Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

24

January 2022

Only the start of an anticipated outperformance cycle from our differentiated approach - Angles & Perspectives

John Gilchrist, Chief Investment Officer

PSG Asset Management

Fund managers need to approach the world differently from competitors to deliver outperformance in the highly competitive world of investing – they need to both think and act in a differentiated manner. Behavioural biases and business pressures make truly independent thinking and positioning in portfolios extremely rare.

“ “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” - Benjamin Graham ”

Only the start of an anticipated outperformance cycle from our differentiated approach

Fund managers need to approach the world differently from competitors to deliver outperformance in the highly competitive world of investing – they need to both think and act in a differentiated manner. Behavioural biases and business pressures make truly independent thinking and positioning in portfolios extremely rare.

As Nobel Prize laureate in economics Daniel Kahneman outlines in his 2011 book Thinking, Fast and Slow, human beings have evolved to default to simplification, frequently using heuristics (mental shortcuts or rules of thumb) and intuition to make quick decisions. In the extremely complex world of investing, this tendency results in simplistic generalisations that drive mainstream opinion and market sentiment. An inherent assumption frequently underlying these generalisations is that the recent market environment will continue into the future. Recent examples of these heuristics include ‘traditional energy is uninvestable because renewables are the future’, 'South Africa is a hopeless case and meaningful growth will never return’, 'inflation is transitory', and 'in a post Covid-19 world REITs are uninvestable'. These generalisations are binary in nature, leaving little scope for the nuances and shades of grey that are always part and parcel of any investment decision.

Our 3M approach helps us take advantage of market opportunities

At PSG Asset Management, our long-term focused, non-benchmark cognisant approach allows us to exploit these oversimplistic generalisations by investing in out-of-favour areas of the market. Our 3M approach (considering moat, management and margin of safety) steers us towards cheap investment opportunities with overlooked inherent quality. While this approach can occasionally lead to us being early, especially when market generalisations persist for extended periods and become accepted as fact, we firmly believe that this approach will deliver the best long-term returns for our clients.

Benjamin Graham, the so-called father of value investing, said “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” Eventually, quality out-of-favour shares become too cheap, with the valuation underpin (dividend yield, free cash flow yield, short-term low earnings on a low multiple) prompting value-orientated investors to buy, and this activity causes the share prices to rally. As Justin Floor outlines in his article Barbarians at the gate: JSE mid-caps on the shopping list, we have seen a recent flurry of South African mid- and small cap buyouts by long-term private equity and industry buyers.

Opportunities remain in our portfolios

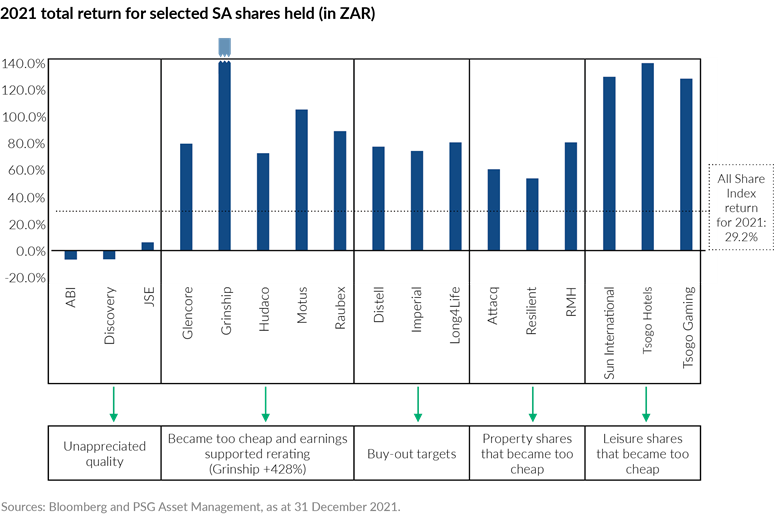

While our portfolios have benefited from numerous valuation-driven rallies that run counter to the prevailing market generalisations, not all of our holdings have rallied:

In our global portfolios we saw a similar pattern in 2021, with our US REIT holdings each rallying more than 115% in ZAR and out-of-favour commodity-related counters (including shipping, energy and fertilisers) also rallying very strongly (up between 44% and 210%).

The obvious question is whether we can sustain the strong performance going forward?

While many of our shares have rallied strongly, some of our most attractive positions have underperformed. In any diversified portfolio, you expect (and want) different shares and sectors to outperform at different points in time. We believe these positions are poised to deliver extremely strong returns for a number of years.

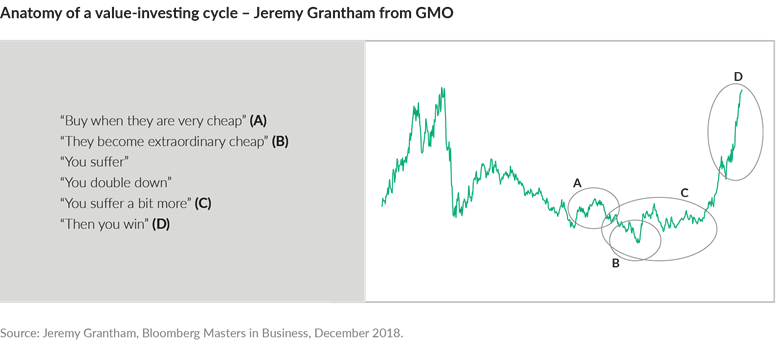

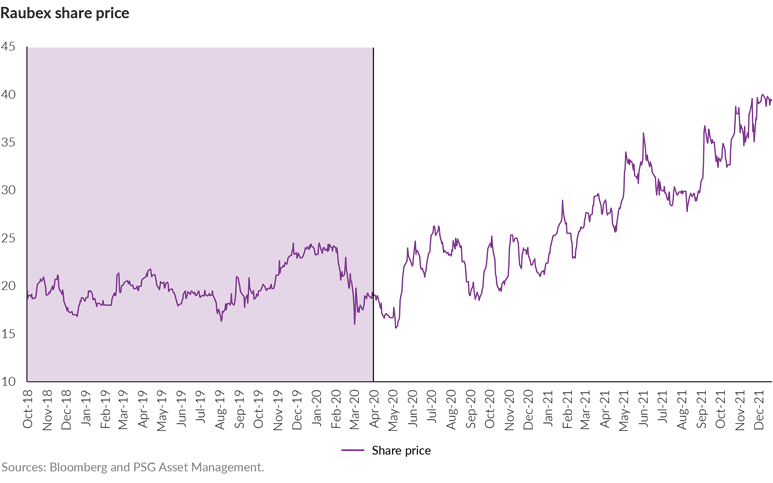

Out-of-favour shares can and do often move into a virtuous circle (with earnings increases driving increases in the share rating), ultimately delivering phenomenal returns for those who are willing to invest when the share is completely out of favour, and hold the positions through the subsequent rally. As an example of this, in the January 2020 Outlook presentation we demonstrated the anatomy of a value-investing cycle as outlined by Jeremy Grantham from GMO using Raubex (2018 to 2020) as an example:

From the end of January 2020 to the end of March 2020, Raubex dropped 26%, before rallying 125% over the next nine months.

Despite this rally, Raubex is still only trading at approximately 7x normal earnings. There are only two listed South African-focused construction companies remaining (compared to seven in 2015). With the company enjoying what the CEO has described as the best operating environment he has seen in 30 years, and a strong net cash balance sheet, we believe the company’s best days could be ahead.

Our portfolios offer many other similar examples

There are several other shares in our portfolio that have moved from the ‘suffering’ to ‘winning’ phases, as illustrated in the anatomy of value-investing chart above. We think many of these companies’ futures are still very bright, like that of Raubex.

Macro aware, with potential upside from an inflationary environment

While we are bottom-up investors, we are macro aware, and we believe that there are many credible signs that the low growth and low interest rate environment of the last decade is likely to change. In the US, we see substantial evidence that an inflection point (with higher growth, inflation and interest rates going forward) is likely:

Growth pressures:

- Households have never been richer (in terms of net wealth) and household debt service as a percentage of disposable income hasn’t been lower since the early 1980s.

- Renewables and infrastructure spending are likely to expand significantly, supporting growth for several years.

- Covid-19 opened Pandora’s box in terms of governments providing direct fiscal support to individuals, and it is likely to be an ongoing feature going forward (supporting growth).

- Deglobalisation trends following Covid-19-related supply issues could add further impetus to capex.

Inflation pressures:

- Labour remuneration as a percentage of GDP bottomed in 2018 and has risen significantly since then (while labour markets remain extremely tight).

- Long-term supply-demand dynamics support continued inflation pressures for a number of years in various commodities.

- US inflation reached 7% year on year in December 2021, the highest level since 1982.

The US Federal Reserve (the Fed) has finally acknowledged that inflation is not transitory and that they need to remove quantitative support and start raising the federal funds rate in 2022. The December 2021 minutes revealed that some members suggested that reducing the Fed’s balance sheet (i.e. selling bonds) would also potentially be required sooner than the market expected.

We believe we are well positioned for an inflationary environment with rising interest rates. Indices, and in particular the S&P 500, are dominated by high growth companies that are particularly interest rate sensitive, while our portfolios currently are behaving more like value-based portfolios and outperforming in a rising interest rate environment.

As bottom-up investors, we don’t assume that global inflation and interest rates will rise. We believe our investments are attractive, regardless of the prevailing economic environment. However, if we do see interest rates rise, this could provide significant additional tailwinds for our portfolios. The extreme market positioning in what has worked for the last decade (a period characterised by low inflation, growth and interest rates) has resulted in many neglected high-quality companies in other parts of the market. Philipp Wörz’s article Global equities – Beware the rearview mirror gives some examples of where we are finding value globally, and the extremely attractive risk-return trade-offs on offer should the future investing environment be more nuanced than the period since the Global Financial Crisis.

We are excited by the prospects for our funds

Our differentiated investment approach has delivered exceptional returns over the last 18 months, as certain out-of-favour areas have outperformed. Despite this, we believe our current portfolios still offer exciting opportunities – some shares and sectors have not rallied strongly (yet), while others have moved from being excessively cheap to simply being cheap. In addition, we feel we have attractive optionality to an inflection point in global markets baked into our portfolios that could provide significant additional performance.

PSG Asset Management is a wholly owned subsidiary of PSG Konsult Group.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

In this edition, we debate why it is important that fund managers differentiate themselves, and then explore how our funds deliver on this imperative. In the first article, Fund Manager John Gilchrist outlines how our 3M philosophy empowers us to deliver long-term outperformance to our clients. Next, Fund Manager Justin Floor finds validation for our views in the recent flurry of interest in mid-cap companies on the JSE. Lastly, Fund Manager Philipp Wörz argues that despite the perception of global markets being expensive, opportunities remain for selective investors using a differentiated approach.

Read moreIntroduction - Angles & Perspectives Q4 2021

Investors often resort to mental shortcuts and rules of thumb to speed up decision-making, and tend to extrapolate the recent environment into the future. This encourages a binary outlook (value vs growth, e-commerce vs bricks and mortar) and, as investors pile into what has worked in the past, markets can be driven to extremes. Taking a view that is different from the consensus outlook can be challenging and may seem foolhardy, especially if anomalous market behaviour persists longer than expected. However, this behaviour also creates opportunities for patient investors who are willing to look beyond such oversimplifications and question prevailing narratives. We would also argue that this approach is essential to assuring long-term outperformance.

Read moreBarbarians at the gate: JSE mid-caps on the shopping list - Angles & Perspectives

It is becoming increasingly apparent that there is something valuable hidden on the JSE. The last while has seen a notable surge in activity from private buyers signalling that they see opportunity in JSE-listed mid-cap companies. Private equity, industry players (particularly foreign companies) and even some management teams are taking listed companies off public markets. This zeal and optimism contrasts with the prevailing sentiment we are still observing on the JSE: many smaller, domestic-oriented companies trade below their reasonable fundamental value and pessimism and disinterest continue to prevail.

Read moreGlobal equities – Beware the rearview mirror - Angles & Perspectives

A globally integrated investment process – different by design. At PSG Asset Management, we have been investing in global equities since 2006. Our global process serves the offshore component of our local funds and our stand-alone global funds. Constructing a portfolio of one’s best ideas can be a challenging task, even in the relatively small local market such as the JSE, and even more so globally.

Read moreStay Informed

Sign up for our newsletters and receive information on finance.