Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

30

April 2021

Are stock markets expensive?

Theo Cloete, Wealth Manager

Wealth

Are stock markets expensive?

“ Anyone can give advice, but objective and quality advice is priceless. ”

Finmonitor

Just over a year ago, global financial markets experienced a massive fallout, triggered by the Covid-19 pandemic. Towards the end of March 2020, as the effects and consequences of the pandemic hit home, most major stock exchange indices plummeted to frightening lows. Double-digit declines were the order of the day.

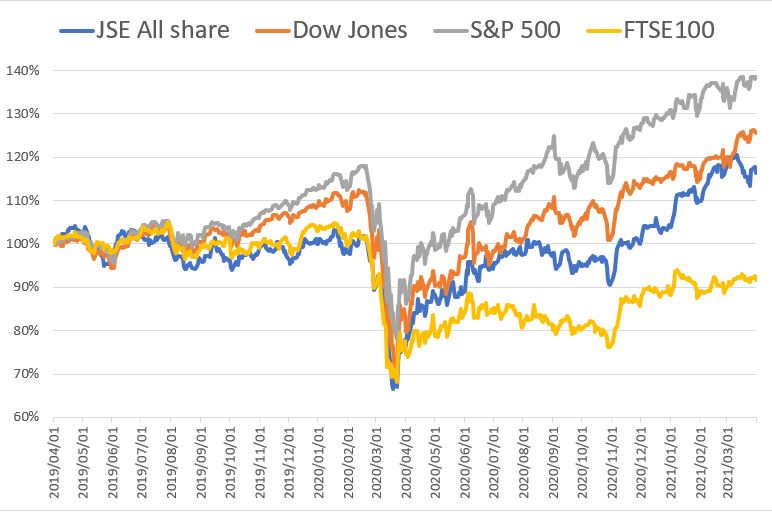

Fear-stricken investors fled the investment markets, leaving behind a trail of severely bruised share prices and tumbling indices. Now, merely a year later, most markets have recovered spectacularly and are even trading at levels higher than their pre-pandemic highs. The accompanying graph illustrates the extent to which the major indices fell and subsequently recovered. (This graph depicts the Dow Jones, S&P 500, FTSE 100 and JSE All Share Indices over a two-year period.)

As the graph shows, the S&P 500 Index in the United States was trading at record highs during the months leading up to the crash, when it fell by 33% between 21 February and 23 March 2020. Locally, the JSE All Share Index (ALSI) also shed 33% over the same period.

A dramatic and spectacular recovery since March/April 2020 is evident from the graph, with the UK’s FTSE 100 lagging the rest of the pack. The S&P 500 skyrocketed gaining 78% to the end of March 2021, again trading at record levels. The JSE ALSI recovered by 74%, more than wiping out the losses incurred a year ago.

However, taking a closer look at the shares included in the indices it becomes clear that in most indices the thrust was driven by clusters of high-performing individual counters. The US S&P 500’s recovery was mostly driven by shares in the ‘big tech’ sector. Here the likes of Apple, Amazon, Google and Tesla come to mind. Locally, in the case of the ALSI, the recovery was mainly driven by commodities and mining companies, as well as Naspers/Prosus.

One could therefore argue that, although the recovery has been significant and in some cases even spectacular, especially from an index point of view, there are sectors and shares – with potential merit – which have not recovered to the same extent. Take the South African banking sector as an example. The ‘big four’ banks (Absa, Nedbank, Standard Bank and FirstRand) are all still trading well below their pre-Covid levels. We are not necessarily advocating that one should buy these banks at current levels, but merely illustrating the point that the recovery has not been as broad-based as the indices would lead one to believe.

The Finmonitor team believes that, although some shares and sectors do appear to have recovered to expensive valuations, there are still potentially rewarding investment opportunities to be found in global and local markets, specifically in certain sectors and undervalued companies. Such opportunities should be sought and assessed by patient investors, taking a long-term view and sticking to the time-tested merit of appropriate risk diversification.

As always, we would recommend that investors seek the advice of qualified, experienced investment professionals before committing to firm investment decisions.

Note: The opinions expressed in this document are the opinions of the writer and not necessarily those of PSG and do not constitute advice. Although the utmost care has been taken in the research and preparation of this document, no responsibility can be taken for actions taken based on information in this article. Always remember the prudent way is to consult your portfolio manager before investing. PSG Wealth Financial Planning (Pty) Ltd is an authorised financial services provider. FSP 728

Theo Cloete is a Wealth Manager with PSG Portfolio Management & Stockbroking, Hermanus.

Stay Informed

Sign up for our newsletters and receive information on finance.