Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

12

December 2023

Getting the Most from your Bonus

Haydn Johns, Head of PSG Life and PSG Invest

PSG Wealth

There was a time when receiving a bonus was much more commonplace than it is today. For those fortunate enough to receive one, it may be tempting to splurge unnecessarily, but this article explains how carefully planning the way such funds are spent can amount to far greater benefits in the future.

“ Bonuses reward significant effort during the year, and the same effort should be applied to ensure they are spent wisely. ”

Better times may lie ahead

There are signs that things are slowly turning in the South African economic landscape. Although local inflation has remained high, the South African Reserve Bank (SARB) has fared well compared to its global peers in terms of managing inflation in the current environment. Interest rates have been high for an extended period, but are likely at their peak (or very close to it), and are widely expected to start dropping from the middle of 2024.

While state-owned enterprises remain in turmoil, the private sector is stepping in to give the economy the best chance of moving forward. For example, the most significant progress in accelerating electricity production has been achieved because of substantial investment in small-scale power installation initiatives by the private sector, and there are early signs that the electricity crisis will start easing during 2024. The Presidency is also considering seeking assistance from the private sector to address the long-standing issues plaguing state-run Transnet, which would have a very positive impact on our economy as it is heavily reliant on the export of commodities. These developments provide much hope and positivity for the future!

Navigating the present economic climate

When navigating these challenging economic circumstances, ensuring that you make the best possible use of any year-end bonuses you may receive is more important than ever. Bonuses reward significant effort during the year, and the same effort should be applied to ensure they are spent wisely. So, what should you consider when deciding how to allocate those hard-earned funds?

Pay down any short-term debt

Short-term debt is the costliest form of debt. Paying off short-term debt as far as possible will therefore improve your financial circumstances significantly. An example of this would be making outstanding payments on credit cards.

Start an emergency fund

Most people take on costly short-term debt because they don’t have an emergency fund for unforeseen expenses, so creating such a fund will help reduce the chances of incurring short-term debt in future. An emergency fund should take the form of an investment vehicle with a consistent return profile and low capital risk that is attractively priced to ensure returns remain competitive. Emergency funds also need to be accessible at short notice. The PSG Cash Account caters to this need and is available exclusively to clients of PSG advisers.

Contribute to your retirement annuity

Take advantage of your allowable retirement annuity (RA) contributions to get an instant effective tax return of 18-45%, depending on your marginal tax rate. You can contribute up to 27.5% of the greater of your taxable income or remuneration (up to a maximum of R350 000 per annum) into an RA. You will receive this refund after tax season opens and you have submitted your tax return. SARS is usually very efficient in refunding this money to taxpayers, and this tax refund can make for a great ‘Christmas in July’ present to yourself!

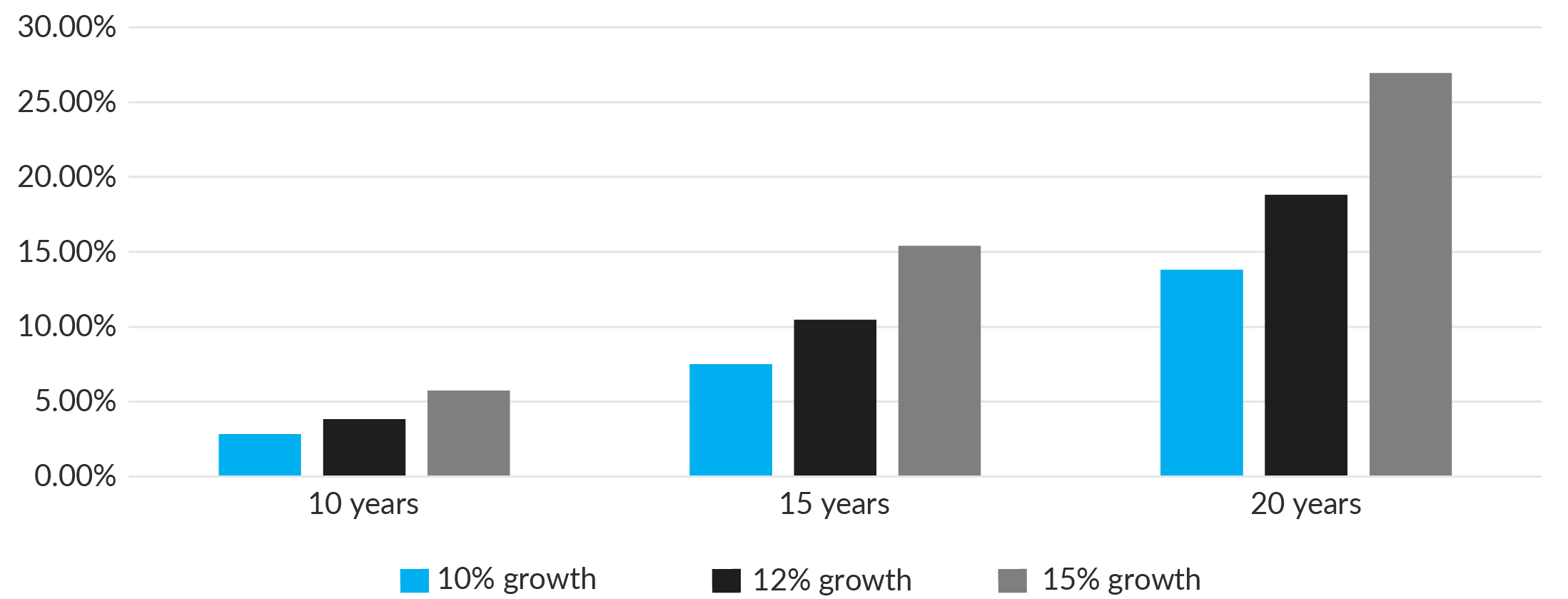

Invest in a tax-free savings account (TFSA)

All returns earned within TFSAs, such as the PSG Wealth Tax Free Investment Plan, are tax free, which significantly enhances the net returns from the investment when compared to voluntary investments, such as the PSG Wealth Voluntary Investment Plan. The earlier you invest in a TFSA, the longer the period you have to take advantage of the compounding effect on these enhanced net returns because of the tax efficiency of the product. The below is an illustration of the percentage by which a TFSAs value exceeds that of a voluntary investment over various periods.

36% tax bracket

Source: PSG Wealth. Assumptions: The maximum TFIP contribution limit of R36 000 per tax year is invested in both the TFIP and the VIP. Annual contributions cease once the lifetime limit of R500 000 is reached. The VIP assumes that the maximum CGT tax exemption is used at the end of each tax year. A tax rate of 36% has been applied.

Spoil yourself (within reason!)

The rule of thumb is that you need to save at least 20% of your pre-tax monthly income, and the inverse is valid for a bonus – that is, don’t spend more than a maximum of 20% of your bonus on yourself or other ‘wants’. You can consider this ‘spoil allocation’ as rewarding yourself for taking advantage of your annual allowable RA and TFSA contributions. If you are considering spending more than this guideline, it is recommended that you first consult with a financial adviser.

Additional options

If you have applied the recommendations already outlined above – including spoiling yourself within reason – and are fortunate enough to still have remaining funds, it is advisable to consider paying off long-term debt or investing in voluntary investments. Deciding between paying off long-term debt and investing in voluntary investments can be complicated and is dependent on various factors, which should be discussed with a financial adviser. These factors include the below.

- The interest rate on your debt compared to the potential return from the voluntary investment.

- How much you already have in the way of liquid assets. If your existing liquid assets are limited, you may consider a voluntary investment as liquid assets give you increased flexibility when making financial decisions.

- Your risk appetite. If you have a low appetite for risk, there is a higher likelihood that the potential return on the investment matching your risk profile will, at most, be equal to your debt interest rate. Furthermore, people with a lower risk appetite usually feel better if they pay off debt first. If either of these scenarios apply, it may be more appropriate to pay off your long-term debt first.

The success achieved by our world champion Springboks required the support of a coach, and the same holds true for making suitable financial decisions. A qualified financial adviser acts as a coach who helps you create a holistic financial plan and ensures you put in the required effort by making optimal financial decisions with your hard-earned money.

Stay Informed

Sign up for our newsletters and receive information on finance.