Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

18

November 2022

Who should I nominate as a beneficiary on my retirement investments?

Bernice Barnard

PSG Wealth Old Oak

Estate planning and nominating beneficiaries can be quite a daunting exercise, given its technical and legislative nature. To find the most cost-effective way to structure their beneficiary nominations, we are often asked by clients whether nominating an inter vivos trust as a beneficiary on a living annuity, retirement annuity or preservation fund is better than nominating an individual.

“ The onus rests on you to partner with your financial planner to find the best solution to suit your individual needs. ”

This consideration is relevant when it comes to estate planning or to ensure the most effective treatment of retirement benefits after death.

Where do you start?

Getting a clear picture of your specific needs and required outcomes in the event of death is essential. All your assets, liabilities and wishes should be taken into account. It is clear that there is no one-size-fits-all solution as every client’s situation and needs are different. Therefore, it is imperative that you understand the tax treatment of both options and that this is considered when structuring beneficiaries on these investments.

Top considerations when making this decision

For this exercise, we will not be unpacking the issue of primary and secondary beneficiaries in-depth or going into intense detail about the legal aspects of estate planning, as there are too many variables at play. We will however, point out key considerations if you are unsure whether to nominate an individual (or individuals) or an inter vivos trust as a beneficiary on these types of retirement investments. The onus rests on you to partner with your financial planner to find the best solution to suit your individual needs.

Living annuities (compulsory income) on which a beneficiary is nominated, retirement annuities, pension funds and preservation funds fall outside your estate, and a letter of executorship is not required to distribute the funds to your beneficiaries. No estate duty is payable on these investments.

If an individual is nominated as a beneficiary on any of these investments, they will have three options to choose from if the investor passes away:

1. Transfer the full benefit to a living annuity/life annuity to earn a compulsory monthly income.

In this event, the lump sum transfer will not result in any tax liability. However, the income the nominated beneficiary receives will be subject to tax according to their marginal income tax rate.

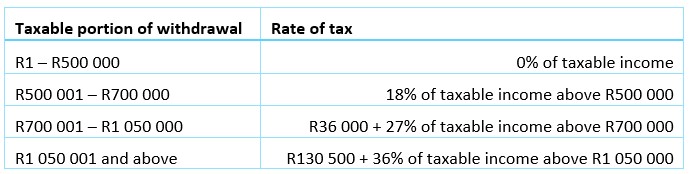

2. Take the full benefit as a cash lump sum.

When choosing this option, the full benefit will be subject to tax (for the deceased) based on the retirement tax table as follows:

It is important to note that by choosing this option, the table is applied cumulatively and considers all lump sums taken from pension/retirement funds over the deceased’s lifetime. This means that the final amount the nominated beneficiary receives will depend on whether the deceased had taken any retirement cash lump sums prior to their death.

3. A combination of a living annuity/life annuity (option 1) and a cash lump sum (option 2).

An important factor to keep in mind is that retirement annuities, pension funds, provident funds and preservation funds are subject to Section 37C of the Pension Funds Act, which means that following the investor’s death, the trustees of the fund will conduct an investigation with regards to the deceased’s dependants, and will distribute the funds according to their findings. Dependants will include children, spouses, individuals towards whom you had a maintenance obligation, other financial dependants, or individuals that may become financially dependent on you in the future, such as unborn children conceived prior to your death and the mother of the unborn child. The trustees will use the nomination form as guidance during their investigation. If they find no dependants, they must pay out the death benefit in accordance the nomination form.

That ultimately means that while they will consider your nominations, you do not have the final say in how your retirement benefit will be distributed after you pass away.

For this reason, it is crucial to ensure that your nominations and dependants are kept up to date on these products to help guide the trustees, which have a maximum of twelve months to finalise the distribution.

A living annuity is not governed by the Pension Funds Act and is consequently not subject to Section 37C. The benefit must be distributed in line with your beneficiary nominations. However, if no beneficiaries have been nominated, the benefit will be paid to your estate and may be subject to income tax according to the retirement scales, executor’s fees and potentially even estate duty (if the spouse does not inherit, in which case Section 4(q) of the Estate Duty Act will not apply).

An inter vivos trust can be nominated as a beneficiary on a Living Annuity, but there are some critical considerations when choosing that option:

- The full benefit, in most cases, will be paid out as a cash lump sum, which will attract tax according to the retirement lump sum tax tables (set out above).

- Not all providers allow for the trust to become the new annuity holder. Where it is permitted, the trustees assume the responsibility of distributing the annuity income to the beneficiaries, subject to the income tax rate applicable to trusts (i.e., 45%). Only some companies allow for a tax directive (which will specify the rate of tax to be deducted) to be requested from SARS by the trustees, which means that the beneficiary may be taxed at a lower rate, but this is an administratively intense procedure to maintain.

Nominating a trust as a primary beneficiary

Once again, your specific needs will dictate the best course of action, making it so important to have the backing of a trusted expert. While we usually do not recommend that the client nominates a trust as a beneficiary on a living annuity based on the abovementioned factors, every client has their own unique situation. Good reasons for nominating a trust as a primary beneficiary on your living annuity include that you may be a single parent with only minor beneficiaries, or you may have financial dependants with special needs. In such instances, you and your planner should weigh all the pros and cons, especially in terms of the tax treatment of the benefit, before you sign off. Kindly note that different tax rates apply to special trusts.

With the introduction of primary and alternative beneficiaries (living annuities), it allows you to assess who will need the money the most in the event of your death, and alternatively, to whom that benefit should be paid in case your primary beneficiary had predeceased you or passes away at the same time as you. It allows you to consider the needs of your respective beneficiaries - to whom a lump sum would be more practical, while others who do live in the country may prefer a monthly income. Certain providers also allow you to nominate your estate as an alternative beneficiary, which allows them to take guidance from the executor when the primary beneficiary is no longer alive.

Structuring your investments to reach the best possible outcome

All of these factors only scratch the surface of the options and concerns you have to ponder when it comes to estate planning in its entirety. Another consideration in the “who gets what” chapter is the impact of Section 4(q) of the Estate Duty Act, which states that the value of all property bequeathed to the surviving spouse can be deducted from estate duty. Capital gains tax in respect of property bequeathed to the surviving spouse will roll over to the surviving spouse and will only be considered for tax purposes once they dispose of the asset.

Undoubtedly, we all want to save as much as we can (especially when it comes to tax), but this illustrates the importance of consulting an expert and providing them with a complete list of assets and liabilities, as well as information about your personal circumstances and wishes when it comes to structuring your investments in line with your estate plan.

Stay Informed

Sign up for our newsletters and receive information on finance.