but it’s also one of the best investment destinations so far this year.

“Be fearful when others are greedy and greedy when others are fearful” – Warren Buffett

Source: Refinitiv Eikon

On to tech-related stocks. During the massive drop in world markets in 2022, when the Nasdaq was at one point down over 30% from its highs, the phrase most often heard from investors with overweight positions in these sectors was, "I will never be greedy again." However, this sector has recovered from the losses of 2022 but has been reaching new highs for months.

In future commentary, I will look at other trends such as high-dividend stocks that look attractive, gold miners that still lag the gold price and the MSCI All Country World Index, excluding the US, which hasn't been a very attractive investment.

Stay Informed

Sign up for our newsletters and receive information on finance.