Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

23

June 2021

Purpose and functions of medical schemes

Estee Beetge

Wealth Adviser

A medical scheme provides liquidity to pay for medical-related expenses. If provision has not been made for these expenses or an emergency arises, other investments will have to be used to pay for the treatment. A medical scheme is strongly advised to form part of your wealth protection plan.

“ A medical scheme is strongly advised to form part of your wealth protection plan. ”

A medical scheme provides liquidity to pay for medical-related expenses. If provision has not been made for these expenses or an emergency arises, other investments will have to be used to pay for the treatment. A medical scheme is strongly advised to form part of your wealth protection plan.

The typical product range of medical schemes

Medical schemes typically offer the following plans, to meet various medical needs:

Basic care option: Provides members with cover for basic care (such as GP visits) through a network of providers.

Hospital plan option (major medical expenses): Provides members with cover for procedures that require hospitalization.

Day-to-day care option: Provides members with cover for day-to-day costs, such as GP and dentistry services, at the member’s own chosen service provider.

Medical savings plan: Allows members to allocate a portion (up to certain maximum percentages) of their contribution towards an individual savings account, which can be used to pay for medical services not covered under their scheme option.

Fully comprehensive plan option: This option typically covers all the above medical needs.

Please take note – PMB’s or Prescribed Minimum Benefits consist of a list of conditions that all medical schemes need to cover on all the health plans offered to members. The PMB condition must be paid from the risk pool, in full.

When deciding whether a condition is a PMB, the doctor should only look at the symptoms and not at any other factors, such as how the injury or condition was contracted. This approach is called diagnosis-based, and each diagnosis has a specific required treatment plan which is the prescribed minimum benefit. The minimum treatment required is the treatment a person would receive for that condition in a public hospital.

There are 270 serious health conditions and treatment pairs as well as defined emergency medical conditions, and 25 chronic diseases.

Health Insurance Products

Health insurance products are top-up insurance products for medical scheme members, or as standalone offerings that are independent of medical schemes. These policies pay out a stated benefit upon hospitalization, usually per day spent in the hospital. The stated benefit is unrelated to the actual cost of any medical service, as it is aimed at covering incidental costs.

Gap Cover Products

These policies cover the shortfall between medical scheme benefits and the rates that private medical service providers may charge in hospitals.

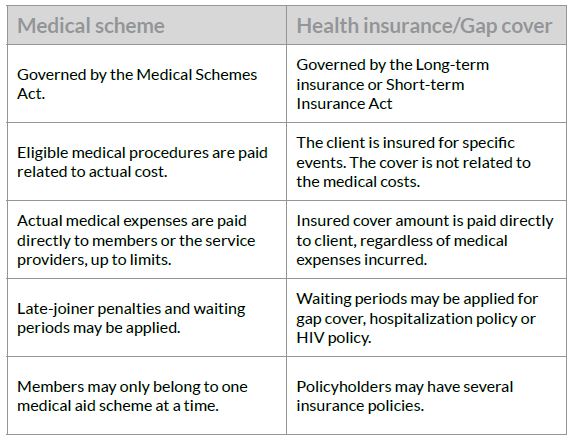

Table of difference between a medical scheme and health insurance/gap cover products:

Source: Moonstone Business School of Excellence – Health Service Benefits

The opinions expressed in this document are the opinions of the writer and not necessarily those of PSG and do not constitute advice. Although the utmost care has been taken

in the research and preparation of this document, no responsibility can be taken for actions taken based on information in this article. Always remember the prudent way is to

consult your portfolio manager before investing. PSG Wealth Financial Planning (Pty) Ltd is an authorised financial services provider. FSP 728

Stay Informed

Sign up for our newsletters and receive information on finance.