Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

23

June 2023

Investment review

Braam Fouche

PSG Wealth

We currently find ourselves with a very unique market sentiment. As South Africans, we are known for tackling issues with resilience and endurance, however, multiple factors impacted sentiment this year. Examples of pressing factors includes the ongoing war in Ukraine, accompanied by tension between China and Taiwan, fears about the health of the global banking system, and increased bond market volatility. With the energy crisis persisting, political tensions rising and the South African Rand reaching a new low, our South African economy is placed under severe pressure.

Feel free to reach out to PSG Wealth adviser Braam Fouche directly.

Governments are taking action against high levels of inflation, leading to interest rates being hiked aggressively by central banks. “The cost-of-living crisis” and “the need to increase unemployment” (yes, you read that right), are topics frequently mentioned by market commentators, and global citizens have one thing in common when it comes to being exposed to the cluttered information in the media. The information out there makes it difficult for citizens to maintain an objective view of the bigger picture, further necessitating the value of quality financial advice.

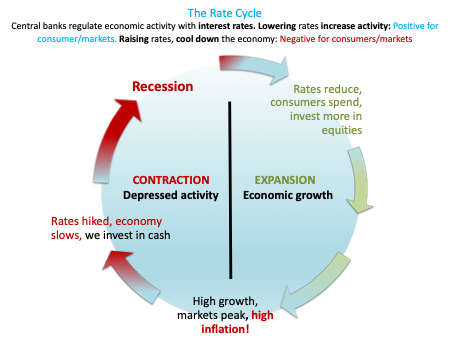

How we view investments in light of the interest rate and economic cycle:

The Rate Cycle

In a normal world we used to manage capital in accordance with the interest rate/economic cycle:

This cycle repeated every five to six years, and as reflected above, capital would be moved between equities, bonds and cash in accordance with the expansion or contraction of the economy.

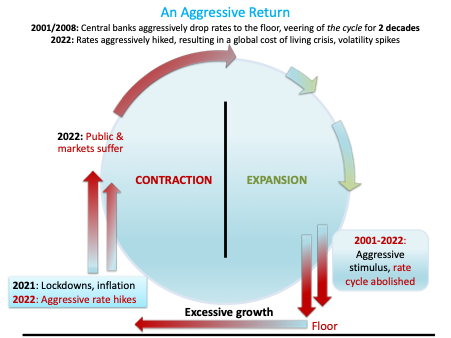

Deviating from the Cycle

During 2001, post-Dot Com crash, it all changed as the US Fed dropped rates extensively, sparking a global property and equity boom which lasted until 2008 when the Financial Crisis lead to large market corrections. Central banks reacted by dropping interest rates to the floor, which action was locked-in until 2022, when they collectively started hiking rates in reaction to “lockdown inflation”:

The cycle is disrupted, and those individuals who managed to retain their jobs and/or business are tied up servicing debt, whilst companies are under major pressure due to reduced economic activity and because of their own higher debt costs. The outcome is low growth, volatility, and reduced returns from the markets. The low interest rates that existed for such an extended period also skewed the valuation of many assets and in reaction to the current reversal we are compelled to restructure our portfolios.

Global view

Short-term interest rates in the US breached 5% p.a. whilst long bond rates are lower than short-term rates. This is referred to as the inverted yield curve and contributes to the deterioration of the balance sheets of banks, which is a real concern. Volatility remains high and rewards can only be achieved when we enter a downward rate cycle again. A prudent approach for investors would be to allocate their global cash to unitized portfolios of money markets and income funds, instead of leaving it in the bank.

Investors seeking returns in equity markets can consider the following:

- Gold

Debt is out of control, this applies to governments, business, and the public. Risk is as high as it has ever been which is driving the demand for gold.

- Strong balance sheets

Companies with low debt and with a competitive advantage (moat). An added advantage is a good dividend policy which enhances immediate returns for investors.

- Emerging markets

The re-opening of the giant economy of China, after an extended lockdown, is regarded as a positive event in a world of uncertainty.

South African view

The rand remains weak and during depressed times the SA public emotionally consider pursuing “greener pastures” in global markets, but blindly allocating capital to a strong US dollar combined with global uncertainty may not be prudent in the long run. SA interest rates are as high as 13% p.a. and increases in SA cash and bonds in the portfolio are almost a no-brainer. Investors still seeking opportunities in the equity market can consider stock picking in the financial, mining, and industrial sectors.

The benefit of our offering

The main benefit of our office’s managed portfolios is our active management of investments which are managed throughout the various economic cycles, and whilst many analysts are predicting a better 2024, we shall remain conservative in our approach until clear evidence of a turnaround emerges.

Stay Informed

Sign up for our newsletters and receive information on finance.