Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

01

February 2022

We live in a world of binary outcomes

Neels Van Schaik

PSG Wealth

Many of our clients will know that our goal is to construct portfolios that consist of a handful of high-quality businesses. Different people may describe quality in different ways. Probably the most descriptive term that encapsulates high quality for us is resilience. Why so much emphasis on resilience?

“ The importance of understanding what you own circles us back to our initial comments about resilience. ”

We live in a world of binary outcomes. History over the past two thousand years is littered with examples of events that have taken a turn for the worst, or sometimes for the better, after teetering on a knife’s edge.

Think about how different the world could have been: if Charles Martell had not defeated the Umayyad armies in 732 AD; if Stalin had not overestimated the Allied nuclear capabilities after invading Berlin, and rather headed straight for Paris; or if Adolf Hitler’s speech at the Bürgerbräukeller in 1939 had lasted a few minutes longer, killing him in the umpteenth assassination attempt during the 1930s.

More importantly though, time-travel back to the eighth century, or the 1930s, as an investor. Given that we now know how history has played out, it is easy to contemplate which investments would have benefited from these outcomes, but at the time, events were so fluid that you could easily have bet on the incorrect outcome. The point is you just don’t know; nobody knows.

These are important considerations when thinking about the current geopolitical tension between Russia and the US regarding the Ukraine’s NATO membership. It is also relevant when thinking about the prevailing narrative regarding inflation and how this has shifted over the past few months.

Only a few months ago, the US Federal Reserve Bank (the Fed) – which employs roughly 400 PhD economists – was confidently predicting the transitory nature of current inflationary pressures that shaped their interest rate decisions at the time. Despite all its predictive muscle, the Fed has since done a complete pivot on its view of inflationary stickiness, and interest rates are now expected to increase more aggressively than many were expecting last year.

Investors are understandably concerned. Rising interest rates means that money/cash becomes more expensive, or more valuable in the hands of investors, which in turn means investors holding cash are less likely to swap cash for equities, bonds, commodities and other assets. When pundits refer to stock market uncertainty it is exactly this: what the appropriate interest rate level is where investors swapping cash for equities are happy that they are getting a better deal from equity returns than they would from cash, taking into account the potential dividends and growth in profits from the underlying businesses.

In short, nobody really knows what that level of interest rate is. A whole lot of people think they do, to the extent that a whole industry has developed around these perceived predictive proficiencies. However, the unpredictable nature of markets stems from these uncertainties and is also the reason why share prices sometimes decline, sometimes a lot. While unnerving, these declines should be judged in the context of long-term returns that could be achieved by patiently riding out market corrections or crashes.

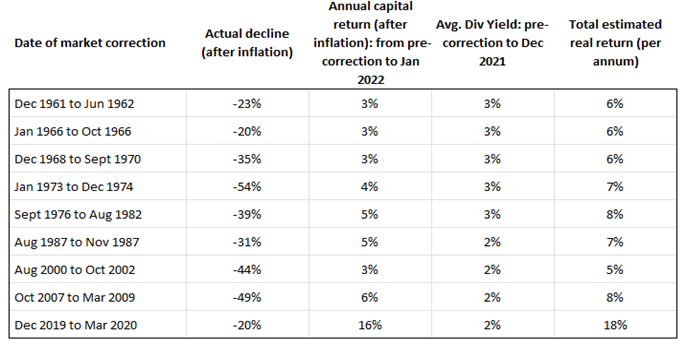

Consider, for example, the corrections of the S&P 500 (second column) since the 1960s in the below table.

Sources: IGraph, Robert Schiller, PSG Tygervalley

Despite these market crashes investors still earned an adequate total return after inflation (last column) if they rode out the market crashes.

The news headlines in recent months paint a picture of elevated uncertainty, whether it is about geopolitics, inflation or interest rates. This is fertile ground for market commentators wanting to be first to predict a pending market crash.

How investors react to these headlines is a choice though, which is a function of their understanding of the underlying assets they own, how these fit into their long-term wealth creation objectives, as well as the market fluctuations they can stomach.

The importance of understanding what you own circles us back to our initial comments about resilience. Resilience of a business has no bearing on its short-term share price performance, but it is indeed indicative of its ability to survive inflationary pressures and onslaughts from competitors, and the ability to exit bouts of economic and political turmoil as a stronger business.

Over years and decades, these companies end up with better margins and higher returns on capital, translating into more cash that can be reinvested or paid out to shareholders. The market tends to reward these businesses over time with higher valuations. Resilience creates consistent value to shareholders that will reflect in the share prices of these companies.

Investment writings at the start of a new calendar year are often filled with prognostications and expectations regarding macro views or popular themes that are reflected in an underlying bias towards particular industries or companies. We tend to avoid exposing portfolios to these explicit themes or macro views. Popular themes are often where exposure to binary outcomes can be the greatest.

We do not know what the next 12 months will hold for investors, nor the next five years, in terms of equity market performance. That in itself is the wall of worry that all investors climb every day. What we can say with a reasonable amount of certainty is that the earnings power of our portfolio companies, as a group, is going to be much stronger three to five years from now. Investors will be rewarded for their fortitude.

The opinions expressed in this article are the opinions of the writer and not necessarily those of PSG. The information in this article is provided as general information. It does not constitute financial, tax, legal or investment advice and the PSG Konsult Group of Companies does not guarantee its suitability or potential value. Since individual needs and risk profiles differ, we suggest you consult your qualified financial adviser, if needed. PSG Wealth Financial Planning (Pty) Ltd is an authorised financial services provider. FSP 728

Stay Informed

Sign up for our newsletters and receive information on finance.