Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

13

February 2024

Investing in SA-Exposed Securities: Finding the Opportunity Amidst the Danger - Angles & Perspectives Q4 2023

Justin Floor, Head of Equities

Asset Management

Dirk Jooste, Fund Manager

Asset Management

Investing in SA-exposed securities: Finding the opportunity amidst the danger

Tilting the odds in your favour by buying with a margin of safety

It’s a challenging time to be an investor in domestic South African securities. Some of the well-telegraphed issues and challenges that exist and that have dominated headlines include:

- Load shedding

- Trouble at Transnet

- Elevated corruption levels

- Unhelpful politics (Lady R, NHI)

- Water infrastructure and municipal disarray

- The highest interest rates since the Global Financial Crisis (GFC)

In response to these challenges, many local assets have derated materially. The equity market is being priced at very low valuation multiples, and in some cases, companies are acutely undervalued relative to their prospects for growth and shareholder return. Our bond yields are close to 13% with one of the highest real rates globally. The rand has been weak and has underperformed the currencies of many other emerging market (EM) countries.

PSG Asset Management follows an integrated global investment process, and we find that examining the SA opportunity set through the eyes of a global investor provides a valuable perspective. It is helpful in contrasting the potential opportunities and risks in local assets relative to competing offshore opportunities.

Clearly, the domestic environment is not without risks and therefore care and prudence are needed. Nevertheless, it seems to us that a very compelling opportunity now exists to earn healthy returns going forward, and have therefore been using the weak price environment to increase exposure to SA securities in our multi-asset portfolios over the past year. We share some of the insights that have informed this perspective below.

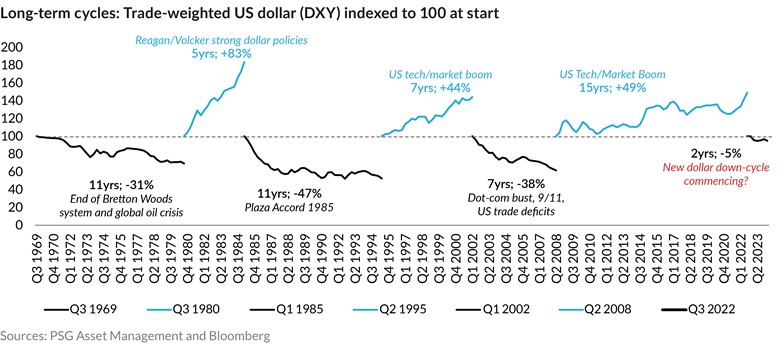

Take note of the long-term US dollar cycle

Since the late 1960s, the trade-weighted US dollar has been through multiple cycles (refer to the graph below) in which it was either dominant, or weak. These cycles have typically lasted multiple years at a time, ranging between five and fifteen years, or around ten years on average. They generally have coincided with large inflation and interest rate cycles. Periods in which the US dollar is strong generally favour US asset prices over those in the rest of the world.

Emerging markets and commodity markets seem to be particularly sensitive to the strength or weakness of the greenback. We note that the world has just concluded a notably long and pronounced cycle of dollar strength (which commenced during the GFC in 2008 and ended in 2020). The evidence of the last few years suggests that we may be in the early stages of a dollar down-cycle. History suggests this cycle could gather momentum and last many years more, with very important implications for investors.

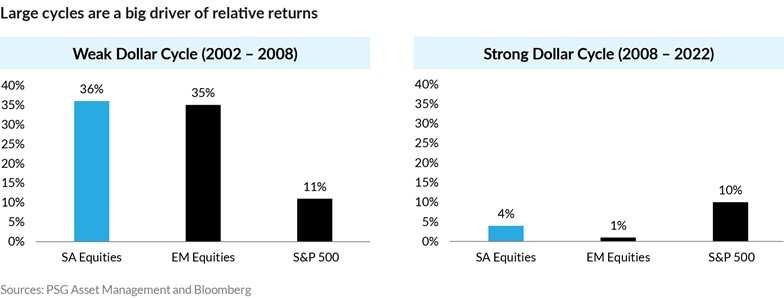

As the chart below illustrates, emerging market and SA equities have not fared well during strong US dollar periods in the past. However, it also highlights that periods of dollar weakness can be a significant tailwind for investment returns in emerging markets, including South Africa. The conclusion for us is that we may be in the early stages of a global backdrop that is much more helpful towards emerging markets than what we have experienced over the last 15 years. This may include South African assets as well.

Some domestic headwinds are starting to abate (and may turn into tailwinds)

We have already alluded to some of the key factors above that have challenged SA asset prices. However, our analysis shows that some of these headwinds are likely to improve and may even turn into tailwinds. Individually, improvement in these factors could be beneficial – in combination, they could be very powerful.

Firstly, high interest rates (highest since the GFC) are likely to stabilise and decrease, easing domestic financial conditions. The current interest rate cycle has been a headwind for the SA economy and security valuations as the economy, companies and consumers adapt to and absorb the highest interest rates in 15 years.

While our interest rates are influenced by US Federal Reserve policies, our own inflation dynamics are reasonably well behaved, and we think there is a good chance of interest rates starting to fall later this year and into 2025. We expect inflation to average 5% and the South African Reserve Bank (SARB) should keep the real rate at around 1% to 2.25%, allowing interest rates to fall by 1% to 2%.

This translates into a sizable reduction (15% to 30%) in the base cost of capital in the economy and could meaningfully benefit consumers’ disposable income and company interest rate expenses, while also having a positive impact on security valuations like PEs and bond yields.

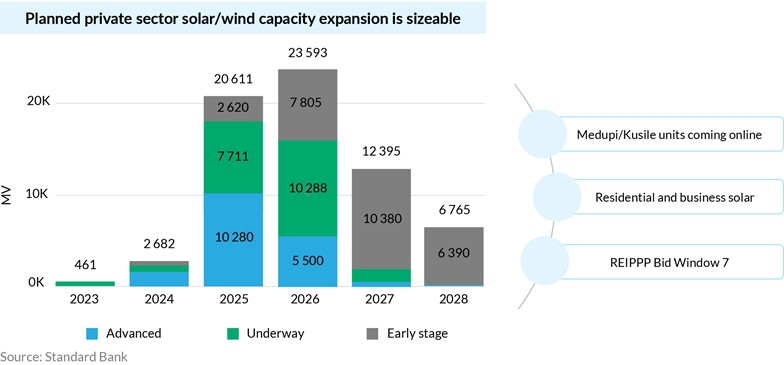

Secondly, SA’s infrastructural challenges may be set to improve. Load shedding is likely to be much lower in the next few years. We see good progress on some of the much-needed energy reforms. The private sector is coming to the party, and there is considerable new capacity in the pipeline. In addition, private sector resources have been deployed to Eskom’s generation fleet and the large Medupi and Kusile units are already coming online. More reforms are needed but the direction of travel will be felt tangibly in economic growth, and the earnings and cash flows of affected companies thanks to fewer sales disruptions, lower energy costs and lower capex requirements.

Energy constraints are lifting…

In addition, although progress has been slow, some improvement is now starting to be seen at Transnet and the ports, with more private sector participation becoming visible. We think more improvement is likely in the near future (although off an unacceptably low base) and there are also likely to be some winners in the local economy from this.

A confluence of technical factors is greatly increasing the likelihood of better outcomes ahead

The last five years have seen a vicious cycle of foreign equity and bond outflows, relaxation of prudential offshore limits (Regulation 28), and local and foreign institutional investors reducing allocations to SA assets with the average global emerging market portfolio being underweight to South Africa. We think it is likely that we are approaching a floor in this recalibration (for example, many large SA balanced funds are close to maximum offshore capacity and may need to start directing funds back to rand assets). We see signs of a bottom in the market, as private capital is buying up (delisting) our cheap companies, and company insiders are increasing buyback activity on the JSE.

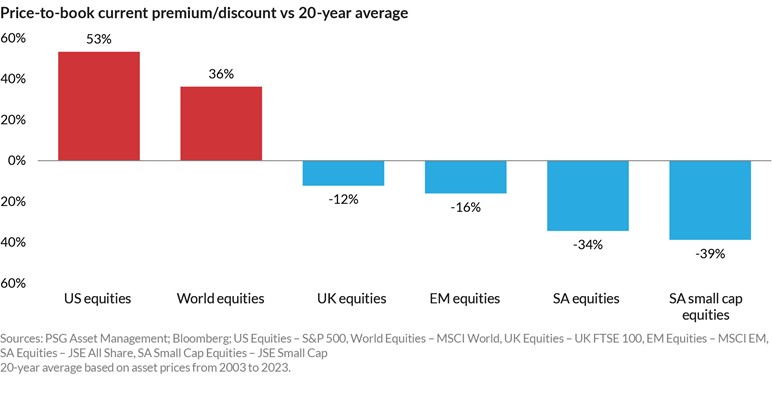

Finally, despite some of the reasons for (tempered) optimism at better prospects ahead, South African assets are valued at prices significantly below global comparatives and their own history.

We have become more optimistic about the outlook for SA assets, because we are finding a happy overlap between prospects for improved valuations ahead, and some quality assets that are priced at a steep discount.

Be selective about SA assets – but don’t ignore the opportunities

Not all opportunities are created equal on the JSE: there will be winners and losers. This is why we believe stock picking will be key going forward – because it will require a dedicated and proven bottom-up stock selection process to distinguish the underappreciated gems from the rest.

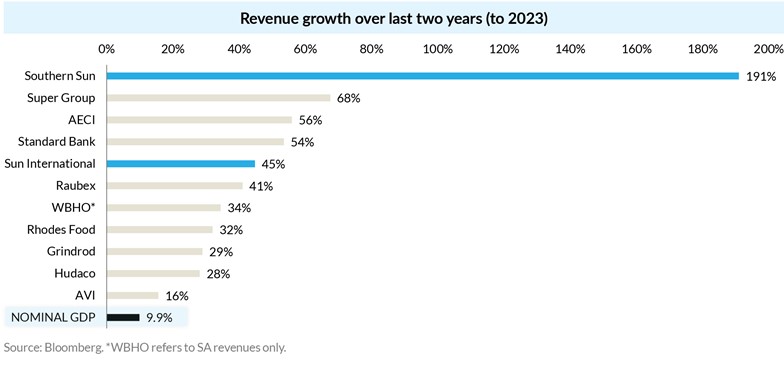

When looking at the SA market, we seek out companies with the potential to grow, especially where that growth is less dependent on the broader SA economy. Good examples are infrastructure stocks (we own Raubex, WBHO, Afrimat and Grindrod, for example) and the tourism and leisure industry (Sun International, Southern Sun Hotels and HCI come to mind).

Pockets of growth exist

In addition, we aim to identify companies with agile and entrepreneurial management who consider how to protect and grow the value per share of the companies they manage. We are also closely watching the increasing trend among companies to repurchase their undervalued shares on the market, as this can be a sign of strength and may benefit shareholders.

The SA market is very top-heavy, and there are substantial benefits to being able to access a wider opportunity set including stocks with smaller market capitalisations – something which can prove challenging to some of the larger managers.

Moreover, we believe our globally integrated process offers further benefits to our clients. An integrated approach, searching the globe for attractive securities and holistically putting them alongside SA securities, allows us to access the opportunity set on offer in a diversified and balanced fashion.

Recommended news

Welcome to the latest edition of the Angles & Perspectives

In this edition, Head of Research Kevin Cousins and Co-CIO Greg Hopkins explain why culture is so important to us at PSG Asset Management, and how it enables us to achieve excellent investment outcomes for our clients. Then, we turn our attention to the many-faceted nature of risk. Head of Equities Justin Floor and Co-CIO John Gilchrist unpack why a more nuanced view of risk can facilitate more robust decision-making. Finally, Head of Equities Justin Floor and Fund Manager Dirk Jooste get to grips with the thorny issues of the risk of investing in SA equities, and weighing them against the opportunities we see ahead.

Read moreIntroduction - Angles & Perspectives Q4 2023

Read moreFostering a Culture of Teamwork and Learning - Angles & Perspectives Q4 2023

Read moreWe are What We Measure - Getting to Grips with Volatility - Angles & Perspectives Q4 2023

Read moreStay Informed

Sign up for our newsletters and receive information on finance.