Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

25

August 2021

A radical proposed amendment to the Income Tax Act that emigrants must take note of

Tian Ebersohn CFP®

Wealth Adviser

The proposed Tax Amendment Act introduced by the Minister of Finance in the National Assembly on 28 July 2021 will have far-reaching consequences for those planning to emigrate. Implementation of the new legislation is proposed for 1 March 2022.

“ South Africans who emigrate from South Africa after 1 March this year will have to wait three years before they can access their retirement funds. ”

Pretoria East August Newsletter 2021

The proposed Tax Amendment Act introduced by the Minister of Finance in the National Assembly on 28 July 2021 will have far-reaching consequences for those planning to emigrate. Implementation of the new legislation is proposed for 1 March 2022.

The proposed amendments follow close on the heels of the so-called three-year waiting period implemented on 1 March this year and that now applies to emigrants. Briefly, the waiting period means that South Africans who emigrate from South Africa after 1 March this year will have to wait three years before they can access their retirement funds. The three-year period commences on the date on which the emigrant ceases to be a South African resident for tax purposes.

The proposed amendment aims to add a new section to the existing Income Tax Act (Act 58 of 1962), which will henceforth be known as section 9HC.

The inclusion of this new section will mean that anyone who emigrates will be viewed as having “withdrawn” his full retirement benefit on the day prior to having given up his status as a South African resident by way of formal emigration.

The consequences of this clause for the emigrant are far-reaching as section 9HC(2)(a) then comes into force and the value of the emigrant's pension fund, provident fund, preservation fund and retirement annuity is considered to have been "withdrawn", and to have accrued to the emigrant.

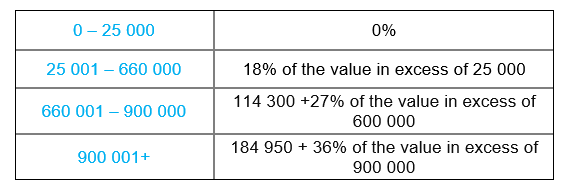

As soon as the value of the retirement fund “accrues” to the emigrant in this way, tax becomes payable according to the retirement tables as contained in paragraph 2(1)(b) of the second schedule of the Income Tax Act. The tax scale is as follows:

Should a person with a retirement benefit of, for example, R10 000 000 emigrate from South Africa, the proposed amendment would have the following implications:

- He will be deemed to have “withdrawn” from his pension fund in terms of the provisions of section 2(1)(b)(ii) of the second schedule (Income Tax Act).

- This deemed “withdrawal” gives rise to a tax liability in line with the withdrawal table set out in paragraph 2 (1) (b). This withdrawal table is a tax scale with different notches, and the tax rate becomes progressively higher as the value of the amount withdrawn rises.

- This amendment to the law thus leads to a bizarre situation whereby tax is levied on a withdrawal from retirement benefits to which the individual has no access for a period of three years.

- In addition to the tax liability that arises, the amendment to the law further stipulates that interest will be charged at the rate as prescribed by section 189 of the Tax Administration Act.

- The interest rate is currently set at 7% per annum.

Joon Chong, a tax expert with a well-known law firm, is quoted in a Moneyweb article (www.moneyweb.co.za) as mentioning that this proposed amendment to the law could lead to numerous legal and practical challenges. The first and most important thing she mentions is that certain countries (especially those countries to which South Africans normally emigrate such as, among others, Australia, England, New Zealand and Germany) have the right to tax certain income under their double taxation agreement with South Africa. This means that the amendment can give rise to double taxation of income on the so-called withdrawal amount.

Hugo van Zyl, a tax and currency control specialist at The Tax Faculty, notes that emigrants who lose their jobs abroad due to circumstances such as the Covid-19 pandemic and who are forced to return to South Africa within three years of emigration are especially likely to find themselves in financial distress.

With this in mind, it is extremely important for anyone planning to emigrate to take note of the legislative amendment that is likely to come into force on 1 March next year and to do their planning well in advance.

Pretoria East | Lynnwood Bridge Office Park, Kaaimans Building, 4th Floor, Lynnwood Manor | Postnet Suite 96, Private Bag X025, Lynnwood Ridge 0040 Tel: 0861 774 000 | Fax: 012 349 5300 | pretoriaoos@psg.co.za | psg.co.za/pretoriaeast

The opinions expressed in this document are the opinions of the writer and not necessarily those of PSG and do not constitute advice. Although the utmost care has been taken in the research and preparation of this document, no responsibility can be taken for actions taken on information in this newsletter.

PSG Wealth Financial Planning (Pty) Ltd is an authorised financial services provider. FSP 728.

Stay Informed

Sign up for our newsletters and receive information on finance.