Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

11

March 2022

Ukraine War, Energy Market Paralysis & Stock Market Positioning

Tunin Roy

Wealth Adviser

“Monetary authorities will need to carefully monitor the pass-through of rising international prices to domestic inflation, to calibrate appropriate responses. Fiscal policy will need to support the most vulnerable households, to help offset rising living costs. This crisis will create complex policy tradeoffs, further complicating the policy landscape as the world economy recovers from the pandemic crisis.”

“ The conflict in Ukraine has threatened energy supply to Europe in particular but also to the world. ”

After a tumultuous and very disturbing week gone by, many of you, particularly those with substantial offshore portfolios, may be feeling some concern about the value of their holdings and the current direction of the markets. That is not to say, of course, that we are not primarily moved by the human tragedy of what is unfolding in Ukraine and the immense levels of suffering that the conflict has unleashed. My first thoughts are certainly to hope desperately for a swift end to the conflict and an end to the brutal scenes seen on our televisions and news channels over the last week.

However, I am also conscious that, as a financial and investment adviser, I have a strong responsibility to navigate the way through such crises to minimise potential negative impacts to my clients and their funds that have been entrusted to me. During the last week, the PSG investment team and I have spent much time analysing the current situation in global markets, discussing it with colleagues and fellow professionals and trying to gauge the right course of action in terms of advice for our clients. I have received an enormous amount of analysis from across the globe from investment banks and asset managers as well as reading the financial press and have been studying all of it to try and make sense of the situation. I therefore thought it useful to share some of this with you and to try and allay some of your fears at this time.

To summarise what is happening currently, we are seeing pretty indiscriminate selling of all global assets across the board – equities, both growth and value, across most sectors, investment grade bonds, credit, property, cryptocurrencies and particularly Europe and emerging markets have suffered as fears of stagflation and $200 oil have gripped markets. The only hiding place has been cash or bonds; and the only thing going up has been commodities, particularly oil and gold, which in a rare turn of events has meant that our local South African equity market has been performing relatively well.

Unsurprisingly, defence stocks and armaments manufacturers have performed well, particularly in Europe. More generally, fear abounds and we are seeing continued sell-offs this morning as fighting in Ukraine intensifies, oil pushes towards $140 with fears of a US-backed embargo and Russia throws a spanner in the works of a new Iran nuclear deal.

The conflict in Ukraine has threatened energy supply to Europe in particular but also to the world. Although Russia is less than 2% of global GDP, its oil accounts for approximately 7% of the global market, its gas supplies over 50% of many European countries’ needs. However, Breugel, the European energy consultants, believe that European energy stocks are just enough to cover the remaining months of their winter. Both Ukraine and Russia are major wheat exporters accounting for more than 25% of world exports and we have seen corresponding rising prices in agricultural markets. The Russian capital markets are effectively closed and more and more international companies are pulling out of Russia, causing potential instability and hopefully fomenting some pressure for change on the domestic front as sanctions start to bite.

Although speculation was rife for about a week prior, Russia’s invasion took the world by surprise and was wholly unexpected by most market participants. We could not have prepared for such an idiosyncratic risk and, like the outbreak of COVID-19, it shocked markets and has caused a very swift and severe response in prices. To quote the economist and financial author Jared Dillian, “Such is the nature of forecasting. You have a logical, well-thought out thesis and then some exogenous event happens that screws everything up – like Russia invading Ukraine and upending global markets.”

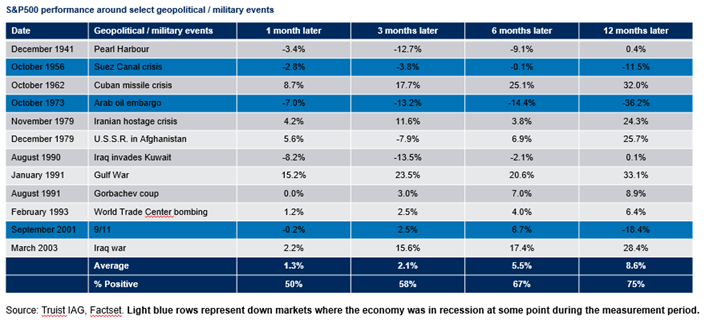

However, now is not the time to panic. There have been multiple geopolitical crises in the past and if you sold in the fear of the immediate aftermath, you almost always would have lost out. The below table shows the performance of the US equity benchmark index, the S&P500, over various short-term periods subsequent to a crisis.

The footnote is worth considering – so, basically, in all cases except those where the US economy was in recession, returns were positive, sometimes substantially, 12 months after the event. The concern now is that the current situation might resemble the period subsequent to the 1973 Yom Kipur War. A period of stagnation is possible and we will be watching data releases to assess every possibility of that playing out. However, although growth is certainly seen to be slowing, the IMF has revised down its forecast for global growth to 4.4% from 4.9% for 2022, which is still a very strong number and suggests that stagnation fears are perhaps overplayed.

A period of elevated inflation seems certain now and the hopes of a year ago that inflation would prove transitory have been dashed. However, it is likely that inflationary pressures should start to ease towards the end of this year and markets should start to price any downwards movement in immediately as they appear. With potential economic weakness also comes less pressure on central banks to raise rates or reduce the size of their balance sheets in response to exogenous inflationary shocks in energy and food markets. This could be good news for markets and may well allow for a reassessment on the valuations for tech stocks, which have been hit particularly hard recently as rising rates have caused higher discount rates to be applied to their long-term cashflows giving rise for pressure on their valuations.

We all know that markets do not deliver returns in a straight line and that short-term volatility comes with the territory. We do not know how this conflict will play out or how long it will last. However, what we do know is

long-term investment returns. Too often I have seen panicked investors wanting to sell or move to more defensive allocation to limit losses at precisely the wrong time and miss out on what can be rapid and significant reversals of downward trends. Covid was just the most recent example of an unexpected negative shock that initially smashed economies and riskier assets. But growth returned strongly and asset prices rallied dramatically. The worry now is that the snapback in growth after the onset of COVID was largely due to central bank levers being pulled which, due to the re-emergence of inflation, can no longer be pulled. The outlook for inflation, the length of the war and the peak for the oil price will be key to determining what happens next.

We expect continued volatility in the short term as world leaders introduce a barrage of additional penalties and sanctions and money managers assess the effects of the intensifying conflict - from sanctions to shortages and price surges. From a monetary policy perspective, this conflict warrants a further evaluation of the already complex growth-inflation tradeoff. Central banks are walking a tightrope between slowing economic momentum and high inflation and are likely to proceed prudently given the elevated growth risks encountered. Myself and the team at PSG Wealth are closely monitoring the potential outcomes, ongoing data releases and the impacts on companies within our funds and as the situation changes and we will be sure to propose adjustments to positioning should they be necessary. For now, however, the best thing is to sit tight and wait although it may be tough.

Stay Informed

Sign up for our newsletters and receive information on finance.