Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

15

July 2025

Impact of the weaker US Dollar on global company earnings

Franske Neiteler CFA®

PSG Pretoria East, Wealth Manager: Securities

As we enter the second half of 2025, one of the most defining macroeconomic shifts for the year to date has been the sharp decline of the US dollar. Currency trends might not dominate headlines like artificial intelligence (AI) or interest rates, but their impact on corporate earnings – especially those of large-cap multinational companies – is profound.

Feel free to reach out to PSG Wealth Manager Franske Neiteler directly.

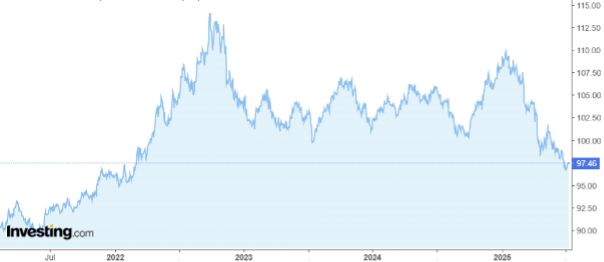

The numbers speak volumes. The US Dollar Index (DXY) fell 10.8% in the first half of 2025, marking its worst first-half performance since the end of the gold-backed Bretton Woods system in 1973. It has also been the weakest six-month stretch for the dollar since the Global Financial Crisis in 2009.

This sharp depreciation has been driven by a mix of investor concerns: a growing US deficit, a rise in protectionist tariffs, and mounting pressure on the US Federal Reserve to cut rates, to name a few.

Figure1: DXY Index 5-year price history

Source: Investing.com

This is not all bad news, since a weaker dollar is generally a net positive for US companies with multinational earnings. Taking the Magnificent 7 (Apple, Microsoft, Amazon, Alphabet, Meta, Tesla, Nvidia) as an example, they earn large parts, if not the majority, of their revenue outside the borders of the US. As the USD declines, foreign income translates into more dollars, lifting top-line results and reported profits.

Figure 2: International revenue exposure of large-cap US companies

While some of these firms may face increased costs in local currencies (particularly if they manufacture abroad), the revenue translation effect typically outweighs the expense impact, especially in high-margin sectors like software, advertising, and cloud services.

However, this does not hold true for the majority of the SP 500 firms, as shown in Figure 3 below.

Figure 3: US and European stock market geographic revenue exposure

Source: Bloomberg

For European multinationals, the story is less favourable. Companies in the Stoxx 600 Index – which derives more than half of its revenue from international markets, particularly the US – are now facing significant FX headwinds. As the euro and pound strengthen against the US dollar, USD earnings convert into fewer euros or pounds, weighing directly on reported revenues. Goldman Sachs created an index of European stocks with significant USD currency exposure and, as shown below, these stocks show a strong pricing relationship with the weaker USD or, alternatively, a stronger EUR.

Figure 4: Goldman Sachs EU dollar-exposed stocks relative to Stoxx 600 vs Dollar Index

Sources: Bloomberg, Goldman Sachs

While the greenback remains dominant in global trade and transactional volume, its share in foreign exchange reserves has been declining steadily over the past decade. Central banks – especially in China, India, Russia, and Saudi Arabia – continue to diversify into other asset classes and currencies as their terms of trade evolve and other emerging markets start to form part of the global trade landscape.

Despite these trends, foreign demand for US Treasuries remains strong, with Japan and the UK leading the way. This supports the longer-term confidence in US capital markets, even as the dollar takes a breather.

While currency volatility has undoubtedly shaped the macroeconomic narrative of the first half of 2025, global equity markets have shown a remarkable ability to absorb and even thrive amid shifting conditions. From a plunging US dollar to evolving global trade dynamics, investors have navigated a complex landscape with resilience. Remarkably, despite these headwinds, major global indices have powered to fresh all-time highs, underscoring the market’s forward-looking nature and faith in earnings strength, policy support, and structural growth trends. As we move into the second half of the year, markets continue to grind higher, reminding investors that volatility and opportunity often go hand in hand, and in any crisis a new opportunity set, or outperformance, arises.

Stay Informed

Sign up for our newsletters and receive information on finance.