Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

15

July 2021

Quarterly Insight

Jan van der Merwe, Head of Actuarial and Product

PSG Wealth

Retirement is an important milestone that many of us look forward to with anticipation. Having built up a working lifetime’s worth of retirement savings, selecting the right annuity option to meet your income needs in retirement is important. You need to take the time to consider your income options carefully, which can be a daunting prospect. In this article, we explore the features of annuities to provide you with some guidance.

“ Living annuities provide the opportunity to pass on wealth to your beneficiaries. ”

Retiring soon? Here is what you should know about annuities

What is an annuity?

An annuity is a product that provides you with a regular income during your retirement. When you retire, at least two-thirds of your retirement fund savings must be used to purchase an annuity. One of your main considerations will be whether to purchase a life annuity or a living annuity.

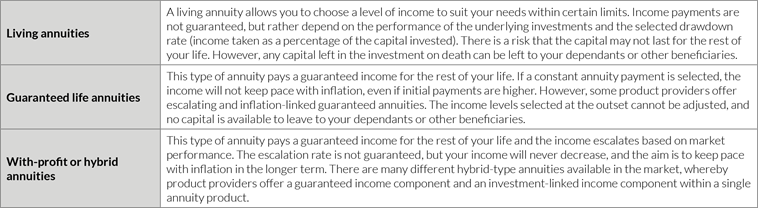

What are the key differences between a life (guaranteed) annuity and a living annuity?

The type of annuity suitable for you will depend on your unique circumstances. In general, the following types of annuities are available in the market:

For all types of annuities, the income will be taxed according to your marginal tax rate.

The key factors to consider at retirement

There are many factors that will influence your decision of providing an income in retirement. The key factors that you need to consider include the following:

- Understand your living costs in retirement – create a three- to five-year budget of your living costs at retirement. Start with your minimum living expenses. These may include food, housing and medical expenses. This will represent the minimum income you need. Keep in mind that living expenses will generally increase with inflation. A financial adviser can help you draw up a budget by doing a financial needs analysis for you.

- Consider your lifestyle – for example, take account of your hobbies or holiday preferences. Note that by drawing a lower income in the early years of retirement, you will have more later on to cover increasing inflationary expenses and possibly increasing medical expenses.

- Consider your accumulated savings from all sources and funds, and other sources of income outside of the annuity (e.g. rental income from a property you may own).

- Consider those who depend on your income – if you have a spouse or other people who are dependent on your income, take into account that they will require an income if you pass away before they do.

- Consider the state of your health – the healthier you are, the longer you are expected to live and the longer the annuity must last.

The main financial risks in retirement

Additional considerations when choosing an annuity

- Enhanced/impaired life annuities

Some life companies allow you to secure a higher monthly income as a result of certain medical conditions, since these may influence your life expectancy. - Guaranteed periods

In the case of life annuities, you may want to consider your need for a guaranteed payment period. This can be useful in the event of early death if the payments are required for a specific period (for example, if you have a few years of home loan payments remaining). - Marital status

Most life annuities can be purchased on a ‘single-life’ or ‘joint-life’ basis. Purchasing an annuity on a joint-life basis means that the annuity income will continue until the death of both you and your spouse. You may also be given the option to reduce annuity payments at the time of death of the first spouse. Living annuities allow you to nominate your spouse as a beneficiary to inherit the remaining funds upon your death. The funds can then be used to fund his/her needs as required. - Financial needs of loved ones

A life annuity does not provide a payment on your death and therefore is not suited to pass wealth on to dependants. However, living annuities provide the opportunity to pass on wealth to your beneficiaries if there are funds left over at the time of your death. These factors should be balanced against the need for a guaranteed income for life.

Top tips to make your retirement savings last

The first step to ensuring that your retirement savings last is to start off with as much in your savings as you can. This means that:

- you should not withdraw your retirement savings when changing jobs

- what you take as the cash component at retirement should be limited to what is necessary and, ideally, be much less than the regulated one-third

- If your circumstances allow, extend the time you are able to work to increase your retirement savings.

If you choose a living annuity, make sure you select a prudent annual drawdown percentage to maximise the number annuity payments you will receive. The drawdown percentage you select will depend on your age, your gender and whether you have dependants.

Selecting an annuity at retirement is not a simple task. It is important that you engage with a financial adviser to support you through this process.

Recommended news

Welcome to the latest edition of the Wealth Perspective

In this edition of The Wealth Perspective, Chief Investment Officer Adriaan Pask explores the pivotal role a financial adviser can play in helping you reach your financial goals. Head of Sales, Nirdev Desai, reiterates the added value a financial planner can offer an investor. Then Madelein Steenkamp, Legal Specialist in Technical Advisory Support, explains the process of winding up a deceased estate. With retirement on the horizon for some, our Head of Actuarial and Product, Jan van der Merwe, provides a handy guide to annuity products and their suitability. Finally, Technical Legal Adviser, Marguerite Marais tackles the realities of retrenchment and what options are available to you.

Read more

Industry Views

Great achievements do not happen by luck, nor do they happen in isolation. Whether it is gaining a well-respected tertiary education, a beautifully designed home, or successfully conquering K2 in the Himalayas, achieving most goals in life will likely require the services and support of skilled experts. In a world where knowledge and insight continually evolves, a do-it-yourself approach is not the smartest strategy. Financial planning is no different.

Read more

A word from our CIO

Substantial evidence shows that the global population is struggling to build sufficient reserves for a comfortable retirement. However, investors who make use of the services provided by reputable financial advisers tend to make better financial decisions. Skilled advisers support clients to approach saving in a more disciplined fashion and make better decisions.

Read more

Estate Matters

Losing a spouse or family member is traumatic enough; being unprepared for the financial realities of death can make it even more devastating. The moment a loved one passes away, their deceased estate comes into existence and must be wound up in terms of the Administration of Estates Act, and – depending on the nature of the estate – the winding up process can be lengthy. In this article I will unpack the various steps of this inevitable process.

Read more

Employee Benefits Insight

Unfortunately, given the turbulent time we are in, retrenchment has become a reality for many. Although often unexpected, is there a way to rebound from such a traumatic and disruptive event?

Read moreStay Informed

Sign up for our newsletters and receive information on finance.