Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

25

February 2022

Understand the financial risks facing a business

Juanita Myburgh CFP®

Wealth Adviser

It is important to understand the financial risks facing a business, to identify those risks and to implement appropriate action plans to mitigate them. One of the methods a business/company can use is key person insurance.

“ It is important to understand the financial risks facing a business, to identify those risks and to implement appropriate action plans to mitigate them. One of the methods a business/company can use is key person insurance. ”

Pretoria East 25 February Newsletter 2022

What is key person/key man insurance?

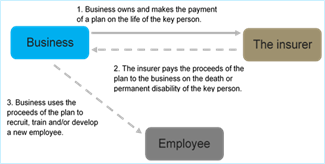

- Key person insurance is a life insurance policy that a company purchases on the life of an owner, a top executive, or another individual considered critical to the business.

- Such insurance is needed if that person's death would be devastating to the future of the company.

- In the case of a small business, the key person might be the owner or founder.

- The company is both the owner of the policy (policyholder) and pays the premiums due on that policy (premium payer) and is entitled to the proceeds payable from the policy (beneficiary).

The structure of key person insurance

The need/risk

Effective and well-trained staff are vital to the success of a business, especially staff with specialist skills or knowledge. Losing a key person could result in increased costs in a number of areas. These might include recruiting and upskilling a replacement, a slowdown in turnover, delays to or cancellation of a business project involving the key person concerned, and stricter terms from suppliers. In addition, such a loss could lead to difficulties in raising finance or having to settle loans, as well as issues due to delays in finding a successor and time lost during the settling-in period.

Key person insurance is the solution

Key person insurance allows an employer to insure the life of a key employee (or director) for the purpose of compensating the business for the loss of income it would suffer in the event of that person‘s death or disability – and, in some instances, even critical illness.

Benefits to the business

Upon the death or disability of the key person, the lump sum payment from the life insurance policy will provide cash to ensure that:

- funds are available for recruiting, training and/or development of a replacement;

- the business and its development can continue seamlessly; and

- the creditworthiness of the business is not affected.

The premiums payable in respect of such insurance may be tax deductible, or the proceeds of the policy may be tax-free.

The tax implications

*A ‘relative’ in relation to a person is defined as the spouse of that person or anybody related to them or their spouse within the third degree, or the spouse of anybody so related.

**A ‘family company’ is defined as a company other than a quoted company, which, at any relevant time, was controlled or capable of being controlled, directly or indirectly, by way of a majority holding of shares, or any other interest, or in any other manner by the deceased or by the deceased and one or more of their relatives.

Frequently asked questions

How is the value of the key person calculated?

In practice, the amount of cover that a business should take out on the life of a key person is usually determined by a combination of the following methods:

- The estimated number of years that it would take for a replacement to reach the key person‘s present level of profitability, multiplied by the drop in profits foreseen as a result of the death or disability of the key person; or

- Itemising the actual costs involved in replacing the key person.

What actual costs and other factors should be considered when calculating the value of the key person?

To ensure that continuity is truly achieved, it is advised that a comprehensive job description for the key person be available. This will enable a fairer valuation method and assist in finding a true replacement.

In addition, the following items should be considered when determining the costs associated with the death or disability of the key person:

- Recruitment cost of a person who can step into the shoes of the key person,

- Possible relocation costs if this person is sourced elsewhere,

- Training costs and further education costs,

- Cost associated with restarting special projects that the key person was involved in,

- A general loss of turnover due to the key person’s absence, multiplied by the number of years it is expected to take the replacement to perform at a similar level, and

- Any loan accounts that might be owing to that key person.

What happens if the key person leaves the business?

Where a key person leaves the employment of the business, there are two alternatives available to the business in respect of the policy it has on him or her.

How is the value of the key person calculated?

In practice, the amount of cover that a business should take out on the life of a key person is usually determined by a combination of the following methods:

- The estimated number of years that it would take for a replacement to reach the key person‘s present level of profitability, multiplied by the drop in profits foreseen as a result of the death or disability of the key person; or

Itemising the actual costs involved in replacing the key person.

What actual costs and other factors should be considered when calculating the value of the key person?

To ensure that continuity is truly achieved, it is advised that a comprehensive job description for the key person be available. This will enable a fairer valuation method and assist in finding a true replacement.

In addition, the following items should be considered when determining the costs associated with the death or disability of the key person:

- Recruitment cost of a person who can step into the shoes of the key person,

- Possible relocation costs if this person is sourced elsewhere,

- Training costs and further education costs,

- Cost associated with restarting special projects that the key person was involved in,

- A general loss of turnover due to the key person’s absence, multiplied by the number of years it is expected to take the replacement to perform at a similar level, and

- Any loan accounts that might be owing to that key person.

What happens if the key person leaves the business?

Where a key person leaves the employment of the business, there are two alternatives available to the business in respect of the policy it has on him or her.

Firstly, the business can cancel the policy, as it is no longer necessary. From a moral perspective, there is no longer any insurable interest between the business and the life insured and, therefore, the continued existence of the policy becomes questionable.

Secondly, the business can cede the policy to the life insured. In this instance, the business will effect an outright cession on the policy and the life insured will become the policyholder, the owner of the policy and also the premium payer. In such a case, the policy will become part of the personal life policy portfolio of the life insured.

There are no tax consequences to this cession. If the policy is ceded in this manner, it will no longer be tax deductible in the hands of the life insured (assuming it was tax deductible under Section 11(w)(ii)). The proceeds will pay out tax-free to the life insured or his or her beneficiaries and the policy proceeds will most likely be included in the deceased’s estate for estate duty purposes.

We can assist with various kinds of business needs, of which contingent liability, buy-and-sell and key person insurance are the most utilised solutions. Please feel free to contact us should you have any enquiries in this regard.

Stay Informed

Sign up for our newsletters and receive information on finance.