Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

12

May 2023

South Africa’s retirement legislation to be amended

Tian Ebersohn CFP®

Wealth Adviser

National Treasury will be implementing certain significant changes to South Africa’s retirement legislation. The changes are planned to take effect on 1 March 2024.

“ Government is sensitive to the fact that retirement fund members are experiencing financial distress, brought on or amplified by the Covid-19 pandemic. ”

Current legislation does not allow members to access retirement funds while they are employed. However, it does allow for taxable withdrawals from pension and provident funds upon termination of employment.

Through retirement reforms, Government aims to strike a balance between incentivising saving for retirement on the one hand, and providing retirement fund members with access to a portion of their retirement fund without having to resign from employment, on the other hand.

A new two-pot system

Legislation surrounding the new retirement reforms has not yet been finalised, but indications are that it will be published later this year.

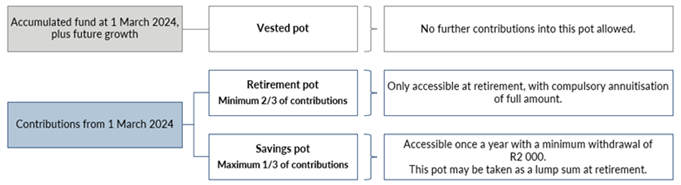

The two-pot system will allow members’ contributions to be divided or split into two separate ‘pots’. The first will be a savings pot and the second a retirement pot. Members will be allowed to contribute a maximum of one-third of their contributions to the savings pot and a minimum of two-thirds to the retirement pot.

This new structure will enable members who need access to funds to withdraw from the savings pot once a year without having to resign from employment. They therefore do not have to go to the extremes of resigning just to access funds which are beneficial not only to them, but also to the employer. The withdrawal, which is limited to once a year and a minimum of R2 000, will be taxed as ordinary income as opposed to being taxed as a lump sum withdrawal.

Through this new initiative, Government will therefore ease the accessibility of funds, but the new tax regime will hopefully discourage members to make unnecessary withdrawals.

Contributions to the retirement pot will only be accessible upon retirement, and the full amount will have to be annuitised, subject to the de minimis threshold.

Contributions made before 1 March 2024 will not be subject to the new legislation and will remain in a third pot (called the ‘vested pot’).

The diagram below shows the way contributions will be split from 1 March 2024 onwards:

Source: PSG Wealth

Aspects that still need to be addressed

As mentioned above, there are still uncertainties to be addressed before implementation of the new retirement reforms. Aspects regarding the accessibility and consolidation of members’ existing accumulated benefits into the two-pot system will need to be clarified before implementation.

Stay Informed

Sign up for our newsletters and receive information on finance.