Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

18

February 2026

Why inflation-linked bonds make sense even when inflation is low - Angles & Perspectives Q4 2025

Duayne Le Roux, Fund Manager

Asset Management

Why inflation-linked bonds make sense even when inflation is low

Local inflation has been declining and has remained contained for the last two years. In addition, the South African Reserve Bank’s move to a lower inflation target looks set to further entrench the low inflation environment. We would argue that investors need to carefully consider the shifting investment landscape before allocating their assets. Counter-intuitively, despite a downward shift in inflation, we believe inflation-linked bonds (ILBs) can play a valuable role as part of a diversified fixed income portfolio.

How SA shifted to a low inflation environment

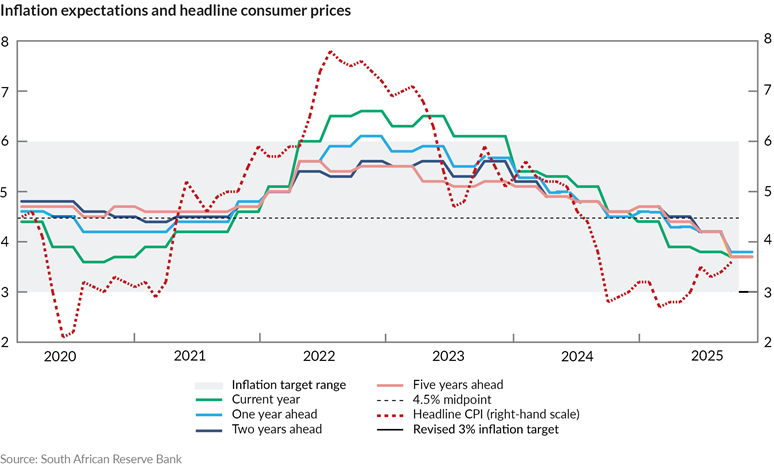

SA inflation has declined from 2022 highs and has been printing in a narrow range since late 2024. The South African Reserve Bank (SARB) and National Treasury have now officially moved towards a lower inflation target. (Read more about the potential benefits of this development here.) The market has responded positively to the news, and we have seen a broad-based downward trend in inflation expectations, which is reflective of the credibility of these institutions.

Although the adjusted target was only announced in November 2025, inflation expectations for the next 1 to 3 years have already moved much lower (refer to the chart below), indicating a successful reframing of the inflation outlook in the SA context.

Asset prices have responded positively to the shift

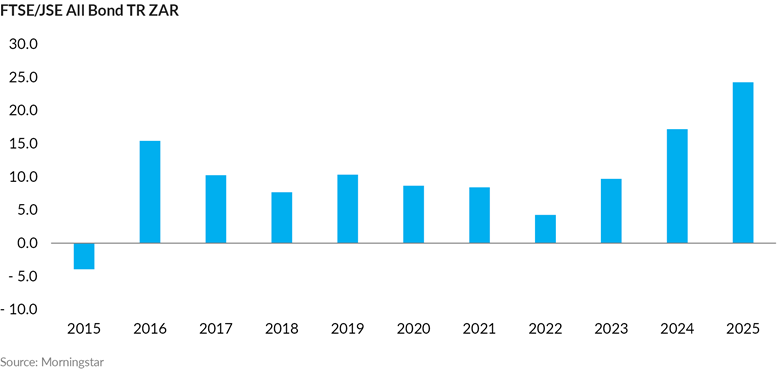

Lower inflation and (cautious) rate cuts by the SARB have positively impacted asset prices: equity and fixed income markets have performed well. South African nominal government bonds have seen two of the most impressive years in history. Returns on South African government bonds (proxied by the All Bond Index (ALBI)) amounted to 17% in 2024 and 24% in 2025.

Other shorter-term fixed income instruments have also done well, although this is less widely spoken about. Consider, for example, the very large and institutional market for negotiated certificates of deposit (NCDs). Seen as the primary financing mechanism for our big institutional banks, these instruments are held widely across portfolios – particularly in low-risk mandates such as income and multi-asset income funds. Due to their highly prized ability to lock in attractive real yields, we have seen the yields on offer materially compress (resulting in a rise in prices, which is good for investors in these instruments). Currently, 5-year NCDs are yielding 7.4%, while they were yielding 9.4% two years ago. This is a 2.0% compression in yield.

Investors should carefully assess the opportunities in the current landscape

Despite the current lower inflation environment, mitigating the effects of inflation remains one of the principal objectives for investors. While we are a proponent of the move to a 3% inflation target and acknowledge the strong credibility of the SARB and National Treasury, we acknowledge that South Africa is an open economy and that there are a multitude of ways in which higher inflation could materialise. These include, for example, higher global food or oil prices, or a more enduring increase in local demand, which could put upward pressure on inflation. In short, risks remain.

Although it has been a spectacular two years for fixed income investors, assets will need to be rolled over into new securities as they mature. However, in the current environment, finding high and stable nominal yields going forward will become more challenging. While some investors may be comfortable using lower forward inflation assumptions to justify locking in the nominal fixed rate yields (currently between 7.0% and 7.5%) available in shorter-term fixed income instruments to achieve real return targets, we think it is the right time to ask whether there are attractively priced, low-risk alternatives.

Inflation-linked bonds are attractive, even in this lower inflation environment

Inflation-linked bonds (ILBs) offer an attractive solution to the risk of unexpected inflation surprises. ILBs are guaranteed to pay a starting yield plus inflation over the period from start to maturity. In addition, should the starting yields compress over time, there is also the potential of a capital gain.

As we have previously highlighted, ILBs have become more attractive over time, and we have been incrementally adding them to our portfolios since 2019. If they can be bought at an attractive price, inflation-linkers secure a return that is immune to inflation and credit risk, and less sensitive to interest rate risk than their fixed rate counterparts. Thus, they provide an attractive pathway to securing a real return for clients, and we believe short-dated ILBs are a compelling destination for cash and maturing shorter-dated instruments, such as NCDs. However, as with all things, the price at which these assets are bought is critical.

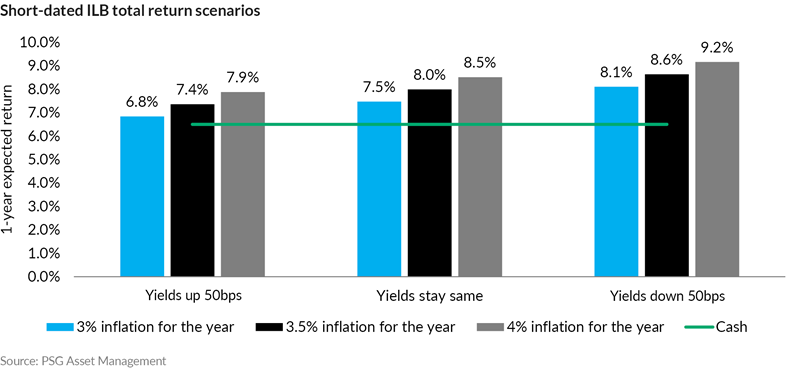

These instruments currently offer a real yield of 4.2% – but is this enough to compensate for an environment where inflation is low? We think so. As the next chart highlights, even if inflation stays at 3% over the next year (the December 2025 inflation print was 3.6%) and yields increase by 50 basis points, returns on these ILBs would still equal the return available on cash (currently yielding 6.5%). And if ILB yields compress and/or inflation prints higher than 3%, these ILBs are likely to outperform cash by a significant margin. This makes it likely that we will achieve returns equivalent to those available on NCDs, while enjoying inflation protection and upside potential.

A dynamic approach to shifting opportunities in the fixed income market

The declining and low inflation environment of the last two years has been excellent for nominal bonds, but securing good real returns for fixed income investors will likely become more challenging with proceeds from maturing portfolio instruments being reallocated in a low inflation environment. In addition, the risk of inflation surprises remains, given that South Africa is a small open economy and vulnerable to supply shocks. ILBs present an elegant and a low-risk way to lock in very high real yields (with the potential to deliver excellent results should conditions change) – importantly, while keeping a firm eye on the overall risk levels in the portfolio. With this in mind, we have been steadily adding ILB exposure to our portfolios at attractive yields.

Recommended news

Welcome to the latest edition of the Angles & Perspectives - Q4 2025

In this edition, we discuss how our process leads us to construct portfolios that are able to do well in a variety of market conditions. Head of Research Kevin Cousins discusses the shortcomings of forecasts, and our preference when navigating an uncertain macro environment. Chief Investment Officer John Gilchrist shares how our stock selection positions our portfolios to excel in a variety of scenarios, while Fund Manager Marc Beckenstrater asks whether large, global managers are really best positioned to deliver performance to investors. Finally, Fund Manager Duayne le Roux highlights that despite a softening interest rate environment, inflation-linked bonds can make an attractive addition to fixed income portfolios.

Read moreFinding opportunities that will reward investors in most environments - Angles & Perspectives Q4 2025

Read moreBoom or bust in 2026? That is the wrong macro question! - Angles & Perspectives Q4 2025

Read moreThe myth of size, scale and location in active asset management - Angles & Perspectives Q4 2025

Read moreStay Informed

Sign up for our newsletters and receive information on finance.