Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

31

October 2022

Economic and market overview

Dawie Klopper CFP® Wealth Manager

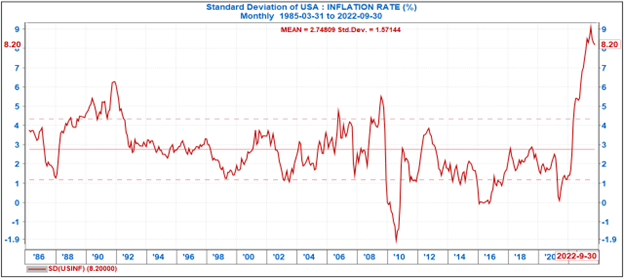

The main theme of my presentation at our biennial client event was that, suddenly, US inflation (graph 1) has become a major problem.

“ Any piece of good news – for instance, stabilising the power crisis in South Africa – will support a recovery in confidence levels, which in turn will contribute towards a market recovery. ”

Graph 1: US inflation

Source: Iress

Although caused by several factors, it also puts pressure on equity and bond markets. In fact, what we experience now – both the US bond market (10-year bonds) and the S&P 500 having declined by more than 10% since the beginning of the year – is the first ever (since 1927).

I also highlighted the growing geopolitical tension around the globe. JP Morgan CEO Jamie Dimon is more concerned about the escalating geopolitical tension than a US recession in 2023. China has just reappointed Xi Jinping for a third presidential term. Xi Jinping follows a shared prosperity policy, resulting in a less market-friendly environment. The Chinese economy has already slowed down to its slowest pace of growth in many decades and it is difficult to see how this trend will turn around soon. This has repercussions for the demand for commodities.

So, it is a very tough market environment. Fortunately (or is it fortunate?) the rand has also weakened, which provided some protection for the offshore component of clients’ investments. Saying that the rand fortunately weakened may not be accurate, as it causes imported inflation, which means interest rates should keep rising.

We should also acknowledge the fact that we are faced with a strong US dollar, not so much a weak rand. On the one hand, the increase in US interest rates is boosting the strong dollar, but on the other hand, it is putting equity markets under pressure. Currently, it seems as if interest rates are set to rise further, not stopping until US short-term interest rates exceed the inflation rate. It may take until Q1 of 2023 to reach the point where interest rates are higher than inflation. This means market volatility will continue, although we should not forget that equity markets tend to prematurely price in future events.

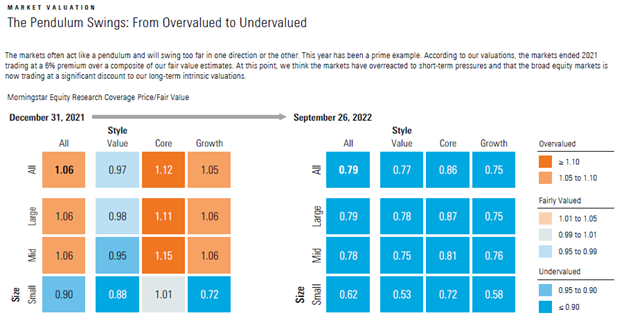

Nevertheless, current equity prices are offering value (according to Morningstar, a large US research firm). In December last year, the situation was reversed, with high US equity valuations due to fiscal support packages and ultra-low interest rates (graph 2).

Graph 2: Market valuations are now cheap

Source: Morningstar

So, if we reach the point where the pressure to hike interest rates is reduced or absent, markets may start rising again.

In South Africa, we are faced with a lot of negativities and the JSE is unbelievably cheap. However, we must ask what is needed to unlock value. Any piece of good news – for instance, stabilising the power crisis in South Africa – will support a recovery in confidence levels, which in turn will contribute towards a market recovery. Relative to the S&P 500, the JSE is now as cheap as it had last been in 2003.

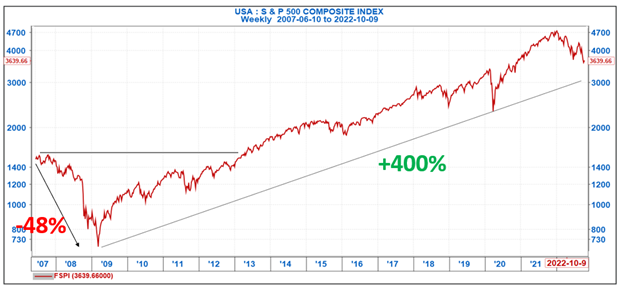

Locally, the last prolonged bear market occurred in 2008/9. At the time, our advice to clients was to stick to their plan and not to make any changes to their portfolios. Our advice is still the same. I realise emotions are terribly negative now and people feel ready to give up on their investments. However, if you did cash in your portfolio at the time of the market low in 2009 (following a 48% drop) you will have missed a 400% rally in the next 14 years (graph 3).

Graph 3: S&P 500 since 2007

Source: Iress

Stay Informed

Sign up for our newsletters and receive information on finance.