Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

06

August 2021

Weighing up the investment case for commodity stocks - Angles & Perspectives

John Gilchrist, Chief Investment Officer

PSG Asset Management

In this article, we weigh up the investment case for commodities given current market conditions. Commodity companies are prone to boom-and bust cycles, and there is currently much debate around the sustainability of the current run-up in commodity prices. The team weighs in on how factors like decarbonisation, the environmental, social and governance (ESG) investing phenomenon and a renewed focus on capital discipline are impacting the commodity cycle.

“ Commodity markets move in pronounced cycles because sporadic surges in demand cannot immediately be met by increases in supply. This imbalance leads to high prices and wide profit margins, which incentivises capital spending, leading to lumpy additions of supply. ”

Weighing up the investment case for commodity stocks

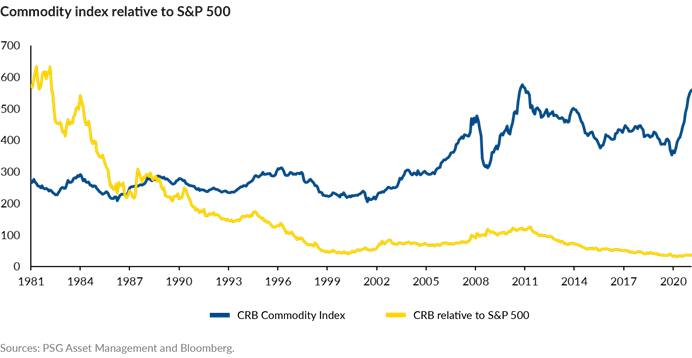

Commodities have been booming lately. Copper is 95% higher than in March 2020 (as at 14 July, and 50% above pre-Covid-19 levels) and has been reaching levels last seen in 2011. Oil is back above US$70, at levels that were not thought possible in a world phasing out fossil fuels, and with recent technological advances in oil and gas extraction (shale). This is the second commodity bull market in two decades. Just like in 2007, there is current debate around the likelihood of a commodity supercycle – a time when commodity prices trade significantly above their long-term price trends for an extended period. Unlike in 2007, when it was argued that Chinese demand drove the supercycle, proponents of the current potential supercycle point to the lack of new supply to meet future demand (which is likely to be supported by global infrastructure projects combined with substantial 'decarbonisation'-related investment). In case we had forgotten that the South African economy is heavily dependent on the fortunes of the commodities we produce, rand strength (until June) on the back of a trade surplus and budget overruns reminds us of the windfall that results from surging commodity prices, especially platinum group metals (PGMs). Unfortunately, when stock prices are buoyant, we tend to forget about the boom-bust nature of commodity cycles. It is worth remembering that the past two decades also saw vicious bear markets (2008 to 2009 and 2012 to 2016). Before that, commodity markets were in the doldrums from the late 1970s right through to the early 2000s when the Chinese growth miracle kicked into gear. Although the commodity index has had a good recent run, the performance still lags when compared to that of the S&P 500.

A reminder on the nature of the commodity cycle

Commodity markets move in pronounced cycles because sporadic surges in demand cannot immediately be met by increases in supply. This imbalance leads to high prices and wide profit margins, which incentivises capital spending, leading to lumpy additions of supply. We witnessed this phenomenon earlier this century when Chinese demand drove commodity prices, and we look likely to witness a substantial increase in demand again on the back of the green revolution and infrastructural ‘build back better’ initiatives.

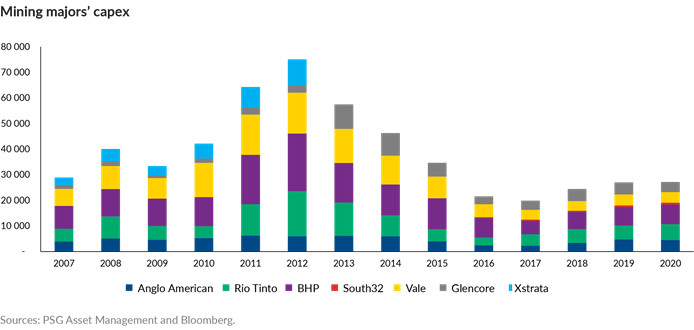

The chart below details the capital spend of the largest miners from 2007 to 2020. Note the supply response to ‘insatiable’ Chinese demand for industrial metals in the 2007 to 2012 period. BHP’s surging capex spend, rising from US$8 billion in 2007 to US$22.7 billion by 2012, is a poster child of the industry’s overall astounding 160% growth in spend from 2007 to 2012.

The rush to build mines in a time of very high commodity prices flooded the market with metals in 2012 to 2015, resulting in some of the mining majors having near-death experiences in late 2015 when Chinese demand eased at the same time that production capacity (supply) surged. Balance sheets that had used debt to finance expansion became very stretched and capital preservation – and in some cases capital raises (Glencore) – became the order of the day. Importantly, the 2015 near-death experience had a pronounced impact on subsequent investor psychology. The mantra from the institutional shareholder base ever since has been to prioritise restoring balance sheet strength first and thereafter focus on capital returns to shareholders. Shareholders’ demands have seen very high hurdles being set for allocating capital to expanding production or exploring for new deposits, and we have seen industry-wide capex all but coming to a halt. BHP has gone from spending US$20 billion a year on mine expansion in 2012 (total capital spend including maintenance US$22.7 billion) to paying US$20 billion back to shareholders this year.

Capital constraints also impact future supply

We have seen similar dynamics at play in the capital cycle for the oil and gas sector: a surge in production, followed by a near-death experience and a strong push for capital discipline and shareholder returns. In this case, abundant cheap capital and technological advancements (fracking) allowed a wall of production to be added in the US between 2010 and 2014 that shattered the OPEC hegemony. Over-indebted oil and gas producers in the US have had a very tough time since, undergoing many years of cash burn, bankruptcies, consolidation and a dramatic reduction in rig count. Like they did for the miners, capital markets have imposed strong capital constraints on oil and gas extractors, with the focus firmly shifting to capital discipline and shareholder-friendly payout policies.

The adoption of capital discipline by commodity producers has had a pronounced impact on future supply. Despite surging prices, exploration remains curtailed and given the long lead times (it can take more than a decade to develop a new large-scale copper project), supply of many commodities could be insufficient to meet robust future demand. Indeed, despite the run-up in prices, the message from the mining majors is that prices would have to be at sustainably higher levels to incentivise a meaningful return of sizeable expansionary projects. Also, the higher-grade deposits in ‘investor-friendly’ countries have been depleted and new supply of metals like cobalt and copper will have to increasingly be sourced in more challenging jurisdictions, like the Democratic Republic of the Congo (DRC).

ESG brings new pressures to bear

Beyond capital discipline at a company level, there is another giant contributor to potential supply constraints: the emergence of environmental, social and governance (ESG) investing. An ESG focus has become well entrenched in capital markets and it is difficult to imagine the influence of this growing trend diminishing anytime soon. That said, the ESG revolution is evolving and while the objectives are sound – holding corporations to higher levels of ESG standards – current implementation is sending tremors through financial markets. For example, the current social mood is firmly focused on the ‘E’ of ESG, with intense political pressure to impose aggressive targets for future greenhouse gas (GHG) emissions or to aim for carbon neutrality. Consequently, there has been a very strong push to divest from industries that are involved in the extraction of fossil fuels or other activities that harm the environment. While such steps and targets are well intended and a more proactive response to climate change is long overdue, things are far from simple and the risks of unintended consequences are extremely high.

The complexities bear some thought

For example, while it is all well and good to refuse to fund new fossil fuel production and mandate future production cuts, we should remember that even the most optimistic projections for energy transition anticipate it taking decades to overturn our dependence on fossil fuels for energy and transport. This is particularly the case in the developing world, which lacks the means to finance a speedier transition. A moratorium on new capacity to replace the existing oil, gas or coal reserves that will certainly be consumed in the decades ahead suggests a high likelihood of higher prices. Higher prices for dirty sources of energy will likely incentivise a speedier transition to greener energy sources, but will amount to a tax on poorer nations that cannot afford new renewable energy production or electric vehicles.

Furthermore, governmental commitment to carbon neutrality necessitates the aggressive roll-out of renewable production capacity and meaningful adoption of electric vehicles and other ‘green’ technologies. This transition is of enormous scale and will require significantly higher quantities of certain metals such as copper, nickel, cobalt, lithium and graphite.

Commodity demand is likely to remain supported

China remains the primary consumer of most commodities. Accordingly, a Chinese slowdown remains the largest demand risk to commodity prices. However, it is worth noting that much of the world is just emerging from the Covid-19 slumber and we are increasingly seeing various governments embarking on sizeable infrastructure projects to ‘build back better’ or provide economic stimulus. The US is in the process of signing off a multi-trillion dollar infrastructure plan. While future demand is inherently unpredictable, it is fair to assume that the dependence on Chinese industrialisation for demand will subside as the global decarbonisation initiative gains traction, other developing economies recover from deep recessions and mega-infrastructure projects are undertaken.

A pragmatic approach can deliver optimal outcomes

We prefer to take a pragmatic (and far more demanding) approach than many of our peers when it comes to investing in companies that produce fossil fuels. While many asset managers may decide not to invest in any such companies, or actively encourage these companies to divest from any fossil fuel exposure, this doesn’t actually address emissions. With global demand for fossil fuels likely to be underpinned by increases in developing market demand for a number of years, pushing the supply away from large public companies that are subject to extensive scrutiny could have material negative consequences, potentially even driving an unintended increase in emissions. Where resources companies are trading at substantial ESG-related discounts, we are open to investing and then supporting or driving reductions in emissions by these companies over time, in accordance with transparent public plans. We believe this approach will deliver the optimal outcome – both from a global emissions perspective and for our investors.

The saying goes that the cure for high commodity prices is high prices, as high prices incentivise more supply, while thrift, substitution and recycling weigh on demand. However, commitment to the decarbonisation agenda likely means that demand remains rigid for 'green’ metals, while supply is likely to be constrained for some time. This current status quo of healthy long-term demand for many commodities, in conjunction with constrained supply, supports our base case that the prices of many commodities will remain underpinned, and there is a reasonable possibility that some commodities could trade above trend in the years ahead. As always, we prefer to take a bottom-up approach in identifying varying risks and opportunities within materials and energy stocks and indirect commodity plays. A feature of the current investment environment is that global portfolios are heavily exposed to the winners of the past (passive, growth and the US), and the weightings of sectors like materials and energy in indices are low.

To illustrate, the weighting of the entire energy and materials sectors in the MSCI World Index reduced from 11% in June 2017 to 7.5% by June 2021, similar to the joint weight of Apple and Microsoft at 7.3%. The situation in the US market is even more extreme, with Apple at 6.2% of the S&P 500 being larger than materials and energy combined (5.3%).

We see attractive opportunities in the resources sector

Despite the run-up in commodity prices and recent price performance, many stocks can be acquired at attractive valuations based on normal commodity prices. While resources stocks are volatile in nature and have had a strong run over the past year, many are currently on favourable valuations, will return a lot of cash to shareholders and serve as very cheap hedges against future inflation, making them a compelling part of a portfolio. Given the attractive set-up we currently see in energy and materials stocks, the PSG Global Equity Fund had 27% of its assets invested in this space. We expand on some of these opportunities in the case studies that follow.

Case study 1: Royal Dutch Shell

Our process favours investing in companies with an inherent quality that is being overlooked by the market. Royal Dutch Shell (Shell) ticks the box on this front. Shell and its oil major peers have found themselves in the crosshairs of ESG activists and hostile governments and have come under intense pressure to hasten the transition of their portfolios towards greener energy. This increased pressure happened to coincide with the Covid-19-induced crisis, which caused the largest oil demand shock seen in non-war times. Anecdotally, 2020 saw Shell cutting its dividend for the first time since World War 2.

This set of circumstances has found Shell deeply out of favour with several market participants. They are unloved by ESG investors for their legacy fossil fuel businesses, which they have committed to descale in a rational fashion. And, paradoxically, they are disliked by oil bulls for offering less leverage to higher oil prices as they undergo this portfolio transition. Due to the dividend cut, Shell is also out of favour with income funds that owned the shares exactly for the stable dividends that the company paid out year after year. What is often overlooked amidst irrational and indiscriminate selling, is the inherent quality of the businesses in Shell’s portfolio, and that a contrarian investor can harness the opportunity to buy a very good business at an exceptional price.

The Shell portfolio has unique characteristics that sets it apart from its peers. Shell’s global footprint is astounding. There are 46 000 Shell-branded retail service stations in the world – more individual locations than McDonalds and Starbucks! This footprint underpins a value that is robust irrespective of the prevailing oil price. Furthermore, Shell has built the single largest liquified natural gas (LNG) business in the world, commanding more than a 20% market share. LNG is a critical energy source for countries that are transitioning away from coal-powered electricity, but do not have their own reserves of natural gas to allow for this. Through liquefaction, gas can be converted into a liquid allowing it to be transported to these countries. Shell has developed the means to supply its LNG in a completely carbon-neutral manner, allowing it to command premium pricing. We argue that the retail and LNG businesses alone are worth Shell’s current market value, which means at the current market price one is getting the core oil production and refining businesses for free – businesses that have generated more than US$100 billion in cash flows from operations over the last five years! We anticipate strong returns in the form of elevated future cash returns, plus a closing of the gap between the share price and a conservative valuation.

Case study 2: Glencore

Glencore appears particularly well positioned for the commodity environment described above. It is a low-cost producer of many of the ‘green’ metals required in a decarbonising world and has capacity to expand production into a strong market. Unlike other mining majors, it has retained its coal business for now, preferring to decommission the business responsibly. The coal division is likely to earn above-trend profits and generate a lot of substantial cash for shareholders, as pricing should be supported as outlined above.

Glencore’s management team remains the most aligned of the diversified majors. While the company is currently undergoing a CEO transition, the new appointee is an insider, supporting our view that capital is likely to continue to be allocated in a shareholder-friendly fashion. Glencore has come in for strong scrutiny of its governance practices in recent times and regulatory investigations are underway. This uncertainty and reputational damage have given rise to a depressed share price and poor performance relative to peers, creating an excellent entry point. Our detailed analysis and engagement with the company indicate a high likelihood of a narrowing of the Glencore ESG risk premium in years ahead and it is actually possible that the ‘green’ relevance of its products could gain a favourable perception. Its trading business generates consistent profits and thrives during periods of strong or volatile commodity prices, and its quality is underappreciated by the market. This has contributed to a persistently wide margin of safety and excellent leverage to a more constructive commodity cycle. We expect very strong cash returns over the next few years. Glencore is a core portfolio holding across all our funds.

Case study 3: Shipping stocks

PSG has been allocating capital to various ideas in the shipping sectors in recent years. These have included dry bulks (Grindrod Shipping and Star Bulk), containers (Maersk) and chemicals and tankers (Stolt-Nielsen, Ardmore and Euronav). The attraction of these ideas has been shaped by our analysis of the supply-side dynamics at play. In a very similar, but even more exaggerated version of the near-death experience in the metal and energy worlds, shipping markets have been decimated by a decade of excess capacity and the resultant very low shipping rates. The most astute shipowners observe that this is a boom-or-bust industry and all the money is made in a few short years. The last supercycle occurred during the early 2000s and during this period the Baltic Dry Index traded fivefold above the past 10-year average. Freight rates have shot up over the past year – container freight rates have increased fourfold over a year and Capesize freight rates are at levels last seen before the financial crisis. However, we believe we have the demand-supply ingredients that should support very strong rates for a number of years. Demand should remain robust as the world emerges from lockdowns, although some Covid-19-induced supply bottlenecks should ease. More importantly, we are observing very tight supply across most shipping sectors and, in the case of the dry bulks, the lowest order books for new ships ever seen. There are several contributing factors to the dearth of new ship builds – including a focus on balance sheet repairs and debt reduction, banks’ reluctance to extend capital to a ‘distressed’ industry, old ships battling to comply with emission regulations, and uncertain future regulations. All of these currently disincentivise new builds.

The combination of a very tough cycle and Covid-19 shutdowns saw shipping stocks trading at extraordinarily cheap valuations (large discounts to depressed book values) last year. The stocks have subsequently enjoyed spectacular increases – Maersk is up 240% and Grindrod Shipping has risen by 346%– amidst surging freight rates and rising ship values. Current cash flow generation is very strong, facilitating rapid balance sheet repair and healthy cash returns to shareholders. It will take a few years for new ships to be ordered and built in response to high rates and during this period, we anticipate high profits and cash returns. Accordingly, we continue to see attractive upside, especially in the dry bulk and tankers arena, and our clients retain healthy exposure.

Case study 4: SA Inc. stocks

Many of the stocks on the JSE tend to be positively correlated with the commodity cycle. Besides mining stocks, many other sectors are indirect beneficiaries of stronger commodity prices (we discuss AECI in ‘A differentiated approach to investing in SA equities’). Strong commodity prices tend to coincide with a strong global economic cycle, a weak US dollar and buoyant emerging markets underpinned by positive inflows of capital. Usually, the rand strengthens in such cycles. This helps put a cap on inflation and interest rates, further boosting domestic consumption. Thus, many SA Inc. shares have historically been indirect beneficiaries of sustainably high commodity prices. Their performance in this cycle has been mediocre. Is this time different, or are commodity prices set for a reversal? Otherwise, emerging markets and SA Inc. should enjoy their time in the sun as flows turn positive and confidence returns.

Read more about our differentiated approach to investing in SA Inc. equities.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

In this edition, we continue to look beyond the surface to find opportunities for our clients. Research and critical inquiry are part and parcel to our research process, and inform our differentiated positioning. We consider the macro views that form a backdrop to our fund positioning, unpack what ESG investing could mean for the current commodity run, and expand on our unique approach to the opportunities in the SA Inc. space.

Read moreIntroduction - Angles & Perspectives Q2 2021

Our value proposition to investors is to seek out great companies that are underappreciated by the market. We believe that if we buy such companies at a discount to their intrinsic value, they are likely to appreciate significantly in value in the long run. But markets, economies and companies are not static: conditions evolve on a daily basis, and what seems like a simple endeavour in theory, becomes a complex one in practice.

Read moreOur current views on the macro environment - Angles & Perspectives

Our panel of fund managers address some key issues around our macro views and how they feed into our portfolio construction process. Our CIO Greg Hopkins addresses the extreme market conditions and the perceived riskiness of our funds, Fund Manager Shaun le Roux explains why our cash holdings are low despite markets being at all-time highs, and Fund Manager Philipp Wörz delves into the global landscape and the resurgence of value as an investment style.

Read moreA differentiated approach to investing in SA equities in turbulent times - Angles & Perspectives

While many investment managers are coming around to our long-held view on the potential of the local market, we are in a unique position to exploit opportunities around SA Inc. shares. Fund Managers Shaun le Roux and Justin Floor unpack our approach to ensuring broader exposure to SA Inc. shares.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.