Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

07

December 2021

A good year for equities

Wilhelm Visser

Partner and Wealth Manager: Securities

The year to date has turned out pretty good thus far, for most equity markets, both global and local, despite lots of uncertainty caused by the ongoing Covid-19 pandemic.

“ After years of interest rate declines it is also doubtful if we will see any more increases in equity price -to-earnings (P/E) ratios and so earning growth could become the main driver of share prices going forward. ”

The year to date has turned out pretty good thus far, for most equity markets, both global and local, despite lots of uncertainty caused by the ongoing Covid-19 pandemic.

In the sections below I would like to highlight some, but definitely not all, of the main market drivers over the past 12 months.

US Markets

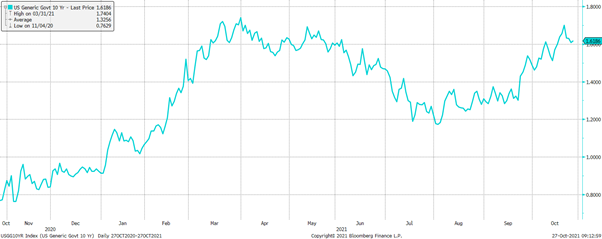

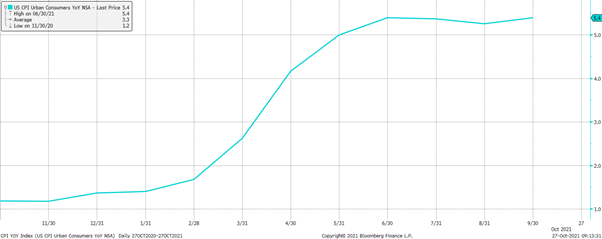

In the US, the S&P 500 increased at a nice pace, with a few scares along the way. The first bit of a wobble came during February and March when US bond yields started picking up. That was because investors started to worry about inflation and that the US Federal Reserve (Fed) might start raising interest rates earlier than previously indicated, putting upward pressure on bond yields. Remember that higher interest rates are negative for consumer spending and will affect profitability for companies with debt since they will be paying more interest. It also, perhaps most importantly, influences share price valuations. When interest rates rise, and all else holds steady, share valuations will likely be lower.

S&P 500

US Bond Yields

US Inflation

This was a recurring theme throughout the year, with investors being especially harsh on the tech sector which had a very good run since the onset of the pandemic. Note the big pullbacks every time the market started worrying about inflation, as can be seen in the performance of the tech heavy Nasdaq Index below.

Nasdaq

Market sentiment moved between inflation fears and Covid-19 pandemic expectations. The first would probably lead to higher rates and therefore lower ratings for sectors like technology. A longer drawn-out pandemic would probably still favour the so-called stay-at-home stocks which kept the tech sector in play along with very good earnings growth.

Lately, the Fed indicated that they will possibly start tapering their stimulus programme. In other words, they will start to scale down their purchases of financial instruments, thereby sending less money into the financial system to stimulate the economy. According to the Fed a rate hike is still a while off, but it remains to be seen if the inflation issue is just transitory as they claim, or if it will stay at the current high levels. If inflation remains at high levels, the Fed will have to act faster and more aggressively than they would like, which would be bad for markets.

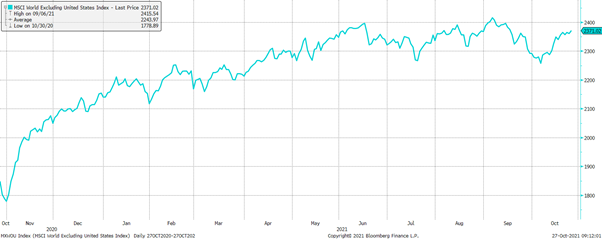

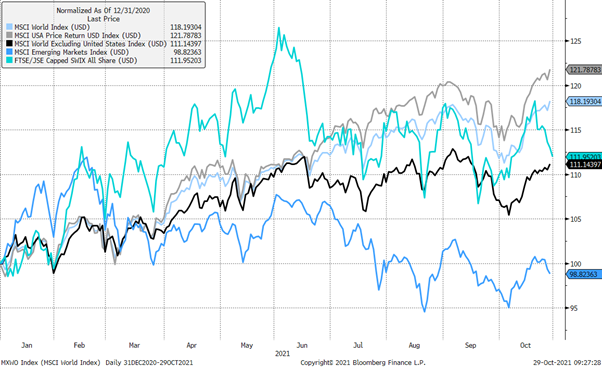

Other developed markets

The rest of the developed world, excluding the United States, started the year with a bang, but has fizzled out around June. This was mainly due to the lingering effects of the pandemic. Countries moved in and out of various forms of lockdown, supply chains where disrupted, economic growth stalled and inflation also started to emerge in places like Europe.

The gains in these markets up to March were also part of a move that started at the end of 2020 when the first vaccines where announced. The expectation was that the pandemic will end sooner and money will flow into shares that stood to recover and benefit from a normal economy. That hope waned as it became clear that the pandemic and government responses to it will last longer as new outbreaks occurred.

MSCI World excluding US

Emerging markets

Emerging markets started the year in the same fashion as the rest of the world and mainly for the same reasons. The first cracks appeared in February, but unlike the rest of the world and the US, they have not staged a recovery as yet.

The main fly in the ointment was the Chinese government with their regulatory crackdown on technology companies, which makes up a large portion of the index. A raft of new rules, which may impact the future profitability of these companies scared off investors and share prices subsequently tanked. This also negatively impacted South African investors who hold Prosus and Naspers, with their massive exposure to Tencent.

It will take a while for companies and investors to adjust to these rules, but a lot of the negatives may already have been priced into the stocks, which bodes well for the future.

China is also fighting inflation, with somewhat different measures than interest rates, which dampened the commodity rally, putting the brakes on local commodity shares as well.

MSCI Emerging Markets

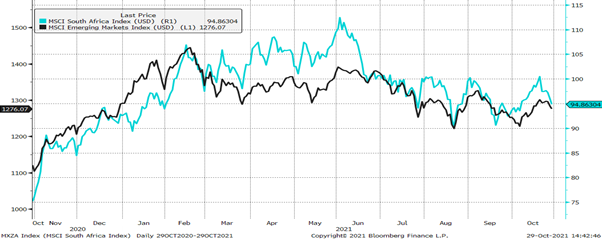

South Africa

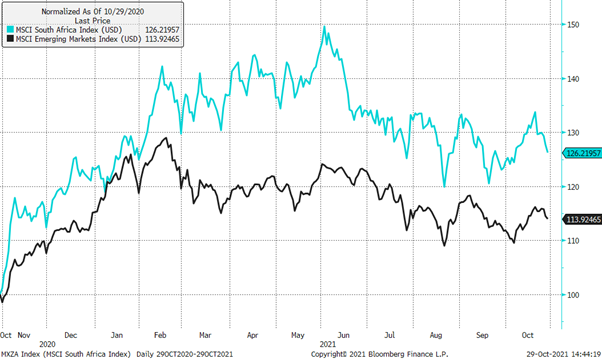

The South African market usually tends to blindly follow other emerging markets and this year was no exception.

SA vs Emerging Markets

Despite our own local problems like Covid-19 induced lockdowns, Eskom’s load shedding and SA civil unrest, the local market, somewhat surprisingly, managed to outperform other emerging markets over the past year as can be seen below.

SA vs Emerging markets rebased

To put our performance into perspective, look at the graph below. It shows what US$100 invested at the beginning of the year would have grown to, as of 29 October.

Indices rebased to 100

Despite massive volatility we were still one of the better performing markets over this period.

SA bonds

Local bond rates followed the rest of the world with a bit of a tick up in risk premium seen towards the end of October, probably as result of uncertainty around local elections. Remember, the more uncertain investors are, the higher the return they require, to compensate for risk. Therefore, uncertainty leads to local rates moving up a bit more than their international counterparts.

SA 10-Year Yield

The Rand

After an initial recovery from 2020 lows the Rand stabilised between R14 and R15.50 to the dollar, again despite everything going on locally. Unless something really untoward happens, we expect this to continue.

We expect the main themes that have driven recent share prices to continue, with more emphasis on inflation and interest rate expectations as we draw closer to the first rate hike in the US.

Economic growth, and especially company earnings growth, will also become very important. A lot of the growth we have seen this year came off a very low base as a result of the pandemic and global lockdowns last year and it remains to be seen how sustainable it is.

After years of interest rate declines it is also doubtful if we will see any more increases in equity price -to-earnings (P/E) ratios and so earning growth could become the main driver of share prices going forward.

Another thing to look out for is the oil price, which ran very hard, and its impact on inflation and economic recoveries around the world. Higher energy prices eventually lead to companies increasing the selling prices of their products to maintain profitability. That will lead to higher inflation, but also through pressure on the consumers wallet, to lower economic activity.

Brent Futures Contract

Also be aware that the Chinese are not the only ones trying to rein in the power and reach of big tech companies. Expect some regulatory changes for these companies across the globe.

With regard to geo-politics, the one area that stands out to watch is China and its stance towards Taiwan, which could cause major disruption in the region and for emerging markets as a whole.

Given all of the above we still see value in emerging markets, local bonds and selected stocks and sectors across the globe.

As always, we try to maintain a balanced view and portfolio that should do well in multiple scenarios and we don’t bet everything on a single outcome.

Stay Informed

Sign up for our newsletters and receive information on finance.