Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

18

November 2025

Opportunities unseen: finding what others have missed - Angles & Perspectives Q3 2025

Philipp Wörz, Fund Manager

PSG Asset Management

Greg Hopkins, Deputy-Chief Investment Officer

PSG Asset Management

Opportunities unseen: finding what others have missed

Investors have experienced extraordinary times in markets since the beginning of the year. The outlook has swung from exuberance to despair (amidst the announcement of US President Donald Trump’s Liberation Day tariffs on 2 April 2025), and more recently, back to exuberance. However, one element that has remained consistent throughout the roughshod journey this year, is that valuations of US equities have remained at elevated levels. Despite record levels of market concentration, geopolitical risks, and a concerning US debt trajectory, investors have continued crowding into already popular US equities – and the Magnificent 7 (Mag 7) stocks in particular.

However, this apparent strength masks an increasingly complex and uncertain investment environment. Investors are faced with a market that is both heavily concentrated and richly valued, particularly in the United States.

Nevertheless, despite the risks we believe there are substantial opportunities for investors who are prepared to look beyond the obvious and embrace a truly global, actively managed approach.

Concentration risks in global markets

There is a growing sense of perplexity about how long markets can continue to defy fundamentals. For many years, investors have favoured the world’s largest and most recognisable companies, most of which are US-based and dominate the S&P 500 and MSCI World Indices. This has proven to be a rewarding strategy for an extended period. However, the structure of global markets now poses important challenges:

- US dominance of global indices: The United States accounts for approximately 73% of the MSCI World Index – a concentration level not seen since the 1970s.

- Elevated valuations: The S&P 500 Index currently trades at a forward price-to-earnings multiple of around 23x, nearly 40% above the long-term average since 1990.

- Heightened complacency: Market participants appear largely unfazed by the fiscal, political and geopolitical risks currently facing the US, leaving little room for disappointment.

US policy changes are contributing to inflections in global markets

Despite this sense of complacency, which seems to be pricing in a continuation of the status quo, few trends last indefinitely. Post Covid, we have already seen a number of economic and macro inflection points being reached, with the structural rebound of interest and inflation rates from historically low levels providing a case in point.

More recently, US President Donald Trump has made it clear that he favours a weaker dollar policy, which holds major implications for liquidity constraints and markets outside the US, and emerging markets in particular, as their economies are less likely to be hamstrung by a strong dollar. Trump’s policies have also forced other countries to put their own houses in order – for example, by highlighting the need for Europe to increase spending on infrastructure and defence substantially.

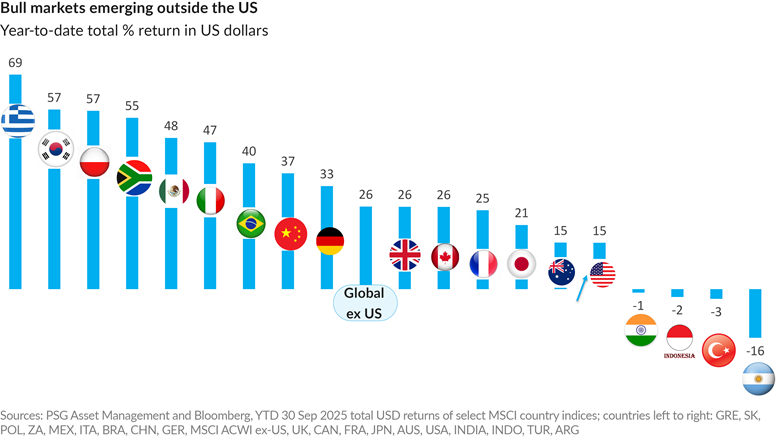

At the start of 2025, investors were positively positioned towards the US, but so far in 2025, markets outside the US have actually outperformed. Global stocks excluding the United States (MSCI World ex-US Index) delivered a return of 26% compared to the S&P 500 Index’s return of 15% for the year to the end of September. Other standouts include China, which delivered 37%, Brazil (40%) and the SA market, which is up 55% in US dollar terms (MSCI South Africa Index).

While the returns delivered by US markets have been relatively attractive, they look less appealing if we consider them on a relative basis, and especially when we take the effect of a weaker dollar into account.

Foreign investment managers reporting on US performance in their home currency, e.g. in euro or even rands, have only recorded returns of between 1% and 5% for the year to the end of September. If this trend is sustained, it is reasonable to expect that investment managers are going to reconsider their exposure to US assets.

Thus, we see many potential headwinds to the US exceptionalism narrative, even as many investors are positioned in indices dominated by tech stocks, which are pricing in very rosy expectations based on the continuation of the status quo.

The value in finding opportunities in out-of-favour and overlooked areas

Despite markets trading close to record highs, there are many exceptional opportunities to be found for those willing to look in less crowded parts of the market. We are currently finding good opportunities in out-of-favour areas of the market, led by our 3M investment process with its focus on seeking out quality assets trading at a discount to fair value. Importantly, we believe avoiding richly valued areas of the market also enables us to construct portfolios that can perform at low levels of risk, while offering our clients valuable diversification benefits.

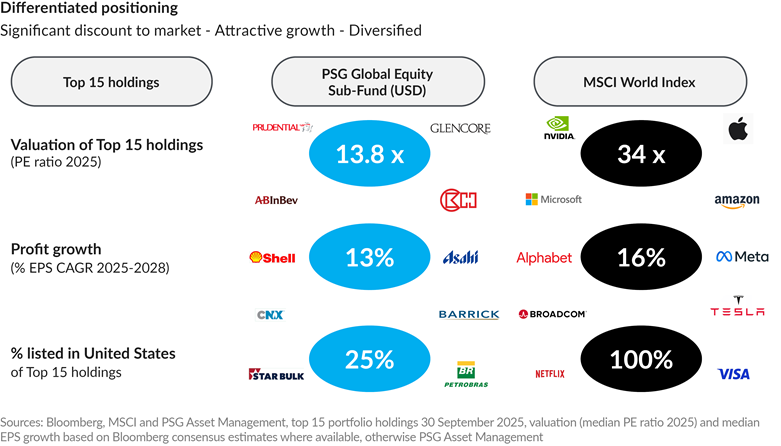

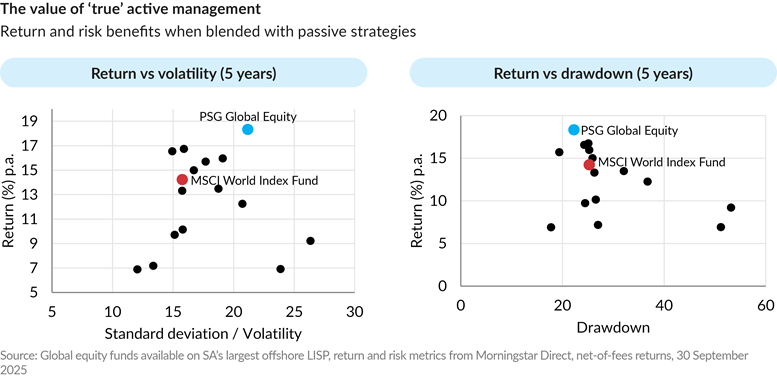

Our portfolios provide a case in point. As an example, while we haven’t had a lot of exposure to the US and the artificial intelligence (AI) narrative and have looked materially different to the index over the past five years, our funds have performed very well. A key benefit is that our funds have delivered those returns at lower levels of drawdown than the index – providing valuable diversification benefits to our clients. Not only are the stocks included in our portfolios a lot more diversified than the MSCI World Index, but they also trade at large valuation discounts to the index and are expected to offer very strong earnings growth prospects in the years ahead.

Looking ahead, we see a rich opportunity set

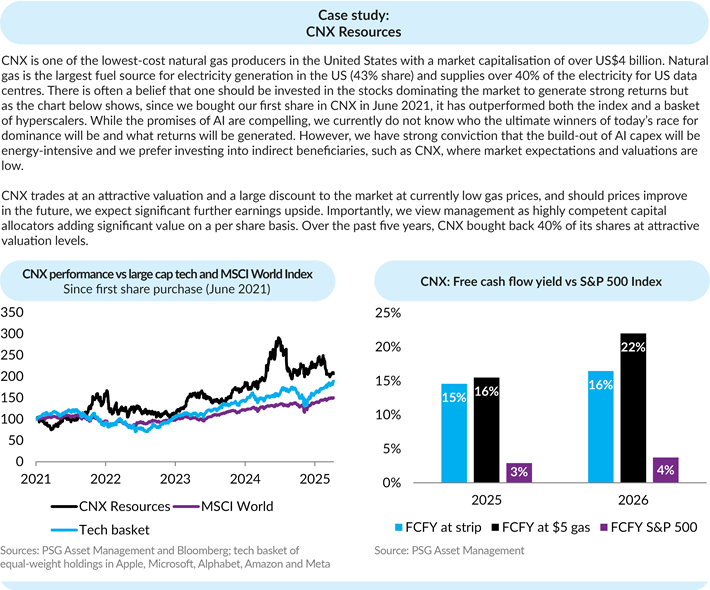

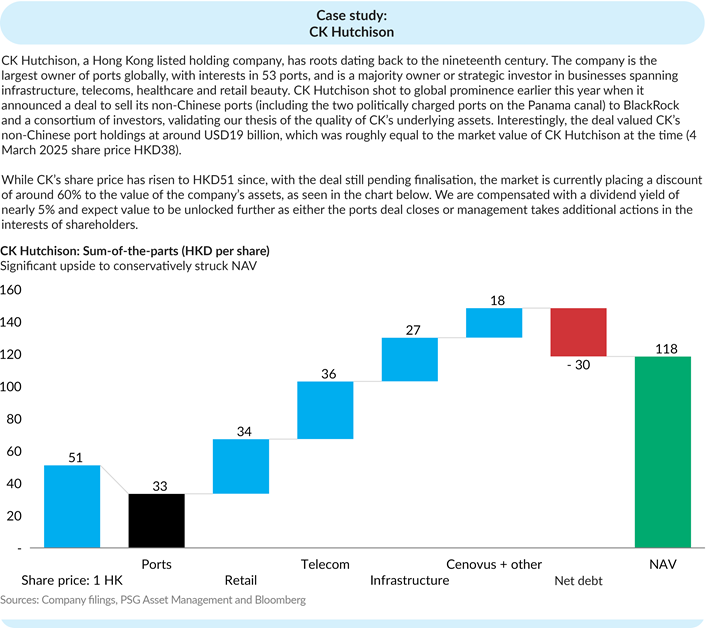

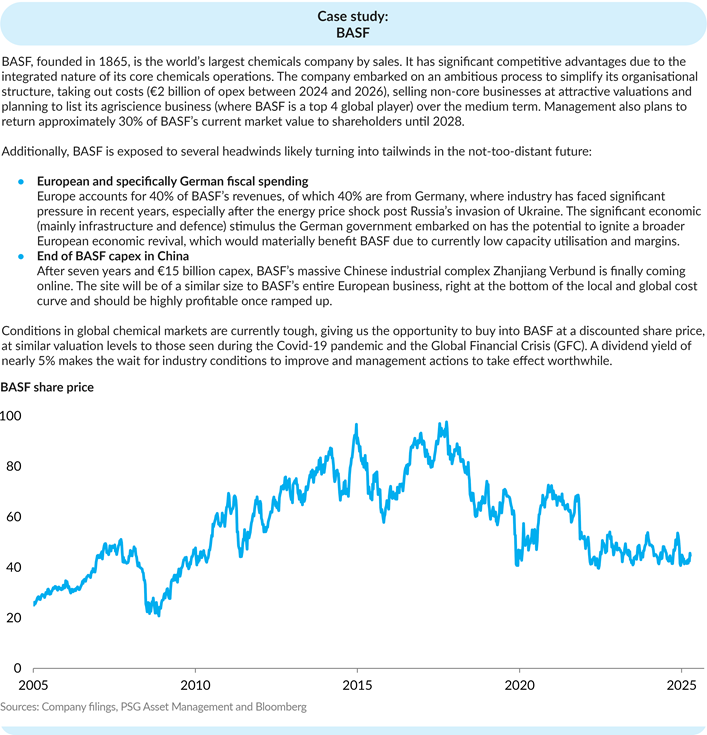

We are currently finding great opportunities in less crowded areas of the market, ranging from Asian life insurance companies to global brewing stocks and spirits companies, and in commodities, such as natural resource companies and energy stocks. We are also finding good opportunities in emerging markets such as Brazil, China and South Africa, in consumer companies and banks. More recently, we have found good ideas in the German stock market, most notably in chemical producers. However, while these opportunities are largely outside of the US, it should be noted that we do not follow an exclusionary investment approach to finding opportunities. We have recently added several attractive opportunities in the US healthcare and payments sectors.

The case studies below serve to illustrate that many opportunities exist beyond the over-owned sector of the market, with the ability to deliver returns on par with or better than those on offer from some of the most popular sectors and areas of the market. However, we believe as these opportunities are characterised by less rosy assumptions and typically bought at very attractive valuations, investment in them holds significantly less risk.

Don’t underestimate the value true active management adds

With stock markets dominated by a few sectors and counters that are trading at historically high valuations driven by very rosy expectations, truly active managers are well positioned to add value to clients. In the environment we see lying ahead, we believe being differentiated from the index and many peers will add significant value to client solutions and portfolios.

Recommended news

Welcome to the latest edition of the Angles & Perspectives - Q3 2025

In this edition, we consider what lies ahead after a strong run in equity markets and given rising levels of market concentration. Head of Research Kevin Cousins highlights the hidden risks in hugging an index. Fund Managers Shaun le Roux and Mikhail Motala unpack the drivers behind the equity rally, and share where they are currently finding opportunities locally. Finally, Fund Manager Philipp Wӧrz and Deputy Chief Investment Officer Greg Hopkins turn their focus to global markets, and explain the value of our differentiated approach.

Read moreIntroduction - Angles & Perspectives Q3 2025

Read moreThe hidden risks of hugging an index - Angles & Perspectives Q3 2025

Read moreCan equity markets continue their strong run? - Angles & Perspectives Q3 2025

Read moreStay Informed

Sign up for our newsletters and receive information on finance.