Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

30

October 2024

The burden on Trustees in South Africa: Relevance, Loans and Distributions

Craig Sterling CFP®

PSG Wealth

The taxation of trusts is a hot topic and every so often laws change, and trustees are left with the burden of applying the correct taxation to the trusts. Income and gains in respect of trust assets can be taxed in a trust’s own right or the conduit principle can be applied where the beneficiaries of the trust are taxed if the income or capital is distributed to the beneficiaries in the same tax year.

Feel free to reach out to PSG Wealth Manager Craig Sterling directly.

A typical South African Trust

It is no secret that it has become more complicated to move assets into a trust since Section 7C of the Income Tax Act came into effect on 1st of March 2017. It was common practice for a trust to receive assets from the Founder of the Trust via an interest-free loan. Well, Section 7C forces individuals to charge the Trustees, interest on any loans to the Trust at the prescribed rate. If they don’t, it will have a donations tax implication for the founder. It is fair to say that the popularity of trusts has reduced since the introduction of this anti-avoidance provision.

Is a Trust still useful?

In short, yes, a trust can be a useful vehicle for estate planning. Trusts have many benefits and can be used effectively within the South African context. We take a look at a few of the benefits of a Trust where all founders and beneficiaries are South African residents.

1. A Trust doesn’t die

Any asset or sum of money within a trust (assuming no loans) will have no estate duty implications for the founder or beneficiaries. No estate duty is a huge benefit of growing wealth in a trust. Remember that when an individual passes away, there is a deemed capital gains tax event of as much as 18%. If the assets are in a trust no such deemed disposal takes place.

2. Effective control

The trustees of a trust take stewardship of the trust assets and thereby control all decisions pertaining to the assets for the benefit of all beneficiaries.

The founder of a trust can rest assured that wealth can be transferred to the next generation without the reckless spending that can accompany transfer of wealth to children.

A trust can also meaningfully assist individuals who have mental health diseases such as Alzheimer’s disease, because the trustees can manage and protect the assets of the individual who does not have the mental capacity to manage their own affairs.

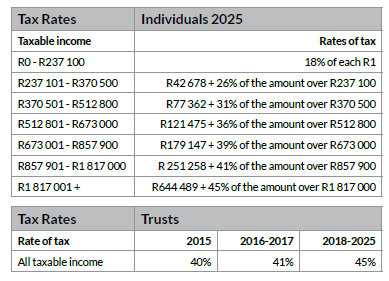

3. Tax and the Conduit Principle

Trust’s carry the highest income tax and capital gain tax of all taxpaying entities. Income is taxed at a flat rate of 45% and capital gains are taxed at a flat rate of 36% - ouch! We have seen an increase in these rates over time:

Distributions:

When Trustees distribute income and/or capital to beneficiaries, they effectively shift the tax burden generated in a trust to the beneficiaries, and benefit from potentially lower tax rates. We refer to this as the conduit principle.

In the below example a trust’s rental unit earns R200,000 in rental income and the rental unit had a capital growth of R200,000. The rental asset is currently worth R4.4 million.

It is therefore fair to assume that the total growth has been R400,000. We are not selling the unit so there is no Capital Gains Tax (CGT) applicable. However, SARS does expect tax to be paid on the income earned.

Example 1: Taxed within the Trust

R200,000 x 45% = R90,000 must be paid to SARS.

The trust therefore makes a net profit of R110,000 and holds assets of R4.31 million.

Example 2: Distributed to a minor beneficiary

R200,000 x 18% = R36,000 – 17,235 rebate = R18,765 must be paid by the minor to SARS. The trust’s asset has reduced by R200,000 because of the distribution. The trust makes a net profit of only R4.2 million for the year

A Comment and a Solution:

Once the trust has distributed income or capital, or it has been vested in the name of the beneficiary, ownership lies with the beneficiary, which may have estate duty implications for the beneficiary. Trustees often decide to retain the distribution within the trust so that future growth takes place in the trust – but the trustees must document that the beneficiaries have a vested right to the distribution and can call on it at any time.

The taxation of trusts has no ‘one size fits all’. Making use of the conduit principle, allows for the most efficient taxation of a family unit but trustees must act independently and, in the trust’s best interest. It is also important to understand the implications of the distribution as part of the beneficiaries own financial plan and to keep in mind that SARS has stringent reporting requirements in respect of distributions to beneficiaries.

Stay Informed

Sign up for our newsletters and receive information on finance.