Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

05

October 2022

Using local investments to build a lasting legacy – the way to go, or duck and run?

Adriaan Pask, Chief Investment Officer

PSG Wealth

We believe diversification is the core of any top-performing portfolio, so it’s crucial to investigate South Africa as an investment destination.

“ We are optimistic about the prospects of most South African asset classes. ”

Looking at news headlines on loadshedding, corruption, labour disputes, damaged infrastructure, economic woes and more, it is easy to become disgruntled about investing in South Africa. However, one has to ask: “is this the objective South African story?” Don’t get me wrong – I’m by no means downplaying the severity of the issues our country faces, but I believe that staying objective in these conditions may be very rewarding in the long term. In this article I attempt to objectively answer four of the most commonly asked questions about investing locally.

Is there any merit in investing in South Africa?

The short answer is yes. We are optimistic about the prospects of most South African asset classes. Cash rates are much higher than what is offered aboard. Cash provides a good buffer against equity volatility, and as rates continue to increase, the opportunity cost of holding more conservative assets continues to decline.

Local bonds are generating attractive returns with yields in excess of 10% for longer-dated bonds. They also come with a potential capital upside if yields normalise. Last but not least, equity dividend yields are elevated and are attractively priced at current levels, which provides upside potential.

Cyclical counters like banks, selected commodities, and energy also seem attractive based on our research. However, these sectors are not the only ones offering value. Companies from other sectors are also offering value, which is why we rely heavily on our equity research team to aid in our selective stock-picking process.

Are the prospects of offshore investments not a better option?

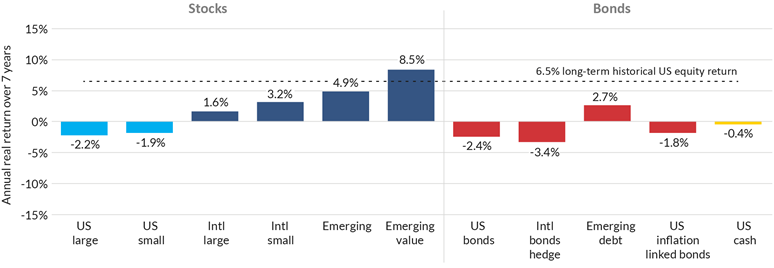

Many investors might want to make the most of market weaknesses by entering the global market. However, our research shows there are other downside risks in the near term that investors should be aware of. GMO Investment and Asset Management conducted research showing the outlook for various asset classes over the next seven years. The group’s findings support our view that emerging markets are likely to outperform developed markets. While the South African market, like many other emerging markets, is more vulnerable than resilient, it is within these vulnerabilities that experienced investors can find investment opportunities.

Graph 1: GMO’s expected real returns over the next seven years

Source: GMO. As of 31 July 2022.

*The chart represents local, real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ from those anticipated in forward-looking statements. US inflation is assumed to mean revert to long-term inflation of 2.2% over 15 years.

At the same time, we think material risks in the offshore landscape are being overlooked. Our key concerns are:

- Developed market bonds are still trading at negative real yields

As rates continue to rise, they could experience more resistance.

- A bad mix of lofty analyst forecasts for US growth shares and inevitable profit margin pressure

Consensus forecasts suggest that company volumes and profit margins are set to continue to grow. Our view, however, is that the economic growth story is far more vulnerable. Higher inflation will squeeze the level of free cashflow yield, and then add a subsequent derating. These could prove to be significant headwinds for global equities, particularly in the US.

- Liquidity withdrawal will most likely lift the veil on a highly indebted world and other overlooked weaknesses

In recent years, we have lived through a period of unprecedented monetary and fiscal support. It has always been a temporary measure to curtail greater economic loss. The thing with debt, however, is that it only buys time. It delays pain and affords you an opportunity to try and grow yourself out of the prevailing problem. The world did a good job to avoid a global economic collapse, but now the liabilities are high, and the cost of financing them is increasing as interest rates and risks escalate.

In short, investing offshore is not risk free. Some risks may even be more severe than the ones faced locally.

What about the poor South Africa economic backdrop?

Firstly, it is important to understand that market drivers and economic drivers are not identical.

Equity market prospects are driven by earnings. Earnings are very broadly linked to the economy but are by no means the only driver of equity returns. One also needs to consider the prospects of a specific security to defy its environmental headwinds, the dividend yield, and the equity’s potential to either become cheaper (derate) or more expensive (rerate).

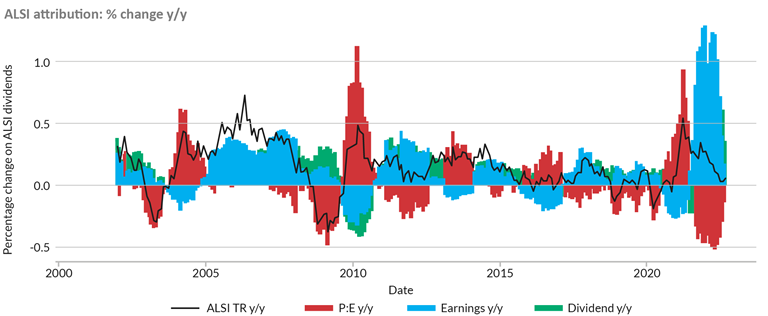

Much of the pain experienced in South African equities is not because of poor earnings. Profit margins are, in fact, high. Our markets are struggling because of a crunch on sentiment, and they simply continued to derate.

Graph 2: Attribution of price, earnings and dividend on the FTSE/JSE All Share Index (ALSI)

Sources: I-Net, Bloomberg

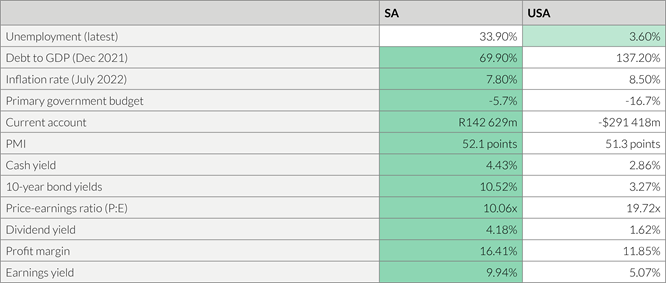

Secondly, the disparity in economic prospects between SA and the US is much less clear than generally believed.

When it comes to deciding whether the US or SA has better investment potential, the debate is usually around the perception of the two countries. These perceptions are influenced by the unemployment rate, business confidence and consumer confidence, among other things, and this tends to favour the US. The market side of the debate (which tends to favour SA) is, however, frequently ignored. It is cheaper to invest in SA. Moreover, investors in SA markets get higher yields and higher returns, and the long-term perception (the yield curve slope) is seen to be better in SA than in the US when comparing the market performance delivered by the two countries.

Over the past 15 years, it has been favourable for investors to diversify their portfolios by investing locally and offshore, with offshore being the alpha generator and local the diversifier. This was due to the growth potential of the US and the rally in its markets. However, given that our current economic state differs from the previous 15 years, a different investment approach should be taken. SA investments have now become the option with more alpha generation potential than the US, meaning the shift should be the inverse of the preceding 15 years.

Table 1: US and SA economic and market data

*Data as at 31 August 2022

Sources: PSG Wealth research team, Trading Economics

10-year bond yields 10-year bond yields are the returns investors get from the government when buying government bonds. Government debt to GDP Ideally, this compares what the government owes with what it can produce, and the output gives an idea of the country’s ability to pay its debt. Although SA is better positioned than the US (69.90% vs 137.20%), it has an upward trend in debt growth, whereas the US historically has a more stable debt-to-GDP ratio, with the last two years being outliers. Current account The current account records the net imports and exports of goods and services of a country. A positive balance means there are more exports than imports, and vice versa. Ideally, you want to invest in a country with a positive balance, such as SA. Manufacturing Purchasing Managers Index (PMI) The Manufacturing PMI indicates whether a country’s manufacturing sector is expanding (above 50 points) or contracting (below 50 points). The difference might seem marginal when comparing the PMIs of SA and the US (52.1 vs 51.5 points), but SA expanded by 4.5 points over the past month, while the US contracted by 0.7 points. |

What are the PSG Wealth Funds of Funds doing in terms of offshore versus local?

Our underlying fund managers make the tactical asset allocation calls in our PSG Wealth Fund of Funds (FoFs). Our fund managers are some of the most experienced and skilled available. The perceived opportunities and risks may vary across managers, and we therefore diversify across a range of managers. It is also important to note that some managers may identify these risks and can mitigate them effectively. They can then direct capital to more attractive or suitable opportunities.

Investors should also know that we still see the merits of offshore investing. However, we would argue that the proposition has shifted from one where offshore has been rich in opportunity since 2013, to one that is currently less pegged on returns prospects and more focused on offsetting domestic risks, like acting as a good diversifier.

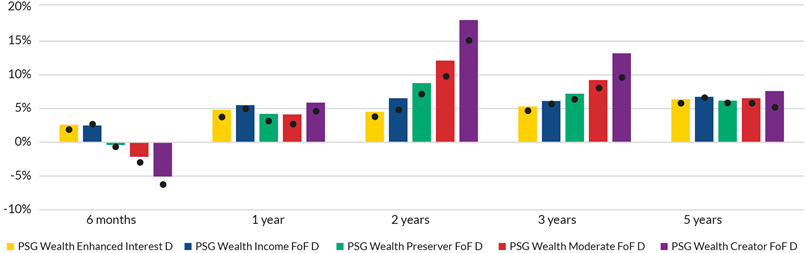

As illustrated in graph 3, the local FoFs of PSG Wealth continue to reach their targets and outperform their respective benchmarks over all long-term periods.

Graph 3: Local PSG Wealth Fund of Funds performances

*Dots represent the relevant benchmark

Data as at 31 August 2022

Source: PSG Wealth research team

Remember, the only uphill in your investment journey should be the returns and performance. So, speak to your adviser regularly to ensure you have a complete view of what your strategy is and how it is developing – and most importantly, to ensure your peace of mind remains undisturbed, despite continued noise in the market.

Stay Informed

Sign up for our newsletters and receive information on finance.