Fraudulent Telegram and WhatsApp groups

Please beware of fraudulent Telegram and WhatsApp groups impersonating PSG Financial Services, our divisions and our advisers. Be cautious, verify links and contact your adviser or Client Services if you have any queries or concerns.

28

January 2026

What we know for sure about 2026

John Gilchrist, Chief Investment Officer

PSG Asset Management

What we know for sure about 2026

At this time of the year, it’s traditional for market professionals – including banks, brokerages and asset managers – to outline their expectations for the year ahead. These detailed predictions, which frequently include estimates of percentage returns from various asset classes and market indices for the year, belie the impossible nature of such a task.

Benjamin Graham said, “In the short run the market is a voting machine, but in the long run it is a weighing machine.” This captures the challenges associated with predicting short-term market moves with any level of success. Short-term market movements are driven by human behaviour and emotions, including psychological biases like fear, greed, panic and herd mentality (the voting machine), all of which are notoriously difficult to predict. However, it is fundamentals (the weighing machine), which are what most analysts focus on, that ultimately drive long-term returns.

PSG Asset Management’s longer-term focus means we fully understand the futility of these annual predictions. However, we do not escape the pervasive questions about our outlook for the year, and when asked, we highlight areas of the market where we believe the odds for above-market returns over the next 3 to 5 years are in your favour.

We do this by focusing on equity opportunities where both valuations and earnings are low, or fixed income opportunities where real returns more than compensate for the risk. However, prediction season prompted us to ask what we know for sure about 2026. And while a knee-jerk, cynical response to this question may be “nothing is certain”, we believe we can respond more constructively than that. Crucially, these ‘certainties’ also hold important clues for investors aiming to construct resilient portfolios capable of navigating a seemingly increasingly uncertain environment.

So, what do we believe can we fairly confidently expect in the year ahead?

- Geopolitical events will continue to dominate news flow and cause periods of volatility: While all of us have been brought up in a pax-Americana world, over the last year we appear to have swiftly moved towards a multipolar world with potentially distinct spheres of influence. Such geopolitical realignments take time, are never easy, and involve friction, posturing and tests of resolve. The recent American-Chinese trade disputes and the current tensions around Greenland are prime examples of this. While recent news flow has centred around US President Trump’s activities, his actions during the first year of his second term have set in motion events that can’t easily be reversed, and that will have significant long-term implications well beyond his term of office.

- Interest rates and inflation will continue to be a focus for market participants: The decisions of the US Federal Open Market Committee (FOMC), and the associated minutes, receive substantial attention – even in normal market conditions. With Federal Reserve Chairman Jerome Powell’s term ending in May 2026, Trump’s new appointee will be under extreme scrutiny. This appointee will be under pressure from Trump to reduce interest rates, regardless of what the economic data indicates, and despite the fact that the final decision is based on the view of the 12 FOMC voting members. With December 2025 US headline inflation at 2.7% year on year, and one to two rate cuts expected in 2026, markets do not view inflation as a problem. This is further supported by break-even inflation implied market prices at 2.3% over 5 to 10 years (slightly above the Federal Reserve’s 2% target), with longer-term (20- to 30-year) expectations hovering in the 2.2% to 2.4% range. We believe US inflationary pressures associated with tariffs, immigration policies and an expansionary fiscal policy are currently under-appreciated, creating an interesting market skew in the event of a non-consensus outcome.

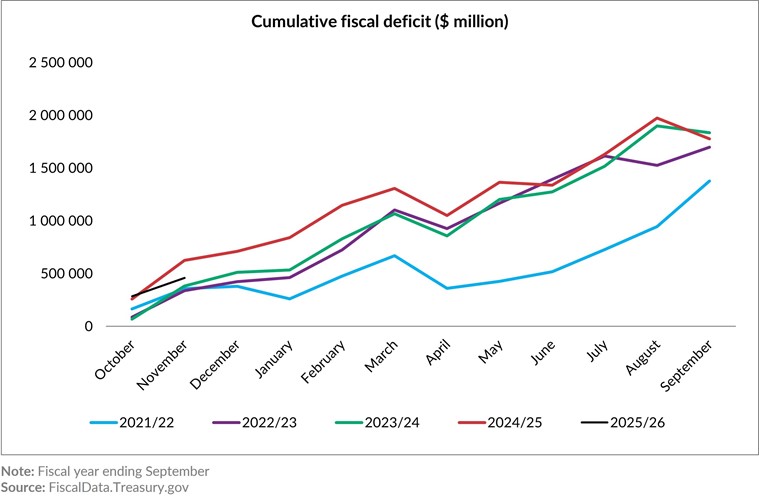

- US government debt will continue to increase: US Federal government debt reached approximately US$38.4 trillion (of which $30.8 trillion is publicly held) at the end of 2025, an increase of nearly $2.3 trillion over the 2025 calendar year (the fiscal year ends in September). The last three US fiscal years show annual cumulative fiscal deficits ranging from $1.7 to $1.8 trillion per annum. While it is still early days, the 2026 fiscal year, despite the much-touted tariff revenue, shows a similar trend, with interest costs in particular continuing to increase, having approached $1 trillion in the 2025 fiscal year.

Cumulative fiscal deficit ($ million)

- Artificial intelligence (AI) will remain a critical driver of markets: Just over three years after AI captured the world’s attention with the release of ChatGPT, it appears that we are set to move from a period of indiscriminate growth (where companies were rewarded based on sentiment or on their ability to deploy AI capital expenditure at scale) towards a greater focus on monetisation and return on investment. With AI infrastructure expenditures exceeding US$400 billion in 2025 and set to be even higher in 2026, investors require substantial and growing revenue to justify this spending. The Magnificent 7 (Mag7) shares have been significant beneficiaries of the AI theme, and now account for over 34% of the S&P 500 Index’s market capitalisation. As a result, a clear demonstration of AI’s ability to drive monetisation and revenue generation will be a key factor informing equity market movements.

- Trump is likely to continue dominating news flow, with markets reacting to the US president’s social media posts: A volatile start to 2026 has made it clear that President Trump is likely to continue advocating his views on social media and dominating headlines, moving markets in the process. With the rules of the post-war, pax-Americana playbook being rewritten on a seemingly daily basis, it is important that portfolios should be designed to deliver for investors in a changing environment where the rules of thumb of the past may no longer apply.

These tentative ‘certainties’ about the year ahead offer some insights for investors looking to maintain and build their future wealth. They underscore the importance of two key principles that we believe will prove valuable in 2026:

- Thoughtful diversification: Rising geopolitical tensions and unpredictable US leadership mean that investors are likely to face intermittent bouts of volatility. Diversification remains one of the most important risk mitigators available to investors. However, strong US performance and dominance of the AI narrative mean that many indices have become highly concentrated, including the S&P 500 Index and MSCI World Index. Not only are investors likely to see a skew towards the US in their portfolios as a result, but also to the technology firms which have benefited from the AI narrative. With the continuation of the AI run looking increasingly uncertain and the American exceptionalism narrative starting to flag, investors need to carefully consider whether their portfolios are adequately diversified. In addition, increased geopolitical fragmentation also raises the likelihood of divergences in economic outcomes. This means that it is important that portfolios include diverse sources of return, rather than focusing on a single sector or geographic region.

- Inflation and portfolio protection: Policy choices in the US seem set to maintain inflation pressures, as will escalating geopolitical fragmentation that is likely to cause reconfigurations in global supply chains and drive up defence spending. Therefore, it is imperative to ensure that portfolios are suitably positioned to deliver inflation-beating long-term growth and maintain investors’ spending power. While US bonds have been a safe-haven asset for years, rising US debt and the spectre of fiscal dominance mean investors may not be rewarded for holding these assets going forward, especially if US dollar weakness persists.

Reconsider traditional playbooks

In our view, including thoughtful diversification and robust inflation and portfolio protection better equip investors to secure long-term returns than trying to select which specific sector or geography will outperform in the year ahead. At PSG Asset Management, our globally integrated 3M investment process means that we are well positioned to identify investment opportunities wherever they may reside, and construct our portfolios with care to deliver in a variety of scenarios.

John Gilchrist is the Chief Investment Officer at PSG Asset Management.

Recommended news

How will 2025 be remembered?

Read more

Welcome to the latest edition of the Angles & Perspectives - Q3 2025

In this edition, we consider what lies ahead after a strong run in equity markets and given rising levels of market concentration. Head of Research Kevin Cousins highlights the hidden risks in hugging an index. Fund Managers Shaun le Roux and Mikhail Motala unpack the drivers behind the equity rally, and share where they are currently finding opportunities locally. Finally, Fund Manager Philipp Wӧrz and Deputy Chief Investment Officer Greg Hopkins turn their focus to global markets, and explain the value of our differentiated approach.

Read moreThe hidden risks of hugging an index - Angles & Perspectives Q3 2025

Read moreAn integrated approach offers advantages – no matter where you’re investing

Read moreStay Informed

Sign up for our newsletters and receive information on finance.